Global Phosphonate Market Size, Share, and COVID-19 Impact Analysis, By Types (ATMP, HEDP, DTPMP, and Others), By End-user (Water Treatment, Detergent and Cleaning Agent, Oil Field Chemicals, Cosmetics, Building Materials, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Phosphonate Market Size Insights Forecasts to 2035

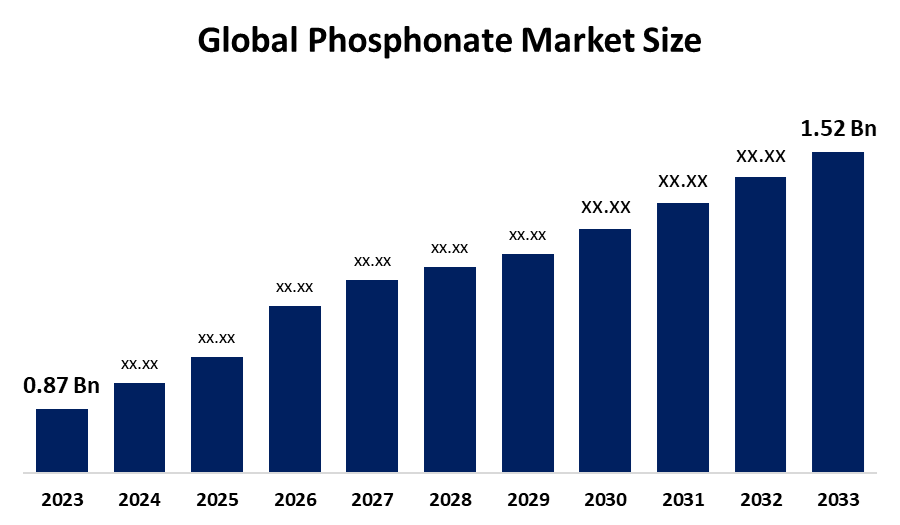

- The Global Phosphonate Market Size Was Estimated at USD 0.87 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 5.2% from 2025 to 2035

- The Worldwide Phosphonate Market Size is Expected to Reach USD 1.52 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a Research Report Published by Spherical Insights and Consulting, The Global Phosphonate Market Size was worth around USD 0.87 Billion in 2024 and is predicted to grow to around USD 1.52 Billion by 2035 with a compound annual growth rate (CAGR) of 5.2% from 2025 to 2035. The Phosphonate Market Size is expanding because industrial water treatment needs scale and corrosion control, together with oil and gas industry growth, and detergent usage of phosphonates. The water discharge regulations have become stricter while Asia-Pacific cities continue to grow rapidly, which creates increased water treatment needs.

Market Overview

Phosphonates belong to organophosphorus compounds, which contain phosphonic acid groups that serve as powerful agents for metal binding and the prevention of scale and corrosion. The molecular structure of these compounds enables them to create strong bonds with metal ions such as calcium and magnesium, which results in protection against scale formation and corrosion within industrial water systems. The most commonly used products on the market include HEDP, ATMP, PBTC and DTPMPA, which dominate North American markets because HEDP provides a cost-effective performance solution that accounts for 30 to 40% of total market share. Phosphonates find extensive application throughout power generation, oil and gas, chemical processing and detergent industries. The water treatment industry creates primary market demand because phosphonates function as essential components that protect pipes from both corrosion and metal leaching.

Governments worldwide invest heavily in water infrastructure development because global water shortages present major challenges. The U.S. Environmental Protection Agency announced in February 2024 that it will invest almost USD 6 billion to improve clean drinking water and wastewater systems. India's National River Conservation Plan designated about USD 75.47 billion in December 2022 for pollution control projects on 36 rivers, which will establish sewage treatment capacity of 2,745.7 million litres per day. The continuous usage of phosphonates in municipal and industrial treatment facilities directly results from these programs. Pro-drugs and nano-porous phosphonates represent new applications that will bring significant growth opportunities to the company.

Report Coverage

This research report categorizes the Phosphonate Market Size based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Phosphonate Market Size. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Phosphonate Market Size.

Phosphonate Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 0.87 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 5.2% |

| 2035 Value Projection: | USD 1.52 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 235 |

| Tables, Charts & Figures: | 120 |

| Segments covered: | By Types, By End-user |

| Companies covered:: | Italmatch Chemicals S.p.A., Solvay SA, Lanxess AG, BASF SE, Excel Industries Limited, Zschimmer & Schwarz Chemie GmbH, Aquapharm Chemicals Pvt. Ltd., Bozzetto Group, Mks DevO Chemical, Biesterfeld AG, Changzhou Kewei Fine Chemicals Co., Ltd., Nouryon Chemicals Holding B.V., Shandong IRO Water Treatment Co. Ltd, and other key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global Phosphonate Market Size is driven by rising demand in industrial water treatment, agriculture, and oil & gas sectors. Phosphonates serve as effective scale inhibitors and corrosion control agents, which become essential for cooling systems and desalination plants because the global industrial water treatment market has reached a value of more than USD 20 billion. Phosphonate-based agrochemicals in agriculture show increasing use because fertilizer consumption will exceed 190 million metric tons worldwide in 2024. The oil and gas industry expansion requires upstream investments, which will exceed USD 500 billion in 2024, which drives up demand for phosphonates. Phosphonate Market Size growth worldwide receives additional support because urbanization increases municipal treatment needs and wastewater regulations become stricter.

