Global Titanium Tetrachloride Market Size, Share, and COVID-19 Impact Analysis, By Production Process (Chlorination, Magnesium Thermal Reduction, Sodium Thermal Reduction, and Aluminum Reduction), By Derivatives (Titanium Nitride, Titanium Dioxide, Titanium Metal, Smoke Screens, and Others), By End Use (Aerospace, Defense, Dyes, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Titanium Tetrachloride Market Size Insights Forecasts to 2035

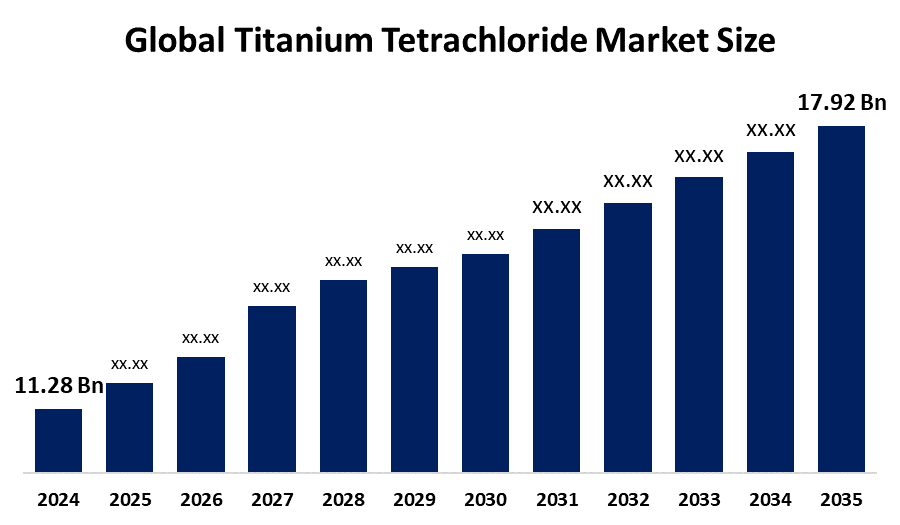

- The Global Titanium Tetrachloride Market Size Was Estimated at USD 11.28 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 4.3% from 2025 to 2035

- The Worldwide Titanium Tetrachloride Market Size is Expected to Reach USD 17.92 Billion by 2035

- North America is expected to Grow the fastest during the forecast period.

Get more details on this report -

According to a Research Report Published by Spherical Insights and Consulting, The Global Titanium Tetrachloride Market Size was worth around USD 11.28 Billion in 2024 and is predicted to Grow to around USD 17.92 Billion by 2035 with a compound annual growth rate (CAGR) of 4.3% from 2025 to 2035. The titanium tetrachloride market experiences growth because of increased demand for Tio, pigments, which are used in coatings, plastics and paper products and because of rising consumption of lightweight titanium metal in aerospace and defence and automotive industries. The demand for products increases because Asia-Pacific countries expand their infrastructure and develop their industrial sectors.

Market Overview

Titanium tetrachloride (TiCl4) exists as a colorless to pale yellow liquid, which exhibits high volatility and functions as an essential chemical intermediate that produces titanium dioxide (TiO2) pigment through its chloride processing method and produces titanium metal. The material functions as an essential intermediate, which produces more than 85% of titanium dioxide (TiO2) pigments and titanium metal through the Kroll process while serving as a raw material for catalysts and surface treatment applications. The global market operates through strong market demand, which drives TiO2 sales in the paints and coatings sector and lightweight titanium component sales in aerospace manufacturing.

The titanium powder market for 3D printing shows a growing opportunity because it will reach 8-10% of total demand by 2030 through newly developed applications such as additive manufacturing. The market shows strong growth because LB Group established a production capacity of 200,000 tons for titanium tetrachloride in 2024 to supply increasing demands from titanium dioxide and metal manufacturing. In January 2024, China imposed a 5% Most-Favored Nation tariff and 13% VAT on titanium tetrachloride imports, while it started additional duties on specific U.S. products. The government strengthened its domestic titanium industry through infrastructure investments and supply chain resilience policies, which supported local manufacturers.

