Global Glacial Acetic Acid Market Size, Share, and COVID-19 Impact Analysis, By Grade (Food Grade, Industrial Grade, and Pharmaceutical Grade), By Application (Vinyl Acetate Monomer, Ester Production, Acetic Anhydride, Solvent, Food Additive, and Others), By End-Use (Chemicals and Petrochemicals, Food and Beverage, Pharmaceuticals, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Glacial Acetic Acid Market Insights Forecasts to 2035

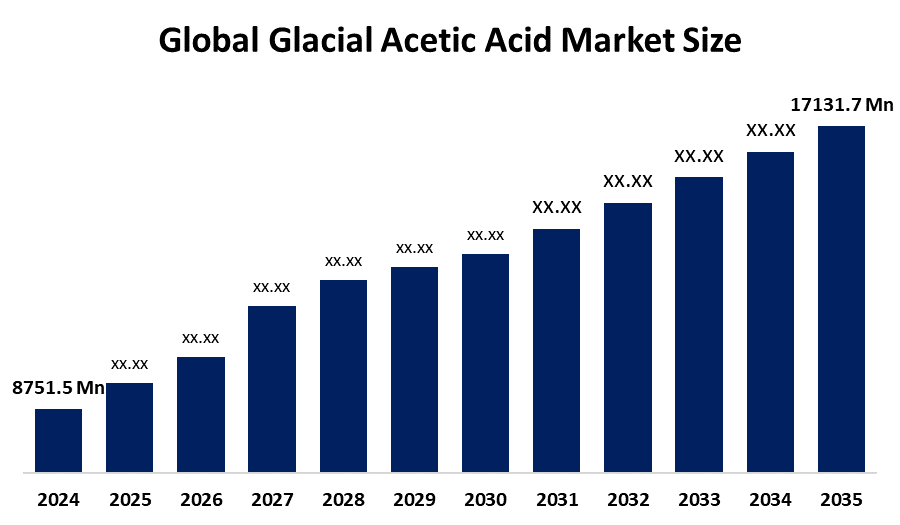

- The Global Glacial Acetic Acid Market Size Was Estimated at USD 8751.5 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 6.3% from 2025 to 2035

- The Worldwide Glacial Acetic Acid Market Size is Expected to Reach USD 17131.7 Million by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global glacial acetic acid market size was worth around USD 8751.5 million in 2024 and is predicted to grow to around USD 17131.7 million by 2035 with a compound annual growth rate (CAGR) of 6.3% from 2025 to 2035. The glacial acetic acid market is growing because downstream industries, which include polymers, adhesives, textiles and packaging materials, need more acetic acid to support their manufacturing operations and increasing demand in the chemical and PET markets throughout the Asia Pacific region.

Market Overview

Glacial acetic acid is a high-purity, water-free form of acetic acid, which serves as a primary chemical building block for producing vinyl acetate monomer, purified terephthalic acid, acetic anhydride and acetate esters. It serves as an essential component in the production of adhesives, paints, coatings, textiles, PET bottles, pharmaceuticals and food preservatives. The global glacial acetic acid market is expanding due to strong demand from the packaging, construction and automotive sectors. PTA accounts for nearly 45% of total acetic acid consumption, while VAM contributes around 30%, which shows strong demand from downstream markets.

Asia Pacific leads both production and consumption because of its extensive chemical manufacturing facilities located in China and India. The development of bio-based acetic acid and the growth of sustainable packaging applications create new market opportunities for businesses. In April 2025, China will begin operating 2.40 million tonnes per year of new glacial acetic acid capacity, which will start in the second quarter. The supply increase will exceed downstream demand growth, which will create market pressure and lead to price drops in the global acetic acid industry.

Report Coverage

This research report categorizes the glacial acetic acid market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the glacial acetic acid market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the glacial acetic acid market.