Restraining Factors

The global Phosphonate Market Size faces restrictions because European and North American environmental regulations create limits on phosphonate usage due to concerns about aquatic toxicity. The production costs increase because high raw-material expenses include phosphorous feedstocks, which experience annual price changes of 20 to 30%. The market growth faces challenges because these factors create difficulties for applications that require low costs.

Market Segmentation

The Phosphonate Market Size share is classified into types and end-user.

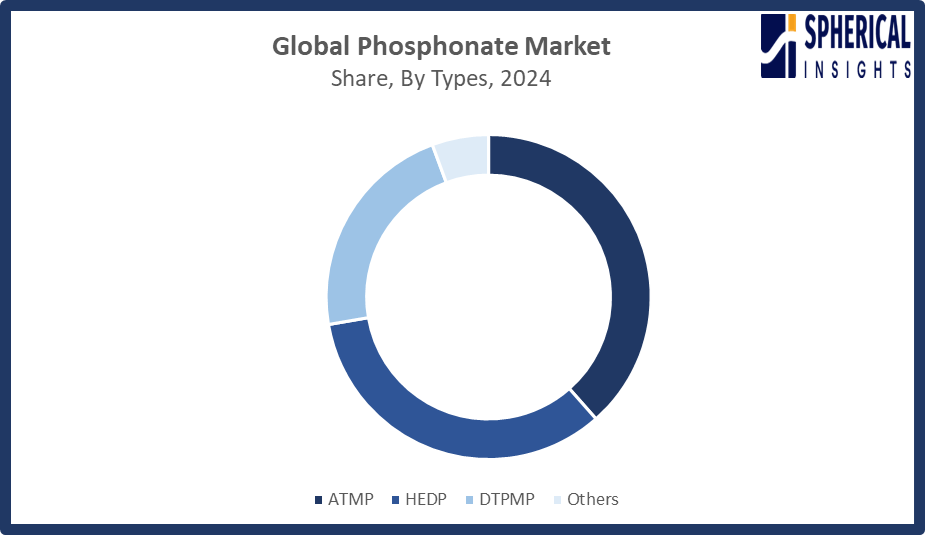

- The ATMP segment dominated the market in 2024, approximately 38% and is projected to grow at a substantial CAGR during the forecast period.

Based on the types, the Phosphonate Market Size is divided into ATMP, HEDP, DTPMP, and others. Among these, the ATMP segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The ATMP segment dominated market growth because it provides better chelating efficiency, together with its effective performance as a scale and corrosion inhibitor for industrial water treatment, oilfield chemicals and cleaning formulations. Power plants and petrochemical facilities prefer the product because it maintains stability during high temperature and alkaline conditions, which has led to its worldwide adoption in power plants and petrochemical facilities.

Get more details on this report -

- The water treatment segment accounted for the highest market revenue in 2024, approximately 44% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end-user, the Phosphonate Market Size is divided into water treatment, detergent and cleaning agent, oil field chemicals, cosmetics, building materials, and others. Among these, the water treatment segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The water treatment segment market growth is due to increasing industrialization, rising water scarcity, and stricter wastewater discharge regulations worldwide. The rising need for phosphonates as scale and corrosion inhibitors extended through power generation facilities, oil and gas operations, and manufacturing industries because of increasing municipal infrastructure development, desalination projects and cooling tower system installations.

Regional Segment Analysis of the Phosphonate Market Size

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the Phosphonate Market Size over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the Phosphonate Market Size over the predicted timeframe. In North America, the Phosphonate Market Size is anticipated to hold one of the largest shares in 2024, capturing approximately 45% of global revenue due to well-established industrial infrastructure and advanced water treatment systems. The United States dominates the market because it receives substantial government investment, which includes more than USD 50 billion from the Bipartisan Infrastructure Law for EPA water projects and almost USD 12 billion for the Clean Water State Revolving Fund. The demand for phosphonates increases because municipalities use them in their wastewater treatment systems, and industrial facilities use them in their cooling systems. The power generation sector, together with the oil and gas industry and wastewater treatment utilities, creates a strong demand for the regional market because these sectors continue to invest in modernization and sustainability projects.

Asia Pacific is expected to grow at a rapid CAGR in the Phosphonate Market Size during the forecast period. The Asia Pacific region will experience rapid growth in the Phosphonate Market Size because industrialisation, urbanisation, and water treatment facilities are expanding throughout China, India and Southeast Asia. China dominates the market as both the top consumer and producer because its market reached 129000 tons in 2024, driven by its extensive manufacturing capabilities, infrastructure development and strict environmental policies, which promote water treatment chemical usage. India’s investments in sewerage and river cleanup programs further support usage. The region's expanding detergent and chemical manufacturing industries will drive higher demand for phosphonates.