Report Coverage

This research report categorizes the titanium tetrachloride market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the titanium tetrachloride market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the titanium tetrachloride market.

Global Titanium Tetrachloride Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024 : | USD 11.28 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 4.3% |

| 2035 Value Projection: | USD 17.92 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 179 |

| Tables, Charts & Figures: | 108 |

| Segments covered: | By Production Process, By Derivatives and COVID-19 Impact Analysis |

| Companies covered:: | The Chemours Company, INEOS, Tronox Holdings Plc, Kronos Worldwide, Inc., Venator Materials PLC, ISK Industries, Toho Titanium Co., Ltd., Ansteel, DowDuPont Inc., The Kerala Minerals & Metals Ltd., Huntsman International LLC, Merck KgA, LB Group, Osaka Titanium Technologies Co., Ltd., and Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global titanium tetrachloride market depends on titanium dioxide (TiO2) pigment manufacturing and titanium metal production, which serve the aerospace and coatings industries. About 90% of titanium tetrachloride produced globally is consumed in TiO2 pigment output, where chloride-route processes offer 15-18% higher efficiency, directly boosting demand from paints, coatings, plastics, and paper industries. The global TiO2 capacity reached approximately 9.93 million metric tons in 2024, which created high demand for TiCl4 and led to market expansion. The growing demand for lightweight titanium alloys in aerospace applications creates ongoing requirements for titanium tetrachloride.

Restraining Factors

The titanium tetrachloride market encounters major challenges due to strict environmental rules that control the handling of hazardous chemicals and the emissions of dangerous substances, thus increasing the costs of compliance. The manufacturing process requires high energy consumption, while the business depends on fluctuating raw material expenses for rutile and chlorine, which reduces profit margins. The market development is restricted because customers choose other titanium production methods and different materials for their downstream requirements.

Market Segmentation

The titanium tetrachloride market share is classified into production process, derivatives and end use.

- The chlorination segment dominated the market in 2024, approximately 58% and is projected to grow at a substantial CAGR during the forecast period.

Based on the production process, the titanium tetrachloride market is divided into chlorination, magnesium thermal reduction, sodium thermal reduction, and aluminum reduction. Among these, the chlorination segment dominated the market in 2024, approximately 58% and is projected to grow at a substantial CAGR during the forecast period. The method achieves high industrial adoption because it operates as a thermochemically stable extraction process that efficiently produces TiCl4 from titanium ores. The system enables extensive mining operations because it successfully operates with both ilmenite and synthetic rutile materials. The new reactor systems, together with their corrosion protection materials and advanced gas handling equipment, achieve operational efficiency while satisfying all environmental standards.

- The titanium dioxide segment accounted for the largest share in 2024, approximately 49% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the derivatives, the titanium tetrachloride market is divided into titanium nitride, titanium dioxide, titanium metal, smoke screens, and others. Among these, the titanium dioxide segment accounted for the largest share in 2024, approximately 49% and is anticipated to grow at a significant CAGR during the forecast period. The production of high-brightness titanium dioxide pigments, which manufacturers use for coatings, plastics and paper products, depends completely on TiCl4, which has established itself as the dominant market force. The chloride process produces better results through its ability to create distinct particle sizes while managing particle distribution throughout the process. The market continues to expand because automotive paints, packaging materials and architectural coatings experience increasing demand, while regulatory bodies permit food-grade and cosmetic-grade products for use.

