Amphibious Vehicle Market Summary

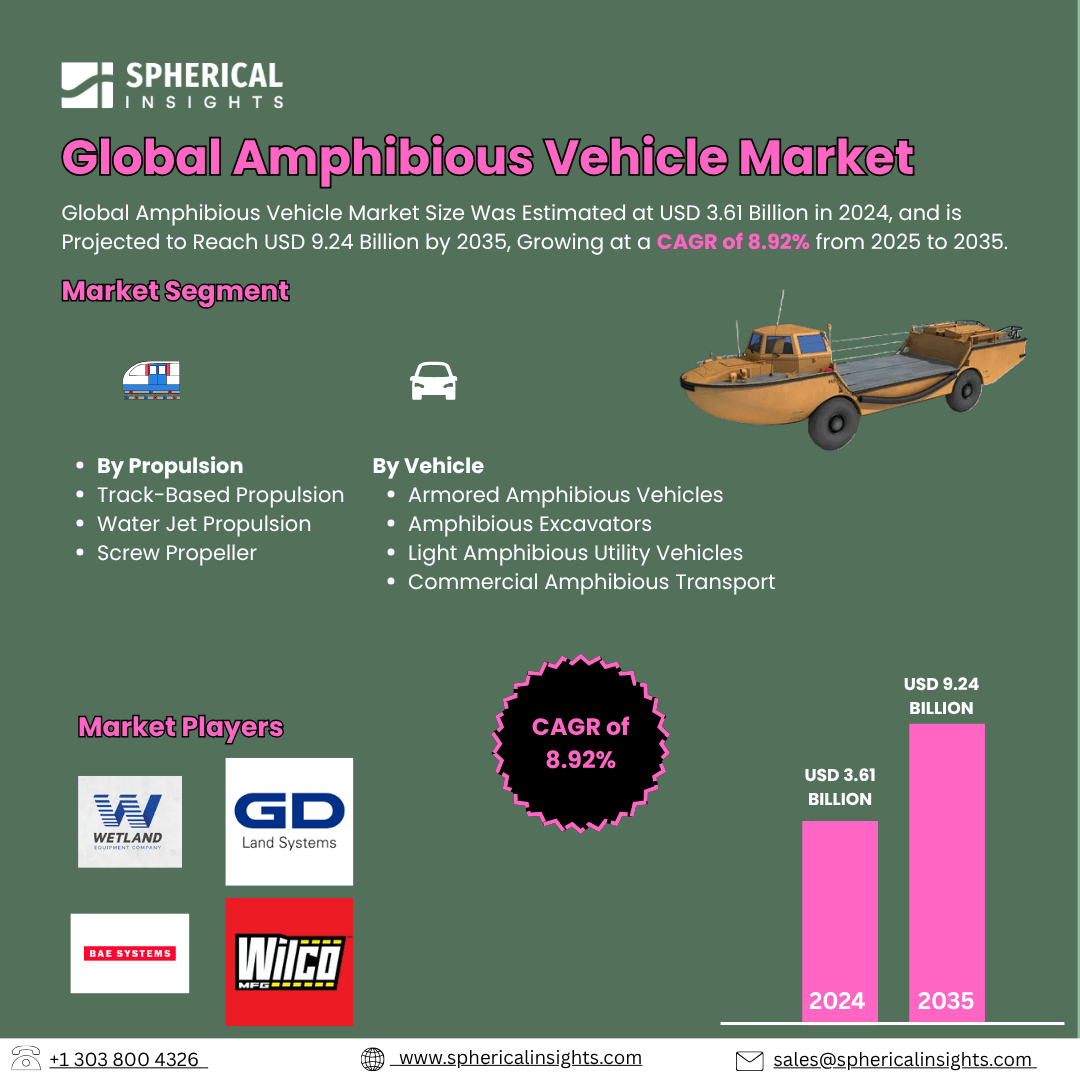

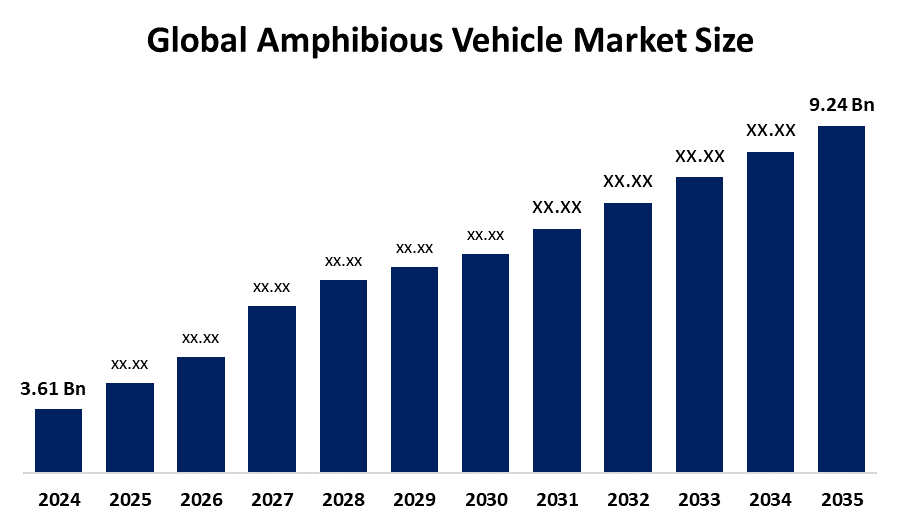

The Global Amphibious Vehicle Market Size Was Estimated at USD 3.61 Billion in 2024, and is Projected to Reach USD 9.24 Billion by 2035, Growing at a CAGR of 8.92% from 2025 to 2035. A number of factors are contributing to the growth of the amphibious vehicle market, such as the defense industry's growing demand for military modernization, the expansion of uses in commercial activities like tourism and transportation, and technological and material advancements.

Key Regional and Segment-Wise Insights

- In 2024, the amphibious vehicle market in North America accounted for the largest revenue share of 44.5% worldwide.

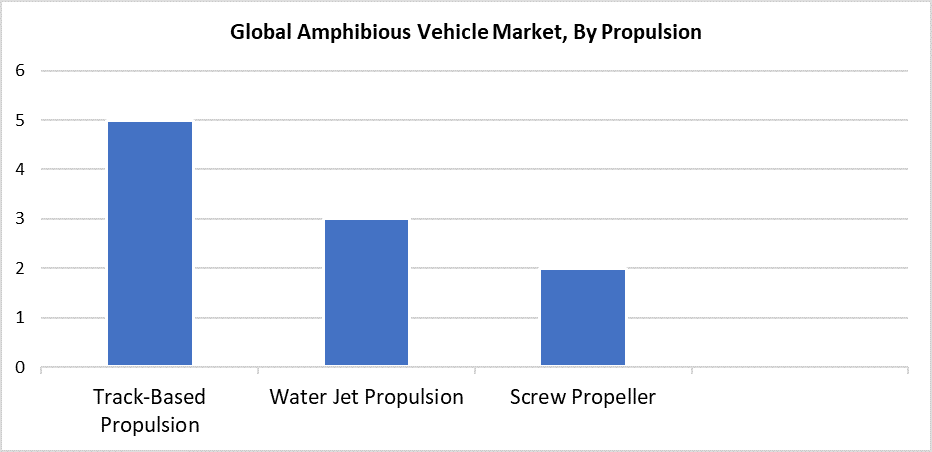

- With a 50.7% revenue share in 2024, the track-based propulsion sector led the market based on propulsion.

- In 2024, the armored amphibious vehicles segment led the market with the largest revenue share based on vehicles.

- The military combat & troop transport segment generated the highest revenue share in 2024 based on application.

Global Market Forecast and Revenue Outlook

- 2024 Market Size: USD 3.61 Billion

- 2035 Projected Market Size: USD 9.24 Billion

- CAGR (2025-2035): 8.92%

- North America: Largest market in 2024.

Amphibious vehicles form the core of the market, which specializes in vehicles that operate on both land and water. These versatile machines enable enhanced movement across different terrains like swamps, rivers, and coastal areas, and serve military forces as well as commercial operators and recreational users. The market expansion stems from primary factors, including the rising demand for advanced military tactical vehicles, increased deployment for rescue and disaster relief missions, and expanding interest in adventure tourism activities. Climate change and frequent flooding events have driven up the need for amphibious solutions in emergency services, along with civil defense operations. The worldwide market continues its steady growth because amphibious vehicles receive increased utilization by both military and civilian organizations.