The growth of Europe's Phosphonate Market Size depends on strict environmental regulations, which require high-performance, compliant inhibitors for industrial water treatment and detergent applications. Germany, France and the UK establish sustainable chemical solutions as their main focus, which leads to increased use of eco-friendly phosphonate products. The regional market expansion receives additional support from ongoing infrastructure development and urban water management projects.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Phosphonate Market Size, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Italmatch Chemicals S.p.A.

- Solvay SA

- Lanxess AG

- BASF SE

- Excel Industries Limited

- Zschimmer & Schwarz Chemie GmbH

- Aquapharm Chemicals Pvt. Ltd.

- Bozzetto Group

- Mks DevO Chemical

- Biesterfeld AG

- Changzhou Kewei Fine Chemicals Co., Ltd.

- Nouryon Chemicals Holding B.V.

- Shandong IRO Water Treatment Co. Ltd

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In April 2026, the Chinese government introduced VAT export tax rebates on selected organic and inorganic phosphorus chemicals, including key raw materials for water treatment inhibitors. The policy is expected to raise production costs for phosphonate manufacturers, potentially reshaping export pricing, accelerating supply chain adjustments, and encouraging product innovation.

- In October 2025, LANXESS introduced Levagard 2100 at K 2025, a low-viscosity reactive phosphonate flame retardant. Unlike additive alternatives such as TCPP, it chemically bonds with polymers, enhancing mechanical strength and sustainability. Backwards-integrated phosphorus production in Germany strengthens supply security for polyurethane and engineering plastics applications.

- In November 2023, PCBL Ltd agreed to acquire Aquapharm Chemicals Pvt Ltd for Rs 38 billion ($456 million). Approved by the board and disclosed to the Bombay Stock Exchange, the deal marks PCBL’s entry into global water treatment and oilfield specialty chemicals markets.

- In October 2022, Italmatch Chemicals began construction of a new flame retardant production line in China, expanding its Phoslite range. Based on proprietary inorganic phosphinate technology developed in 2005, the expansion will increase capacity and support growing domestic and international demand across multiple high-performance applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Phosphonate Market Size based on the below-mentioned segments:

Global Phosphonate Market Size, By Types

- ATMP

- HEDP

- DTPMP

- Others

Global Phosphonate Market Size, By End-user

- Water Treatment

- Detergent and Cleaning Agent

- Oil Field Chemicals

- Cosmetics

- Building Materials

- Others

Global Phosphonate Market Size, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What role do phosphonates play as scale inhibitors in industrial water treatment and oilfield applications?Phosphonates chelate calcium and magnesium, reducing scale formation by over 90% in cooling systems and boilers. In oilfields, they extend equipment lifespan by 20-30% and lower maintenance costs by approximately 15% annually.

-

2. How do phosphonates contribute to energy efficiency in industrial processes by preventing scale formation?Phosphonates prevent calcium carbonate scale, maintaining heat-transfer efficiency by up to 95%. Studies show a 1 mm scale can raise energy use 7-10%, phosphonate treatment cuts fuel consumption 5-8% and reduces maintenance downtime nearly 15% annually.

-

3. What are the latest technological innovations in phosphonate production to reduce toxicity and improve environmental compatibility?Recent innovations include biodegradable phosphonate derivatives and enzyme-assisted synthesis, reducing aquatic toxicity by over 40% while maintaining performance. Green production methods also cut energy use and waste generation up to 30% compared to conventional processes.

-

4. How is the trend toward bio-based and sustainable chemicals influencing phosphonate product development?The shift to bio-based sustainable chemicals is driving the development of eco-friendly phosphonates, with green alternatives reducing carbon footprint up to 70% and aligning with stricter environmental standards in Europe and North America.

-

5. What impact is the global push for water conservation and recycling having on phosphonate consumption in cooling towers and boilers?The global push for water conservation and recycling is increasing phosphonate use in cooling towers and boilers, with global water reuse investments rising over 10% annually, driving efficiency and reducing scale-related downtime.

-

6. How are Chinese manufacturers expanding production capacities to dominate the global phosphonate supply chain?Chinese manufacturers are expanding phosphonate production capacity, some increasing output by 30-50%, to meet rising domestic and export demand, strengthen regional supply chains, and challenge Western producers in water treatment and industrial chemical markets.

-

7. What challenges do new entrants face in penetrating the technically demanding Phosphonate Market Size?New entrants face high R&D costs, complex production technologies, and strict environmental compliance, with barrier-to-entry expenditures often exceeding $10 million, limiting competition and slowing market penetration against established phosphonate producers.

-

8. What are the key strategic partnerships, mergers, and acquisitions shaping the competitive landscape?Key strategic moves shaping the Phosphonate Market Size include acquisitions such as PCBL’s $456 m buy of Aquapharm and Italmatch’s global expansion, strengthening water treatment portfolios and production capacity while driving sector consolidation and innovation.

Need help to buy this report?