Global Space Semiconductor Market Size By Application (Satellite, Launch Vehicles, Deep Space Probe, Rovers and Landers, and Others), By Type (Radiation Hardened Grade, Radiation Tolerant Grade, and Others), By Component (Integrated Circuits, Discrete Semiconductors Devices, Optical Devices, Microprocessor, Memory, Sensors, and Others), By Region, And Segment Forecasts, By Geographic Scope And Forecast to 2033

Industry: Aerospace & DefenseGlobal Space Semiconductor Market Insights Forecasts to 2033

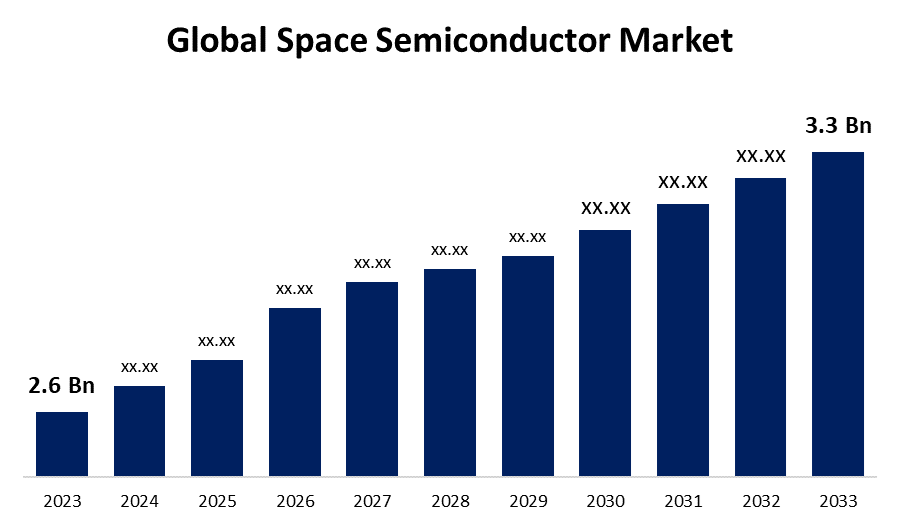

- The Space Semiconductor Market Size was valued at USD 2.6 Billion in 2023.

- The Market Size is Growing at a CAGR of 2.41% from 2023 to 2033

- The Worldwide Space Semiconductor Market Size is expected to reach USD 3.3 Billion by 2033

- Asia Pacific is expected to Grow the fastest during the forecast period

Get more details on this report -

The Global Space Semiconductor Market Size is expected to reach USD 3.3 Billion by 2033, at a CAGR of 2.41% during the forecast period 2023 to 2033.

Smaller, lighter, and more power-efficient semiconductor components are in greater demand as the emphasis on lowering the dimensions and weight of satellites and space exploration equipment grows. There are special obstacles in space habitats because of things like radiation, severe temperatures, and vacuum conditions. Ruggedization is necessary for semiconductors used in space applications so they can survive these extreme circumstances. There has been an increase in the use of small satellites for a variety of purposes, such as communication, Earth observation, and science. The need for semiconductor parts appropriate for tiny satellite platforms is being driven by this trend. Ambitious space exploration missions are being carried out by both commercial enterprises and space government. These missions include crewed trips to the Moon, Mars, and beyond. Advanced semiconductor technology is needed for these missions' scientific instruments, communication, navigation, and onboard systems.

Global Space Semiconductor Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 2.6 Billion |

| Forecast Period: | 2023 - 2033 |

| Forecast Period CAGR 2023 - 2033 : | 2.41% |

| 2033 Value Projection: | USD 3.3 Billion |

| Historical Data for: | 2019 - 2022 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Application, By Type, By Component, By Region |

| Companies covered:: | Teledyne Technologies Incorporated, Infineon Technologies AG, Texas Instruments Incorporated, Microchip Technology Inc., Cobham Advanced Electronic Solutions Inc., STMicroelectronics International N.V., Solid State Devices Inc., Honeywell International Inc., Xilinx Inc., BAE System Plc, and TE Connectivity |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Space Semiconductor Market Value Chain Analysis