Global Glacial Acetic Acid Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 8751.5 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR Of 6.3% |

| 2035 Value Projection: | USD 17131.7 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 217 |

| Tables, Charts & Figures: | 121 |

| Segments covered: | By Grade,By Application,By End-Use |

| Companies covered:: | Celanese Corporation, INEOS Group Limited, Daicel Corporation, Eastman Chemical Company, Sinopec, LyondellBasell Industries Holdings B.V., SABIC, Jiangsu Sopo (Group) Co., Ltd., BP p.l.c., Mitsubishi Gas Chemical Company, Wacker Chemie AG, BASF SE, Formosa Plastics Corporation, Reliance Industries Ltd.,and Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global glacial acetic acid market exists because chemical manufacturing, textiles, plastics, and food industries require increasing amounts of glacial acetic acid. The substance acts as a vital ingredient for producing vinyl acetate monomer (VAM), purified terephthalic acid (PTA), and acetic anhydride. Acetic acid drives increased demand for adhesives and coatings and polyester fibers because the packaging, construction, and automotive industries experience growth. The expanding pharmaceutical and food preservation markets create additional demand for the product. The industrialization process moves forward in the Asia Pacific because China and India develop their production and trade activities. The market experiences ongoing expansion because petrochemical investments and chemical production growth continue to increase throughout the world.

Restraining Factors

The global glacial acetic acid market faces restraints from volatile raw material prices, which cause feedstock costs to rise by 15-20% throughout 2024. The industry faces growth limitations because environmental issues and strict regulations on emissions and capacity reductions from major manufacturers created supply shortages, which affected overall market development.

Market Segmentation

The glacial acetic acid market share is classified into grade, application, and end-use.

- The industrial grade segment dominated the market in 2024, approximately 67% and is projected to grow at a substantial CAGR during the forecast period.

Based on the grade, the glacial acetic acid market is divided into food grade, industrial grade, and pharmaceutical grade. Among these, the industrial grade segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The industrial grade segment dominated because it provides economical manufacturing solutions that work effectively for producing adhesives, textiles, and plastics in large-scale production. The high-purity product functions as the most economical option for bulk chemical production because it meets essential production standards without needing premium specifications.

- The vinyl acetate monomer segment accounted for the largest share in 2024, approximately 38% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the glacial acetic acid market is divided into vinyl acetate monomer, ester production, acetic anhydride, solvent, food additive, and others. Among these, the vinyl acetate monomer segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The vinyl acetate monomer (VAM) segment maintains its market leadership because of its dominant role in adhesive and paint production, sealant development, and coating application. The construction and packaging industries experience rapid growth in the Asia-Pacific region, which leads to high levels of VAM consumption. The market depends on its derivatives, which function as vital components for developing water-based emulsions and resins because they use glacial acetic acid.