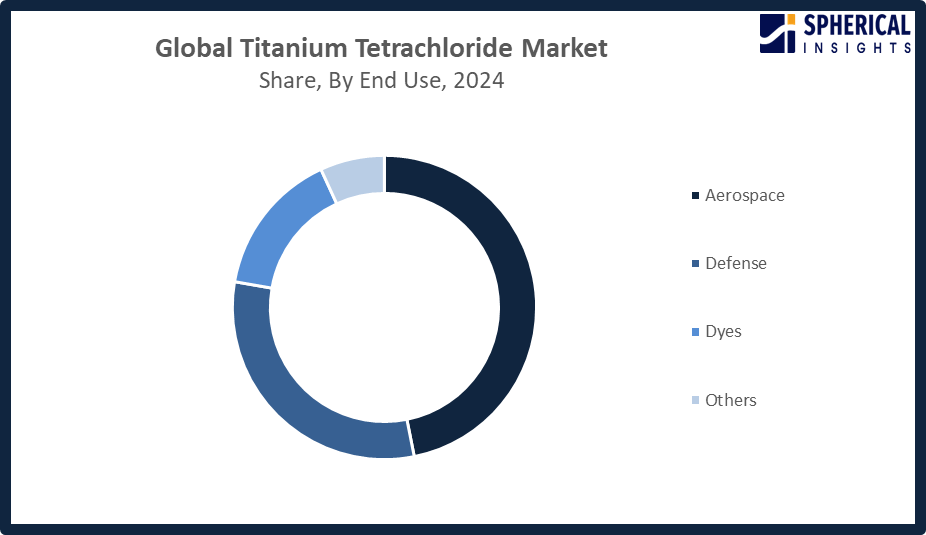

- The aerospace segment accounted for the highest market revenue in 2024, approximately 47% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end use, the titanium tetrachloride market is divided into aerospace, defense, dyes, and others. Among these, the aerospace segment accounted for the highest market revenue in 2024, approximately 47% and is anticipated to grow at a significant CAGR during the forecast period. The Kroll process requires TiCl4 as an essential material to create titanium sponge, which manufacturers use to produce lightweight, corrosion-resistant titanium alloys for aerospace-grade applications. The need for fuel-efficient aircraft, combined with existing aircraft fleet modernization programs, leads to increased titanium consumption for airframe and engine production. The aircraft industry needs strict standards, which, along with advances in sponge metallurgy and alloy processing, create ongoing demand for TiCl4.

Get more details on this report -

Regional Segment Analysis of the Titanium Tetrachloride Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the titanium tetrachloride market over the predicted timeframe.

Get more details on this report -

Asia Pacific is anticipated to hold the largest share of the titanium tetrachloride market over the predicted timeframe. Asia Pacific is anticipated to hold the 48% share of the titanium tetrachloride market due to its strong titanium dioxide pigment production and expanding aerospace and chemical industries. China leads the region with large-scale chloride-route TiO2 manufacturing and integrated titanium metal facilities. India supports growth through rising infrastructure, coatings demand, and government-backed manufacturing initiatives. Japan contributes through high-purity titanium processing for electronics and aerospace applications. Rapid urbanization, industrial expansion, and growing demand for lightweight materials in the automotive and construction sectors collectively drive sustained regional market growth.

North America is expected to grow at a rapid CAGR in the titanium tetrachloride market during the forecast period. North America is expected to have 20% in the titanium tetrachloride market due to strong demand from aerospace, defense, and pigment manufacturing industries. The United States leads regional growth, supported by advanced aerospace production and titanium sponge manufacturing using the Kroll process. Expanding aircraft programs and defense modernization initiatives increase titanium alloy consumption, directly driving TiCl4 demand. Canada contributes through its mineral resources and integrated titanium dioxide production facilities, supporting pigment applications in coatings and plastics, further strengthening regional market expansion. In March 2024, the U.S. Food and Drug Administration reaffirmed titanium dioxide’s approval as a food color additive under 21 CFR 73.575, permitting up to 1% by weight, while reviewing a 2023 petition seeking repeal of its authorization in foods.

Europe is witnessing steady growth in the titanium tetrachloride market due to strong demand from pigment, aerospace, and specialty chemical industries. Germany leads with its advanced coatings and automotive manufacturing sectors, requiring high-quality titanium dioxide through the chloride process. France supports growth through aerospace production, while the United Kingdom contributes through defense and specialty materials. Strict environmental regulations also encourage the adoption of efficient chloride-based TiO2 production technologies across the region.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the titanium tetrachloride market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- The Chemours Company

- INEOS

- Tronox Holdings Plc

- Kronos Worldwide, Inc.

