United Kingdom General Surgery Devices Market Size, Share, By Type (Disposable Surgical Supplies, Surgical Non-woven, General Surgery Procedural Kits, Examination and Surgical Gloves, Venous Access Catheters, Needle and Syringes, Energy-based and Powered Instrument, Drill System, Powered Staplers, Minimally Invasive Surgery Instruments, Laparoscope, Organ Retractor, Adhesion Prevention Products, Open Surgery Instrument, Catheters, Dilator, and Others), By Application (Thoracic Surgery, Urology and Gynecology Surgery, Orthopedic Surgery, Ophthalmology Surgery, Plastic Surgery, Cardiology, Wound Care, Audiology, Neuro Surgery, and Other Application), By End Use (Hospitals, Ambulatory Surgical Centers, and Specialty Clinic), and United Kingdom General Surgery Devices Market Insights, Industry Trend, Forecasts to 2035

Industry: HealthcareUnited Kingdom General Surgery Devices Market Insights Forecasts to 2035

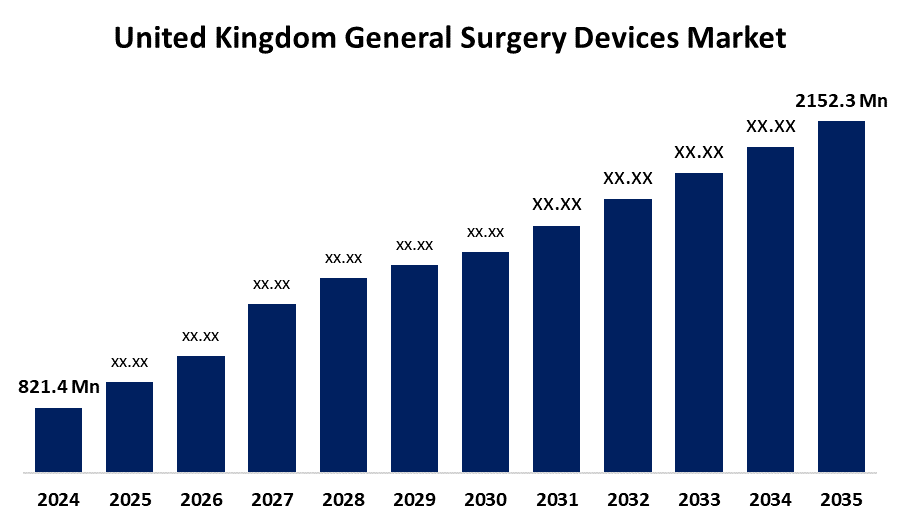

- United Kingdom General Surgery Devices Market Size 2024: USD 821.4 Mn

- United Kingdom General Surgery Devices Market Size 2035: USD 2152.3 Mn

- United Kingdom General Surgery Devices Market CAGR: 9.15%

- United Kingdom General Surgery Devices Market Segments: Type, Application, and End Use

Get more details on this report -

The market for general surgery instruments in the UK is growing gradually, due to an older population, chronic illnesses, and trauma cases that are driving increasing surgical volumes. With its high volume of elective and emergency treatments, the NHS continues to be the largest end-user, driving demand for a wide range of devices, including disposable supplies, less invasive instruments, energy-based systems, and sophisticated visualization tools. Modern operating rooms, increased surgical capacity, and shorter wait times are the goals of NHS England's and devolved health authorities' ongoing investments in healthcare infrastructure and strategic procurement efforts. Continuous investments in healthcare infrastructure and strategic procurement initiatives by NHS England and devolved health authorities aim to modernize operating theatres, enhance surgical capacity, and reduce waiting times.

The United Kingdom general surgery devices market growth is significantly shaped by government efforts. infection control, cost-effective care delivery, and better surgical results are given top priority in the United Kingdom government and NHS programs. To improve procedural efficiency and patient safety, public health funding encourages the use of cutting-edge surgical technologies and clinical training initiatives. Outside of conventional hospital settings, initiatives supporting outpatient care and ambulatory surgery centers also increase demand for devices.

The terrain is changing due to technological improvements. Robotic-assisted surgery, improved laparoscopic systems, AI-integrated surgical planning, and smart energy devices are examples of innovations that increase precision, shorten recovery times for patients, and increase the number of conditions that may be treated. Intraoperative guiding and procedure precision are improved by the use of modern imaging and computerized surgical platforms. The UK general surgical devices industry has a promising future thanks to favorable legislative frameworks and quick technology advancements.

United Kingdom General Surgery Devices Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 821.4 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR Of 9.15% |

| 2035 Value Projection: | USD 2152.3 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 230 |

| Tables, Charts & Figures: | 140 |

| Segments covered: | By Type,By Application,By End Use |

| Companies covered:: | Medtronic plc Johnson & Johnson (Ethicon) Stryker Corporation Boston Scientific Corporation B. Braun Melsungen AG Smith & Nephew plc Zimmer Biomet Holdings Olympus Corporation Intuitive Surgical, Inc. ConvaTec Group plc Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Market Dynamics of the United Kingdom General Surgery Devices Market:

A major driver of market expansion is the aging population and rising incidence of chronic diseases, which are driving an increase in the volume of surgical procedures performed. Demand for cutting-edge surgical equipment, energy-based gadgets, and disposable supplies has surged due to the increasing use of robotically assisted and minimally invasive procedures. Demand is further stimulated by the NHS's ongoing expenditures in hospital infrastructure, upgrading of operating rooms, and emphasis on cutting surgical backlogs. Additionally, the usage of single-use surgical instruments and supplies is increasing due to stringent infection prevention and control regulations.