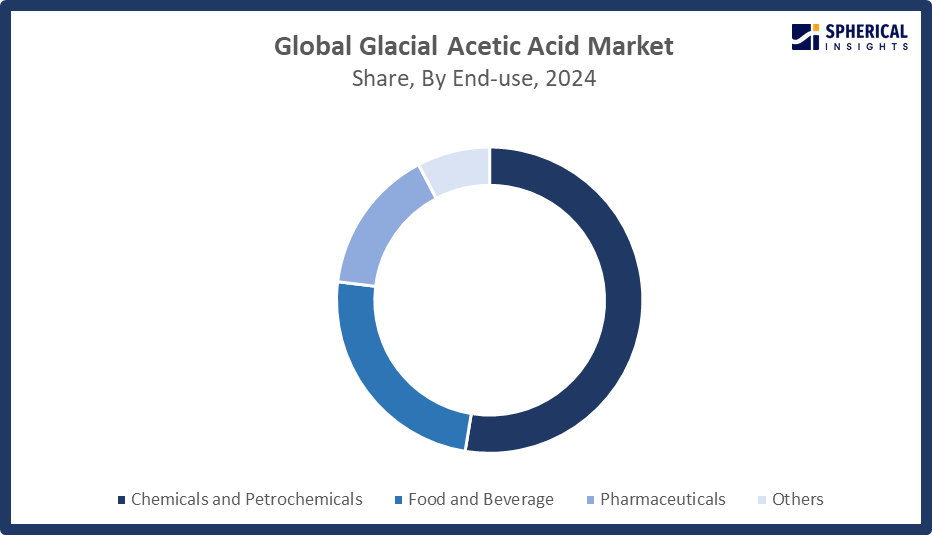

- The chemicals and petrochemicals segment accounted for the highest market revenue in 2024, approximately 53% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end-use, the glacial acetic acid market is divided into chemicals and petrochemicals, food and beverage, pharmaceuticals, and others. Among these, the chemicals and petrochemicals segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The acetic acid market received its main demand from the chemicals and petrochemicals segment, which needed the compound to produce vinyl acetate monomer (VAM) and purified terephthalic acid (PTA). The global industrial market needs these derivatives to produce paints and adhesives, packaging materials, and polyester fibers.

Get more details on this report -

Regional Segment Analysis of the Glacial Acetic Acid Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the glacial acetic acid market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the glacial acetic acid market over the predicted timeframe. The glacial acetic acid market will experience its maximum growth in the Asia Pacific region due to industrialization and the high demand from key end-use industries, which include textiles, packaging and chemical production. The region accounted for over 60% of global market volume as China leads production and consumption, supported by extensive downstream output of PTA and VAM. China dominates the market because it possesses extensive chemical production facilities and continues to develop its manufacturing capabilities, while India creates new demand through its growing polyester and manufacturing sectors. Asia Pacific maintains its top regional position because its industrial and chemical sectors continue to develop.

North America is expected to grow at a rapid CAGR in the glacial acetic acid market during the forecast period. The glacial acetic acid market in North America will experience a 25% share of rapid growth because of rising demand from the pharmaceuticals industry and food and beverage sector, coatings production and chemical manufacturing operations. The United States leads regional growth with strong consumption in VAM, PTA, and specialty chemicals, supported by expanding infrastructure and advanced production technologies that enhance market resilience. North America’s market growth occurs because companies use their existing products and develop new, environmentally friendly chemical solutions, which leads to consistent regional advancement.

Europe’s glacial acetic acid market growth results from the strong chemical and pharmaceutical industries, which drive high PTA and VAM demand. The countries of Germany and France consume the most products, which the packaging industry and specialty chemical sector both support. The European Union's sustainability regulations, which include the REACH revision scheduled for January 2026, improved chemical safety and risk management standards, which helped to control industrial chemical production and trade, including glacial acetic acid.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the glacial acetic acid market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Celanese Corporation

- INEOS Group Limited

- Daicel Corporation

- Eastman Chemical Company

- Sinopec

- LyondellBasell Industries Holdings B.V.

- SABIC

- Jiangsu Sopo (Group) Co., Ltd.

- BP p.l.c.

- Mitsubishi Gas Chemical Company

- Wacker Chemie AG

- BASF SE

- Formosa Plastics Corporation

- Reliance Industries Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In February 2026, Celanese Corporation announced price increases across the Western Hemisphere. Acetic acid will rise by USD v 50/USD 50 per metric ton, vinyl acetate monomer by USD 100/USD 100, acetic anhydride by USD 60/USD 60, and esters by USD 50/USD 50, effective immediately or as contracts permit.

- In November 2024, INEOS Acetyls and Gujarat Narmada Valley Fertilizers & Chemicals Ltd signed an MoU to explore building a 600 kt acetic acid plant in Bharuch, Gujarat. The joint venture aims to boost India’s domestic production and reduce import dependence, targeting launch by 2028.

- In May 2025, glacial acetic acid production is projected to reach 1,179,600 tonnes, up 18.58% month-on-month, according to OilChem. The surge is driven by the commissioning of 1.40 million tonnes per year of new capacity, the absence of planned outages, and stable operations across most production units.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the glacial acetic acid market based on the below-mentioned segments:

Global Glacial Acetic Acid Market, By Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

Global Glacial Acetic Acid Market, By Application

- Vinyl Acetate Monomer

- Ester Production

- Acetic Anhydride

- Solvent

- Food Additive

- Others

Global Glacial Acetic Acid Market, By End-Use

- Chemicals and Petrochemicals

- Food and Beverage

- Pharmaceuticals

- Others

Global Glacial Acetic Acid Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Need help to buy this report?