Technological advancements that enhance payload capacity, together with speed, maneuverability, and fuel efficiency, are major forces driving the amphibious vehicle market. Electric and hybrid propulsion systems have gained popularity since they minimize environmental impact while extending operational range. Modern performance enhancement and durability improvement depend on using advanced materials, including lightweight composites. The increasing demand results from government initiatives that support infrastructure development alongside disaster preparedness programs and defense force modernization projects. The combination of public-private partnerships with targeted R&D funding has led nations to increase their investment in amphibious platforms, which creates favorable conditions for industrial development.

Propulsion Insights

The track-based propulsion category led the amphibious vehicles market with 50.7% revenue share in 2024. Track-based systems maintain exceptional traction and stability while offering excellent performance on difficult terrains like mud and sand, and wet conditions, which makes them highly suitable for military and rescue operations. Their load-carrying capacity, together with off-road mobility, makes these vehicles ideal for operations in remote areas and disaster-affected zones. Defense forces, together with emergency response teams across the world, continue to adopt these vehicles because they possess robust construction and operate effectively in challenging environments. The market leadership of track-based propulsion systems in 2024 stemmed from their proven reliability and operational efficiency, which attracted most customers.

During the forecast period, the amphibious vehicle market's water jet propulsion segment is anticipated to experience the fastest growth rate. Water jet propulsion systems provide several advantages, including superior maneuverability together with faster water speeds, and enhanced safety through propeller-free designs. The features of water jet propulsion systems make them most suitable for commercial vessels, search and rescue teams, and modern military units requiring fast water-to-land adaptability. The adoption of water jet technology continues to grow because of the increasing demand for versatile and high-performance amphibious vehicles. Research in lightweight construction and improved propulsion efficiency has driven this segment's rapid expansion across global defense and civilian markets.

Vehicle Insights

The armored amphibious vehicle segment held the largest revenue share of the amphibious vehicle market revenue in 2024 because of both rising defense expenditures throughout the world and rising requirements for advanced tactical mobility. These vessels serve as essential tools for contemporary military operations, including amphibious assaults, reconnaissance missions, and troop transport, because they deliver both defensive capabilities and offensive capabilities, operational flexibility across land and sea domains. The armed forces of North America, Europe, and Asia-Pacific have extensively embraced these vehicles because they operate effectively in demanding and difficult conditions. The strong demand exists because of increased funding for multifunctional combat vehicles combined with rising geopolitical conflicts and current defense modernization initiatives.

The commercial amphibious transport segment of the amphibious vehicle market will demonstrate significant CAGR during the forecast period. The expanding requirement for amphibious vehicles throughout travel operations, emergency response services, and tourism sectors represents the primary factor behind this market growth. The use of commercial amphibious vehicles continues to increase throughout coastal cities, island regions, and water-based tourist destinations for sightseeing, shuttle services, and adventure activities. Their seamless transition from land to water makes them ideal for locations with minimal infrastructure and frequent flood occurrences. The adoption of commercial amphibious vehicles is gaining pace in developed nations as well as emerging nations because of increasing environmental awareness toward innovative transport solutions, along with supportive coastal infrastructure development policies.

Application Insights

The military combat & troop transport sector led the amphibious vehicle market in 2024. The sector dominance is because military operations require adaptable platforms that can perform well on both land and water in difficult combat conditions. Military troops utilize amphibious vehicles for combat operations and transportation purposes because these vehicles enable rapid deployment while providing tactical superiority. These vehicles exist to transport personnel with their equipment, armaments across wetland areas, waterways, and oceanfront terrain. The market demand for these vehicles continues to grow because defense allocations increase, geopolitical tensions rise, and modernization programs expand across primary economic regions. The market segment dominance arises because these vehicles perform essential duties in border surveillance missions as well as in humanitarian rescue operations and water-based military attacks.