The high cost of sophisticated surgical technologies, such as robotic platforms and powered tools, can restrict adoption, particularly in smaller healthcare facilities, despite the market's promising development potential. Budgetary constraints within the NHS, coupled with procurement delays, may slow technology upgrades. Moreover, supply chain disruptions and dependence on imported components can impact device availability and pricing.

The growth of ambulatory surgical facilities, the trend toward day care and outpatient procedures, and the growing need for affordable, minimally invasive treatments all create substantial prospects for the market. Strong innovation potential is provided by technological developments, including AI-assisted surgery, enhanced visualization systems, and smart energy gadgets. Furthermore, it is anticipated that expanding public-private collaborations and surgeon training programs may hasten the UK's adoption of cutting-edge general surgery equipment.

Market Segmentation

The United Kingdom general surgery devices market share is classified into type, application, and end use.

By Type:

On the basis of type, the United Kingdom general surgery devices market is categorized into disposable surgical supplies, surgical non-woven, general surgery procedural kits, examination and surgical gloves, venous access catheters, needle and syringes, energy-based and powered instrument, drill system, powered staplers, minimally invasive surgery instruments, laparoscope, organ retractor, adhesion prevention products, open surgery instrument, catheters, dilator, and others. Among these, the disposable surgical supplies segment held the majority market share in 2024 and is predicted to grow at a remarkable rate during the predicted period. The enormous number of surgical procedures performed in both NHS and commercial hospitals, stringent infection prevention and control protocols, and the single-use nature of many consumables, including drapes, gowns, sutures, and syringes, are the main causes of this dominance.

By Application:

Based on the application, United Kingdom general surgery devices market is divided into thoracic surgery, urology and gynecology surgery, orthopedic surgery, ophthalmology surgery, plastic surgery, cardiology, wound care, audiology, neurosurgery, and other applications. Among these, the orthopedic surgery segment accounted for the largest market share in 2024 and is expected to grow at a significant rate of CAGR during the projected period. The high incidence of musculoskeletal problems, an aging population, and an increase in joint replacement and trauma-related surgeries in the UK are the main factors contributing to orthopedic surgery's dominance.

By End Use:

The United Kingdom general surgery devices market is classified by end use into hospitals, ambulatory surgical centers, and specialty clinics. Among these, the hospitals segment held the largest market share in 2024 and is expected to grow at a remarkable CAGR during the forecast period. The huge number of surgeries carried out in NHS and private hospitals, the accessibility of cutting-edge surgical equipment, and the presence of qualified surgeons and interdisciplinary care teams are the main factors contributing to this domination. The demand for a variety of general surgery instruments is raised by hospitals' early adoption of cutting-edge surgical technologies, such as robotically assisted and minimally invasive procedures.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the United Kingdom general surgery devices market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in the United Kingdom General Surgery Devices Market:

- Medtronic plc

- Johnson & Johnson (Ethicon)

- Stryker Corporation

- Boston Scientific Corporation

- B. Braun Melsungen AG

- Smith & Nephew plc

- Zimmer Biomet Holdings

- Olympus Corporation

- Intuitive Surgical, Inc.

- ConvaTec Group plc

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the United Kingdom, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the United Kingdom general surgery devices market based on the following segments:

United Kingdom General Surgery Devices Market, By Type

- Disposable Surgical Supplies

- Surgical Non-woven

- General Surgery Procedural Kits

- Examination and Surgical Gloves

- Venous Access Catheters

- Needle and Syringes

- Energy-based and Powered Instrument

- Drill System

- Powered Staplers

- Minimally Invasive Surgery Instruments

- Laparoscope

- Organ Retractor

- Adhesion Prevention Products

- Open Surgery Instrument

- Catheters, Dilator

- Others

United Kingdom General Surgery Devices Market, By Application

- Thoracic Surgery

- Urology and Gynecology Surgery

- Orthopedic Surgery

- Ophthalmology Surgery

- Plastic Surgery

- Cardiology

- Wound Care

- Audiology

- Neurosurgery

- Other Applications

United Kingdom General Surgery Devices Market, By End Use

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinic

Frequently Asked Questions (FAQ)

-

1. What is the market size and growth outlook for the UK general surgery devices market?The market was valued at USD 821.4 million in 2024 and is projected to reach USD 2,152.3 million by 2035, growing at a CAGR of 9.15% during the forecast period (2025–2035).

-

2. What factors are driving the growth of the UK general surgery devices market?Key growth drivers include an aging population, rising prevalence of chronic diseases, increasing surgical procedure volumes, adoption of minimally invasive and robotic-assisted surgeries, and continuous NHS investments in surgical infrastructure.

-

3. What are the major challenges faced by the UK general surgery devices market?Major challenges include the high cost of advanced surgical technologies, NHS budget constraints, procurement delays, and supply chain disruptions affecting device availability and pricing.

-

4. What opportunities exist in the UK general surgery devices market?Opportunities include the growth of ambulatory surgical centers, increasing shift toward daycare and outpatient procedures, technological innovations such as AI-assisted surgery and robotic systems, and expanding public–private partnerships.

-

5. Who are the key players in the UK general surgery devices market?Key companies include Medtronic plc, Johnson & Johnson (Ethicon), Stryker Corporation, Boston Scientific Corporation, B. Braun Melsungen AG, Smith & Nephew plc, Zimmer Biomet Holdings, Olympus Corporation, Intuitive Surgical, Inc., and ConvaTec Group plc.

Need help to buy this report?