Global Styrene Copolymer Market Size, Share, and COVID-19 Impact Analysis, By Polymer Type (Acrylonitrile-Butadiene-Styrene (ABS), and Styrene-Acrylonitrile (SAN)), By End User (Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Styrene Copolymer Market Insights Forecasts to 2035

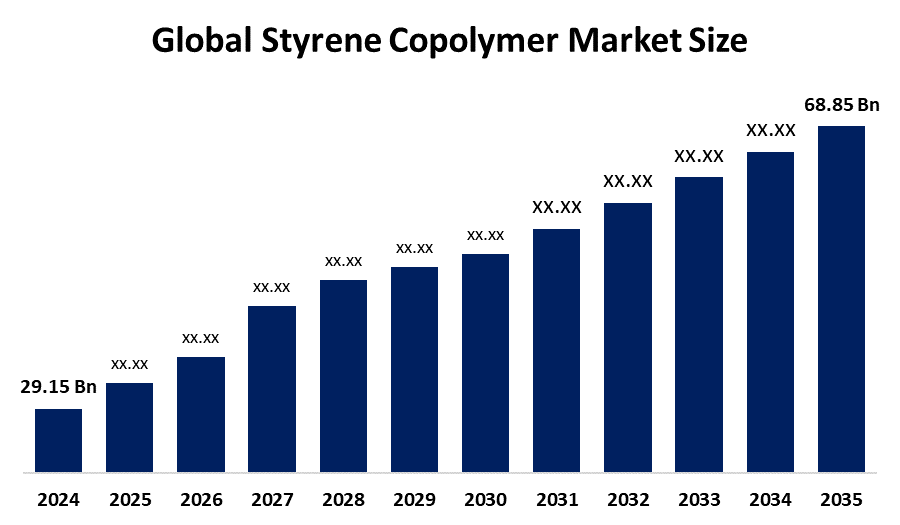

- The Global Styrene Copolymer Market Size Was Estimated at USD 29.15 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 8.13 % from 2025 to 2035

- The Worldwide Styrene Copolymer Market Size is Expected to Reach USD 68.85 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global styrene copolymer market size was worth around USD 29.15 billion in 2024 and is predicted to grow to around USD 68.85 billion by 2035 with a compound annual growth rate (CAGR) of 8.13 % from 2025 to 2035. Opportunities in the automotive, packaging, and construction industries are presented by the styrene copolymer market, which is driven by advancements in high-performance and sustainable polymer solutions as well as the need for lightweight, robust, and reasonably priced materials.

Market Overview

The production, trade, and use of thermoplastic resins made from styrene monomer copolymerized with acrylonitrile, butadiene, or other co-monomers, producing products like acrylonitrile butadiene styrene (ABS) and styrene acrylonitrile (SAN), are all included in the styrene copolymer market. These adaptable polymers play vital roles in automobile parts, electrical housings, rigid packaging, building fittings, and aerospace constructions due to their exceptional hardness, dimensional stability, and processability. In order to decrease food waste and increase food safety, government and regulatory activities are favoring better packaging, both of which encourage material innovation.

Europe launches sustainability initiatives: The PPWR aims for 5% packaging waste reduction by 2030, while EFSA’s June 2025 affirmation of styrene’s non-genotoxicity supports safer, sustainable food-contact applications. The expanding industrial need for adaptable, long-lasting, and reasonably priced polymeric materials across various industries is the main driver of the styrene copolymer market. The market for styrene copolymers, ABS, and SAN is greatly driven by the electronics industry's explosive growth. Due to their exceptional electrical insulating qualities and thermal stability, ABS and SAN materials are preferred in the manufacturing of electronic housings, components, and appliances.

Report Coverage

This research report categorizes the styrene copolymer market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the styrene copolymer market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the styrene copolymer market.

Global Styrene Copolymer Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 29.15 Billion |

| Forecast Period: | 2024 – 2035 |

| Forecast Period CAGR 2024 – 2035 : | CAGR of 8.13% |

| 024 – 2035 Value Projection: | USD 68.85 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 244 |

| Tables, Charts & Figures: | 100 |

| Segments covered: | By Polymer Type, By End User |

| Companies covered:: | CHIMEI, Formosa Plastics Group, INEOS, Kumho Petrochemical, LG Chem, Lotte Chemical, PetroChina Company Limited, SABIC, Techno-UMG Co., Ltd., Tianjin Bohai Chemical Co., Ltd., Toray Industries Inc., Trinseo, Versalis S.p.A., And Others Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The growing automotive sector, which uses styrene copolymers like ABS and SAN extensively to create lightweight, impact-resistant, and aesthetically pleasing components, is one of the main drivers. These materials help reduce vehicle weight, improve fuel economy, and cut emissions, all of which are in line with the growing regulatory focus on environmental sustainability. These materials are in high demand due to their adaptability and use in a variety of industries, such as consumer products, electronics, and automobiles. This rise is being driven by the proliferation of consumer electronics and smart devices, as manufacturers favor lightweight and durable materials. The use of styrene-based copolymers in insulation, piping, fittings, and decorative applications where durability, thermal stability, and resistance to environmental deterioration are crucial is driving demand in the construction sector.

Restraining Factors

The market for styrene copolymer is restricted by a number of factors, including high production costs, strict government regulations, environmental concerns about non-biodegradable polymers, and fluctuating raw material prices. These variables limit widespread adoption and make sustainable growth difficult in some areas and applications.

Market Segmentation

The Styrene Copolymer market share is classified into polymer type and end user.

- The acrylonitrile-butadiene-styrene segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period.

Based on the polymer type, the styrene copolymer market is divided into acrylonitrile-butadiene-styrene (ABS), and styrene-acrylonitrile (SAN). Among these, the acrylonitrile-butadiene-styrene segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The extensive use of acrylonitrile-butadiene-styrene (ABS) in the consumer goods, electronics, and automotive industries supports the segment. The market is also fueled by the growing need for lightweight parts, ongoing industrial growth, and the growing use of advanced engineering plastics in a variety of end-use industries.

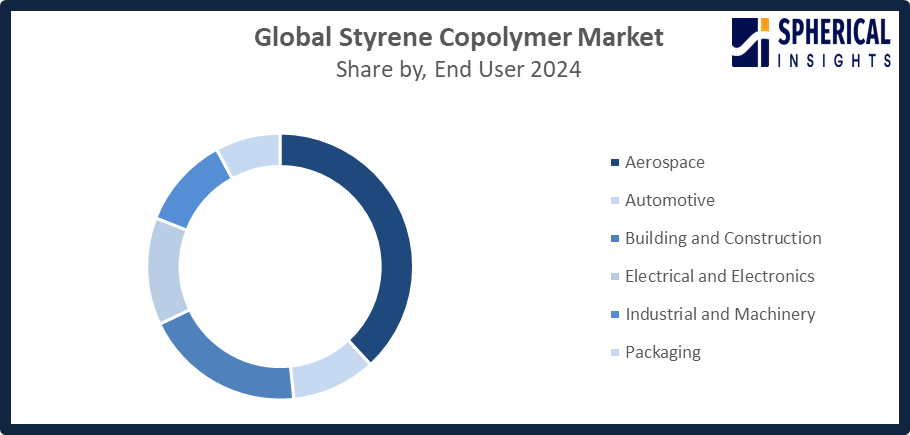

- The aerospace segment accounted for the highest market revenue in 2024, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the styrene copolymer market is divided into aerospace, automotive, building and construction, electrical and electronics, industrial and machinery, packaging, and others. Among these, the aerospace segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The growing need for lightweight, strong, and long-lasting materials in aircraft construction, which improve overall performance and fuel efficiency, is the main factor driving the aerospace industry. The aerospace market is also anticipated to be sustained by continued investments in aerospace technology and the growth of both commercial and defense aviation.

Get more details on this report -

Regional Segment Analysis of the Styrene Copolymer Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the styrene copolymer market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the styrene copolymer market over the predicted timeframe. The Asia-Pacific region's increased production capacity and consumption levels are attributable to a number of structural and economic reasons. The demand for styrene-based materials in industries such as automotive, electronics, construction, and packaging has increased significantly due to rapid industrialization, particularly in China, India, South Korea, and Southeast Asian nations. The demand for ABS grades used in housings and interior components surged due to the recovery of automobile production and the growth of electronics manufacturing in Asia. India's 2025 Union Budget unveiled a PLI scheme for plastics to boost exports and sustainable production, while November reforms scrapped 14 quality norms, reducing input costs and easing chemical imports.

Get more details on this report -

North America is expected to grow at a rapid CAGR in the styrene copolymer market during the forecast period. The region's strong market position is attributed to the existence of well-established manufacturing hubs, an adequate supply of raw materials, and relatively cheaper production costs. The use of consumer products and appliances that significantly rely on styrene copolymers is further stimulated by growing urbanization and increased disposable incomes. Additionally, consistent market growth is supported by ongoing investments in petrochemical infrastructure expansion and technical advancements. Bio-based styrene innovations rise amid ESG mandates as Trinseo’s October 2025 ABS/SAN price adjustments signal supply-chain optimization. U.S. government data values the 2025 styrene sector at $32 billion, supporting 253,000 jobs.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the styrene copolymer market, along with a comparative evaluation primarily based on their Polymer type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes Polymer type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- CHIMEI

- Formosa Plastics Group

- INEOS

- Kumho Petrochemical

- LG Chem

- Lotte Chemical

- PetroChina Company Limited

- SABIC

- Techno-UMG Co., Ltd.

- Tianjin Bohai Chemical Co., Ltd.

- Toray Industries Inc.

- Trinseo

- Versalis S.p.A.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In October 2025, Trinseo launched a EUR 10 per ton price reduction for ABS and SAN grades, expected to intensify competition and trigger potential price adjustments across the global styrene copolymer supply chain.

- In December 2024, INEOS Styrolution signed a definitive agreement to sell its Map Ta Phut ABS and SAN production facility in Thailand to Styrenix Performance Materials. The deal is expected to close by early 2025.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the styrene copolymer market based on the below-mentioned segments:

Global Styrene Copolymer Market, By Polymer Type

- Acrylonitrile-Butadiene-Styrene (ABS)

- Styrene-Acrylonitrile (SAN)

Global Styrene Copolymer Market, By End User

- Aerospace

- Automotive

- Building and Construction

- Electrical and Electronics

- Industrial and Machinery

- Packaging

- Others

Global Styrene Copolymer Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the CAGR of the styrene copolymer market over the forecast period?The global styrene copolymer market is projected to expand at a CAGR of 8.13% during the forecast period.

-

2. What is the market size of the styrene copolymer market?The global styrene copolymer market size is expected to grow from USD 29.15 billion in 2024 to USD 68.85 billion by 2035, at a CAGR of 8.13 % during the forecast period 2025-2035.

-

3. Which region holds the largest share of the styrene copolymer market?Asia Pacific is anticipated to hold the largest share of the styrene copolymer market over the predicted timeframe.

-

4. Who are the top 10 companies operating in the global styrene copolymer market?CHIMEI, Formosa Plastics Group, INEOS, Kumho Petrochemical, LG Chem, Lotte Chemical, PetroChina Company Limited, SABIC, Techno-UMG Co., Ltd., Tianjin Bohai Chemical Co., Ltd., Toray Industries Inc., Trinseo, Versalis S.p.A., and Others.

-

5. What factors are driving the growth of the styrene copolymer market?The styrene copolymer market is driven by rising demand from automotive, electronics, and packaging sectors, supported by industrial expansion, technological advancements, lightweight material adoption, and increasing consumer product applications.

-

6. What are the market trends in the styrene copolymer market?The styrene copolymer market trends include rising use of bio-based styrene variants, increasing emphasis on sustainability, technological innovations, expanding applications in automotive and electronics, and greater investment in high-performance, durable, and recyclable polymer solutions.

-

7. What are the main challenges restricting wider adoption of the styrene copolymer market?Major challenges include fluctuating raw material prices, stringent environmental regulations, competition from alternative polymers, supply chain disruptions, and rising sustainability pressures that complicate large-scale production and limit broader market.

Need help to buy this report?