- Venator Materials PLC

- ISK Industries

- Toho Titanium Co., Ltd.

- Ansteel

- DowDuPont Inc.

- The Kerala Minerals & Metals Ltd.

- Huntsman International LLC

- Merck KgA

- LB Group

- Osaka Titanium Technologies Co., Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In January 2026, Tronox Holdings plc announced plans to permanently close its 46,000-metric-ton TiO2 plant in Fuzhou due to weak domestic demand, rising sulfur costs, and oversupply in China. About 550 employees are affected, while global operations will maintain customer supply continuity.

- In July 2025, The Chemours Company introduced Ti-Pure TS-4657, a low-abrasion, chloride-processed titanium dioxide pigment designed for printing inks. Showcased at CHINACOAT in Shanghai, the specialty grade improves ink formulation performance while reducing printing plate wear compared to conventional chloride TiO2 pigments.

- In March 2025, Tronox Holdings plc announced the permanent closure of its 90,000-ton titanium dioxide plant in Botlek following a chlorine supply failure. The decision affects about 240 employees, with the company leveraging its global production network to maintain customer supply continuity.

- In January 2025 the European Commission imposed definitive anti-dumping duties on Chinese titanium dioxide, excluding ink-grade products. Specific duties replace ad valorem rates: 0.74/kg for Longbai, 0.25/kg for Anhui Jinxing, 0.64/kg for other respondents, and 0.74/kg for non-responding firms, effective from customs declaration date.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the titanium tetrachloride market based on the below-mentioned segments:

Global Titanium Tetrachloride Market, By Production Process

- Chlorination

- Magnesium Thermal Reduction

- Sodium Thermal Reduction

- Aluminum Reduction

Global Titanium Tetrachloride Market, By Derivatives

- Titanium Nitride

- Titanium Dioxide

- Titanium Metal

- Smoke Screens

- Others

Global Titanium Tetrachloride Market, By End Use

- Aerospace

- Defense

- Dyes

- Others

Global Titanium Tetrachloride Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. How is the rapid growth in global aerospace production impacting titanium tetrachloride demand for titanium metal manufacturing?Rapid global aerospace production increases demand for lightweight, high-strength titanium components. This drives higher titanium metal output, boosting titanium tetrachloride consumption as a critical intermediate in the Kroll process used for producing aerospace-grade titanium sponge.

-

2. What is the impact of China's massive 6.05 million metric ton TiO₂ production capacity on global titanium tetrachloride supply and pricing?China’s massive 6.05 million mt titanium dioxide capacity has created oversupply pressures, helping push down TiO₂ and related titanium tetrachloride prices globally and forcing export competition, while exerting downward influence on pricing benchmarks and supply balances.

-

3. How are innovations in high-purity titanium tetrachloride (3N, 4N grades) creating new opportunities in semiconductor and electronics applications?Innovations in 3N/4N high-purity titanium tetrachloride are boosting semiconductor and electronics use: demand for ≥99.99% TiCl₄ has grown 30% for ultra-clean thin-film deposition, enabling defect-free chips and advanced electronic components essential for next-gen devices.

-

4. What impact does raw material price volatility for rutile and ilmenite have on titanium tetrachloride manufacturer profitability?Raw material price volatility for rutile and ilmenite significantly squeezes titanium tetrachloride manufacturers’ profitability, feedstock costs can account for 55-65 % of total production costs, and ±20–40 % ore price swings directly compress margins and increase production uncertainties.

-

5. How is the trend toward lightweight materials in automotive manufacturing influencing titanium tetrachloride consumption for titanium components?The automotive shift to lightweight materials is increasing titanium use, driving titanium tetrachloride consumption up 12-15 %, as more titanium components replace steel and aluminum to improve fuel efficiency and EV range.

-

6. What is the impact of medical device industry growth on demand for high-purity titanium tetrachloride for biocompatible implants?Growth in the medical device industry is increasing demand for high-purity titanium tetrachloride for biocompatible implants, with consumption rising 18-22 %, driven by expanding orthopedic and dental implant markets requiring ultra-clean titanium metal.

Need help to buy this report?