The commercial and recreational transport segment is anticipated to grow at the fastest CAGR throughout the forecast period. The main factor driving this market growth emerges from growing consumer interest in vehicles that adjust to land and water environments, particularly within coastal and water-abundant locations. The main advantage of amphibious vehicles allow them to transition smoothly from land to water operations. The vehicles find widespread application in sightseeing tours, along with water-based leisure activities and emergency transportation for flood-prone locations and islands. The segment achieves promising growth because of increasing consumer income levels along with expanding awareness about eco-friendly travel and vital applications in commercial emergency response and disaster relief. This growing pattern receives additional support through both infrastructure development and government backing measures.

Regional Insights

The North American amphibious vehicle market held the largest revenue share of 44.5% in 2024 because of strong defense funding combined with advanced technology and established manufacturing facilities. Troop transport vehicles and amphibious combat units receive substantial funding from regional military forces to enhance their operational adaptability across different terrains. The defense industry continues to grow because of major defense corporations operating in the region, along with advancements in armor, propulsion, and navigation technologies. The rising application of amphibious vehicles in search and rescue, alongside emergency response and commercial sectors, drives additional market demand. The North American market secured its top position for amphibious vehicles in 2024 through favorable governmental regulations as well as extensive infrastructure development and ongoing modernization programs.

Asia Pacific Amphibious Vehicle Market Trends

The Asia Pacific amphibious vehicle market accounted for a substantial market share in 2024 because of rapid military modernization, together with increasing defense expenditures and expanding demand for multi-purpose vehicles in commercial and disaster response operations. The armed forces of China, India, Japan, and South Korea invest heavily in advanced amphibious systems to enhance their operational capabilities across multiple environments, including rivers and coastal areas. The increasing use of amphibious vehicles for rescue and relief operations stems from the region's frequent exposure to natural disasters such as floods and tsunamis. The Asia Pacific region maintains strong amphibious vehicle market prospects in 2024 because of expanding infrastructure development alongside growing industrial activities and enhanced government backing for defense and disaster readiness.

Europe Amphibious Vehicle Market Trends

The European amphibious vehicle market demonstrated strong profitability potential in 2024 because of increased defense modernization programs and high-tech military equipment investments. European countries focus on developing their amphibious capabilities to support operations across multiple terrains and quick deployment and coastal defense missions. The heightened necessity for amphibious vehicles in civilian operations stems from European nations' enhanced focus on emergency management and disaster response capabilities. The development of armor and propulsion systems, and adaptable vehicles, progresses faster because of governmental partnerships with leading defense manufacturing companies. Europe's amphibious vehicle market grow significantly during 2024 because of beneficial legislation combined with escalating international conflicts.

Key Amphibious Vehicle Companies:

The following are the leading companies in the amphibious vehicle market. These companies collectively hold the largest market share and dictate industry trends.

- BAE Systems plc

- Wetland Equipment Company

- General Dynamics Corporation

- Wilco Manufacturing L.L.C.

- Rheinmetall AG

- Hydratrek, Inc.

- Hitachi Construction Machinery Co., Ltd.

- Hanwha Aerospace

- Marsh Buggies Incorporated

- EIK Engineering Sdn. Bhd.

- Others

Recent Developments

- In April 2025, the U.S. Marine Corps awarded BAE Systems a USD 188.5 million contract for 30 ACV-30mm vehicles, including fielding support and replacement parts. Ship-to-shore and advanced land operations are supported by the ACV-30, which has a 30mm remote turret.

- In February 2025, BAE Systems unveiled the Amphibious Combat Vehicle (ACV), during the UAE's IDEX defense show. With its design for open-ocean amphibious operations and rough terrain, the ACV emphasizes the program's objective of global expansion and increased operational flexibility for allied military across the globe.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the amphibious vehicle market based on the below-mentioned segments:

Global Amphibious Vehicle Market, By Propulsion

- Track-Based Propulsion

- Water Jet Propulsion

- Screw Propeller

Global Amphibious Vehicle Market, By Vehicle

- Armored Amphibious Vehicles

- Amphibious Excavators

- Light Amphibious Utility Vehicles

- Commercial Amphibious Transport

Global Amphibious Vehicle Market, By Application

- Military Combat & Troop Transport

- Disaster Response & Humanitarian Aid

- Construction & Dredging

- Commercial & Recreational Transport

Global Amphibious Vehicle Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa