Global Water and Wastewater Management for the Mining Market Size, Share, and COVID-19 Impact Analysis, By Mine Type (Coal Mining, Metal Mining, Non -Metal Mining, and Industrial Minerals Mining), By Process Type (Water Treatment, Wastewater Treatment, Water Recycling and Reuse, and Sludge Management), By End Use (Process Water, Dust Suppression, Mine Dewatering, Tailings Management, and Drinking Water Supply), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Water and Wastewater Management for the Mining Market Insights Forecasts to 2035

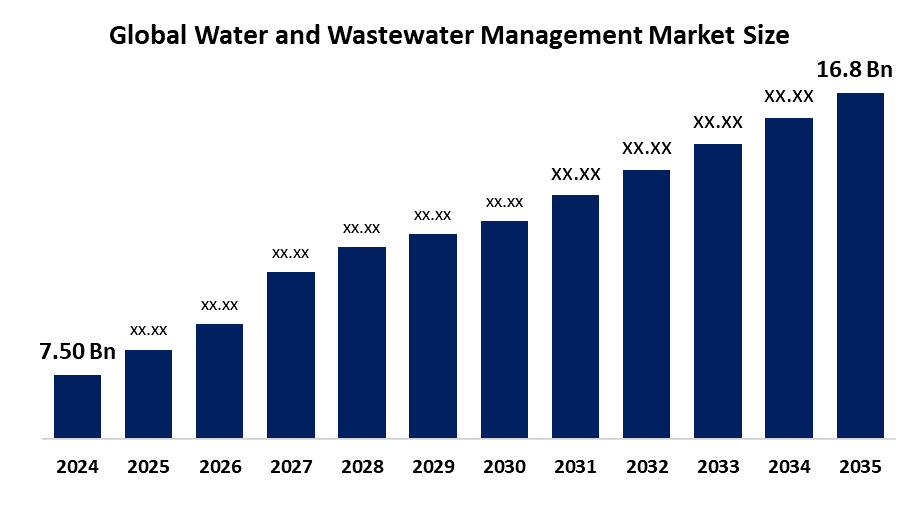

- The Global Water and Wastewater Management for the Mining Market Size Was Estimated at USD 7.50 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 7.61% from 2025 to 2035

- The Worldwide Water and Wastewater Management for the Mining Market Size is Expected to Reach USD 16.8 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global water and wastewater management for the mining market size was worth around USD 7.50 billion in 2024 and is predicted to grow to around USD 16.8 billion by 2035 with a compound annual growth rate CAGR of 7.61% from 2025 to 2035. The mining market for water and wastewater management continues to grow because of stricter environmental rules, increasing water shortages and the higher demand for minerals that need water for their processing. This drives mines to adopt advanced treatment and recycling technologies to ensure operational sustainability.

Market Overview

Global water and wastewater management in the mining industry encompasses technologies and services that treat recycle and manage water used across mining operations. Mining consumes substantial water for ore extraction mineral processing and dust suppression thereby generating wastewater that contains heavy metals chemicals and suspended solids Efficient water management not only ensures compliance with environmental regulations but also reduces operational costs and minimises ecological impacts. In January 2026 Saudi Arabias Ministry of Industry and Mineral Resources in collaboration with MODON and SIO launched and rare earth operations and develops shared infrastructure aligned with Vision

Market growth is fueled by rising water scarcity with over 40 of the global population experiencing water stress driving mining companies to adopt efficient treatment recycling and reuse solutions Stricter government regulations on wastewater discharge and heavy metal contamination further accelerate demand, ensuring ecosystem protection. Advanced technologies including reverse osmosis zero liquid discharge systems and IoT enabled monitoring enhance water recovery and operational efficiency. Opportunities exist in deploying membrane filtration automation, and AI based monitoring to optimize treatment at remote or legacy mine sites reducing costs. In July 2025 Indias Ministry of Coal along with CIL NLCIL and SCCL promoted the use of treated mine water for drinking irrigation and industrial purposes following CPCB standards and BIS IS expanding safe water utilization across mining regions nationwide

Water and Wastewater Management for the Mining Market Growth Factors

- Increasing global mining activities: Expansion of mining for metals like copper, lithium, and cobalt has raised water consumption and wastewater production. In 2024, global mineral extraction reached over 17 billion tons, highlighting the growing demand for effective water and wastewater management solutions.

- Corporate ESG and sustainability commitments: Mining companies are adopting stricter environmental, social, and governance ESG standards, emphasizing water efficiency and wastewater recycling. Reports indicate over 75 of major mining firms now disclose water management practices, fueling investments in treatment and monitoring systems.

- Advancements in treatment technologies: Innovations such as membrane bioreactors, electrocoagulation, and AI-driven water optimization enhance efficiency and reduce costs. Adoption of membrane-based water treatment is growing at 12 annually, enabling higher water reuse rates and improved operational sustainability.

Report Coverage

This research report categorizes the water and wastewater management for the mining market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the water and wastewater management for the mining market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the water and wastewater management for the mining market.

Global Water and Wastewater Management for the Mining Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 7.50 billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 7.61% |

| 2035 Value Projection: | USD 16.8 billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 90 |

| Segments covered: | By Mine Type,By Process Type |

| Companies covered:: | Veolia,Evoqua,SUEZ,Xylem,DuPont,Aquatech And Others Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis Pitfalls & Challenges |

Get more details on this report -

Driving Factors

The global water and wastewater management for the mining market operates because of rising water shortages, strict environmental regulations and increasing sustainability efforts. Mining operations consume vast amounts of water, and companies are adopting efficient water recycling and treatment solutions because global freshwater stress affects 40 of the population. The need for advanced treatment technologies such as reverse osmosis systems and zero liquid discharge systems increases because of strict regulations that prohibit wastewater discharge and heavy metal contamination. Market growth throughout the mining industry advances because IoT based monitoring systems and hybrid filtration systems enable organizations to optimize their water reuse practices while decreasing operational expenses and achieving their environmental, social, and governance standards. In August 2024, Indias Ministry of Coal announced plans to rejuvenate 500 water bodies in coal and lignite mining areas by 2029 using treated mine water for drinking, irrigation, fish farming, and groundwater recharge, benefiting communities and the environment.

Restraining Factors

The global mining industry faces obstacles in water and wastewater management because treatment processes and infrastructure maintenance require significant financial investments, because mine site conditions present operational challenges, and because there is a shortage of qualified personnel. The treatment system expenses reach 30 40 of operational budgets, which results in increased compliance costs under stringent regulations, and this situation hampers smaller mining operations from adopting new technologies.

Market Segmentation

Mine Type Insights

The metal mining dominated the water and wastewater management for the mining market with the 45 market share, because metal extraction and processing activities for resources such as copper gold and lithium require substantial water usage. This segment represents nearly 40 of total mining water consumption, producing significant volumes of contaminated wastewater that require advanced treatment and recycling solutions.

The industrial minerals mining segment is the fastest growing segment with a significant CAGR during the forecast period. This growth is driven by the rising demand for minerals, including phosphate, potash, and limestone. Worldwide industrial mineral production exceeds 9 billion tonnes annually, increasing the need for efficient water treatment and recycling systems.

Process Type Insights

The wastewater treatment dominated the market with the 42 market share, due to the large volume of contaminated effluent generated during mineral extraction and processing. Mining operations can produce thousands of cubic meters of wastewater daily, and stricter discharge regulations drive the adoption of advanced treatment technologies to remove heavy metals and pollutants.

The water recycling and reuse segment is the fastest growing segment with a significant CAGR during the forecast period, as water scarcity and sustainability targets encourage mining companies to reuse treated water. Recycling technologies can help operations cut freshwater consumption by 30 40, lowering costs and environmental impact.

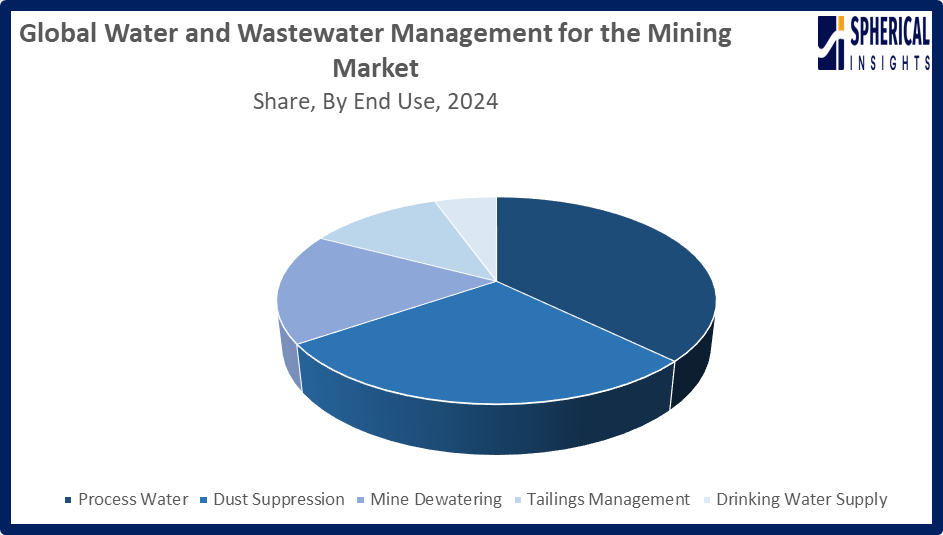

End Use Insights

The process water segment dominated the market with the 37 market share, because of the extensive water requirements in mineral processing activities such as grinding, flotation, and separation. Mining operations can consume up to 47 m³ of water per tonne of ore processed, increasing demand for treatment, recycling, and efficient water management systems.

The tailings management segment is the fastest growing segment for the foreseen period, due to the rising generation of mining waste and stricter environmental standards. Large-scale mines can generate more than 200,000 tonnes of tailings per day, increasing the need for advanced water treatment and tailings water recovery systems.

Get more details on this report -

Regional Segment Analysis of the Water and Wastewater Management for the Mining Market

- North America U.S Canada, Mexico

- Europe Germany, France, U.K. Italy, Spain, Rest of Europe

- Asia-Pacific China, Japan, India, Rest of APAC

- South America Brazil and the Rest of South America)

- The Middle East and Africa UAE, South Africa, Rest of MEA

Asia Pacific Market Trends

Asia Pacific dominated the water and wastewater management for the mining market with the 38 market share, driven by extensive mineral extraction activities and increasing environmental regulations in key countries such as China, Australia, and India. The region contributes nearly of global mining output, which significantly increases water demand for mineral processing and extraction operations. China alone accounts for more than half of global rare earth mineral production, while Australia remains a major exporter of iron ore and lithium. Growing industrial development, stricter environmental policies, and rising water scarcity in mining areas are encouraging companies to adopt advanced wastewater treatment, recycling, and reuse solutions. In March 2024, Chinas National Development and Reform Commission introduced a directive to raise mine water utilization in the Yellow River Basin above 68 by 2025 through advanced treatment technologies and fiscal incentives supporting circular resource management.

India Water and Wastewater Management for the Mining Market Trends

Indias water and wastewater management market for mining is expanding steadily due to rising mining operations stricter environmental norms, and growing water scarcity. Government initiatives promoting treated mine water reuse and compliance with Central Pollution Control Board standards encourage the adoption of advanced treatment and recycling technologies.

North America Market Trend

Get more details on this report -

North America is the fastest growing market for water and wastewater management for mining, with an approximate 25 share, due to expanding mineral production and stringent environmental regulations. The United States and Canada are increasing investments in sustainable mining and water treatment infrastructure. According to the US. Geological Survey the U.S. produced minerals worth over 100 billion in 2023, increasing water management requirements. Strict regulations enforced by the US. Environmental Protection Agency on wastewater discharge and heavy-metal contamination are driving the adoption of advanced technologies such as membrane filtration, recycling, and zero-liquid-discharge systems across mining operations.

U.S. Water and Wastewater Management for the Mining Market Trends

The U.S. market is growing due to stricter environmental regulations, increasing mining activities, and rising adoption of advanced water treatment technologies. Mining companies are investing in water recycling systems and digital monitoring solutions to reduce freshwater consumption, manage wastewater effectively, and meet sustainability and environmental compliance requirements.

Europe Water and Wastewater Management for the Mining Market Trends

Europe’s water and wastewater management market for mining is growing steadily, supported by strict environmental regulations, sustainability goals, and technological progress. The region represents nearly 30 of global water and wastewater treatment revenue, backed by strong regulatory systems and infrastructure investments. Policies such as the Water Framework Directive require mining and other industries to maintain high water-quality standards. In 2023, industrial water abstraction in the European Union reached about 29.1 billion cubic meters, increasing demand for advanced treatment and recycling solutions. In January 2026 the European Commission will issue new Water Framework Directive guidance and revise permitting rules to accelerate critical raw material mining. The Metal Mining BREF questionnaire, released in March, collects data for EU wide emission standards, while the Environmental Omnibus package eases water related permits for strategic projects.

U.K. Water and Wastewater Management for the Mining Market Trends

The U.K. water and wastewater management market for mining is growing due to strict environmental regulations and increasing adoption of sustainable water practices. Regulatory frameworks such as the UK Environmental Permitting Regulations 2016 require strict control of industrial wastewater discharge. Additionally, guidance from the Environment Agency encourages mining operators to implement advanced treatment and water recycling technologies to improve efficiency and environmental compliance.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations companies involved within the water and wastewater management for the mining market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Veolia

- Evoqua

- SUEZ

- Xylem

- DuPont

- Aquatech

- BQE

- Pentair

- Larsen

- Thermax

- KSB

- Fluence

- Jacobs

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026, DuPont Water Solutions expanded its WAVE PRO modeling platform with reverse osmosis and nanofiltration capabilities. The upgraded software integrates and technologies, enabling water professionals to design and simulate efficient treatment systems for drinking water, industrial water, wastewater, and desalination applications.

- In February 2026, Veolia strengthened its presence in India by securing major contracts for two large water treatment plants in Mumbai. Developed with Welspun Enterprises Ltd, the Bhandup and Panjrapurfacilities will supply over 60 of the citys water demand by 2030.

- In January 2026, Chinas National Standardization Committee launched the Technical Guide for Mine Water Quality Treatment and Graded Utilization setting standards to treat and reuse mine water, supporting the 68 utilization target in the Yellow River basin.

- In January 2026, Jacobs was selected to upgrade the San Jose Santa Clara Regional Wastewater Facility in California, United States. The 200 million project will modernize biosolids infrastructure, replace mesophilic digesters, and add a FOG receiving station to boost biogas energy production and reduce emissions.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the water and wastewater management for the mining market based on the below-mentioned segments:

Global Water and Wastewater Management for the Mining Market, By Mine Type

- Coal Mining

- Metal Mining

- Non-Metal Mining

- Industrial Minerals Mining

Global Water and Wastewater Management for the Mining Market, By Process Type

- Water Treatment

- Wastewater Treatment

- Water Recycling and Reuse

- Sludge Management

Global Water and Wastewater Management for the Mining Market, By End Use

- Process Water

- Dust Suppression

- Mine Dewatering

- Tailings Management

- Drinking Water Supply

Global Water and Wastewater Management for the Mining Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. How is rising global mineral extraction influencing the demand for advanced water and wastewater management solutions in the mining industry?Rising global mineral extraction drives demand for advanced water and wastewater management as mining produces vast effluents; in 2023, global copper and lithium mining consumed over 500,000 liters of water per tonne, increasing treatment and recycling adoption.

-

2. What role does water scarcity play in accelerating wastewater recycling and reuse technologies in mining operations?Water scarcity accelerates wastewater recycling in mining, as over 40% of the global population faces water stress. Mines reuse treated water, reducing freshwater consumption by 30-40%, supporting sustainability and operational efficiency.

-

3. How are stricter environmental regulations affecting investment in mining water treatment technologies worldwide?Stricter environmental regulations drive global investment in mining water treatment. In 2023, compliance with heavy metal discharge limits prompted mining companies to adopt advanced systems, contributing to a $5.5-7.9 billion market.

-

4. What impact does sustainable water management have on the environmental footprint of large-scale mining projects?Sustainable water management reduces mining’s environmental footprint by recycling up to 40% of freshwater, lowering contaminated discharge. Large-scale mines producing over 200,000 tonnes of tailings daily minimize ecosystem damage and regulatory penalties.

-

5. How are innovations such as membrane filtration, zero liquid discharge, and digital monitoring transforming water management in mining?Innovations like membrane filtration, zero-liquid-discharge, and digital monitoring enhance mining water management by recovering 30-40% of freshwater, reducing wastewater discharge, and improving efficiency in operations producing thousands of cubic meters of effluent daily.

-

6. What is the economic impact of water recycling and reuse systems on mining operational costs?Water recycling and reuse systems reduce mining operational costs by 15-25%, cutting freshwater procurement and wastewater treatment expenses. Large mines consuming millions of cubic meters annually benefit from improved efficiency and regulatory compliance.

Need help to buy this report?