Integrated circuits (ICs) and customised chips for space applications are created by semiconductor companies. To survive the severe conditions of space habitats, these systems frequently call for radiation-hardened components and specialised functionality. Upon completion, semiconductor designs are produced in specialised fabrication facilities, or fabs. Strict quality criteria must be followed by these fabs to guarantee the dependability and functionality of semiconductors suitable for space travel. To make sure they fulfil the specifications needed for space applications, space-grade semiconductors go through extensive testing and qualifying procedures. Larger electronic systems, such as satellite payloads, onboard computers, communication systems, navigation systems, and scientific instruments, are combined with semiconductors that meet space qualification requirements. The entire satellite platform or spacecraft is further integrated with integrated semiconductor components. Rockets or other launch vehicles are used to send space systems using semiconductor components into orbit after they have been integrated and tested. Semiconductor parts continue to function as part of the satellite or space exploration mission after they are in orbit. When space systems and satellites reach the end of their useful lives, it may be necessary to decommission them and dispose of them carefully to avoid creating space debris.

Space Semiconductor Market Opportunity Analysis

The need for space-grade semiconductor components is driven by the growing number of satellites being deployed for communication, Earth observation, navigation, scientific research, and other purposes. The formation of additional satellite constellations—including mega-constellations for worldwide internet coverage—further fuels this need. Dedicated space agencies' and private firms' space exploration programmes present semiconductor manufacturers with chances to offer parts for spacecraft, rovers, landers, and other exploration vehicles. High-performance, radiation-hardened semiconductor technology that can resist the harsh conditions of space settings is needed for these missions. New markets and applications for semiconductor manufacturers to supply parts for creative space-based solutions are being created by emerging markets and applications in space, like space-based internet services, space-based manufacturing, in-orbit servicing, and space debris abatement.

Regional Forecasts

North America Market Statistics

Get more details on this report -

North America is anticipated to dominate the Space Semiconductor Market from 2023 to 2033. NASA (National Aeronautics and Space Administration) is based in North America and is responsible for leading a number of space exploration missions, satellite launches, and scientific research projects. The need for cutting-edge semiconductor technology for space missions is driven by NASA's partnerships with international partners and commercial space firms. Spending on space-related projects is mostly borne by the aerospace and defence industries in North America, especially in the US. The need for space-grade semiconductor components is fueled by investments made by defence contractors and agencies in missile defence, satellite technology, and reconnaissance systems. For satellite communications services such as military communications, broadband internet, and television transmission, North America is a significant market. The space semiconductor market is expanding due to the need for high-performance semiconductor parts for ground stations and satellite payloads.

Asia Pacific Market Statistics

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China, India, Japan, and South Korea are among the nations in the Asia-Pacific area that are aggressively growing their satellite fleets for use in scientific research, communication, Earth observation, and navigation. The increased use of satellites is driving up demand for space-grade semiconductors. Asia-Pacific nations, especially South Korea, China, and Taiwan, are important centres for the production of semiconductor components. Integrated circuits (ICs), microprocessors, memory chips, sensors, and other space-grade components are supplied by semiconductor companies in the area. The Asia-Pacific region's need for space semiconductor components is being driven by emerging markets like precision agriculture, satellite-based remote sensing, and disaster management. To solve a range of societal and environmental concerns, governments and corporations are investing in satellite-based solutions.

Segmentation Analysis

Insights by Application

The satellite segment accounted for the largest market share over the forecast period 2023 to 2033. Satellite deployments for a range of purposes, such as communication, navigation, Earth observation, scientific research, and national security, have increased significantly. The demand for semiconductor components used in satellite systems has increased in tandem with the boom in satellite deployments from both commercial and government space agencies. Smaller, lighter, and more power-efficient semiconductor components are becoming more and more necessary as a result of the trend towards satellite miniaturisation, which has been fueled in part by the rise of CubeSats and small satellites. Commercial off-the-shelf (COTS) semiconductor technology that has been modified for space use is frequently used in these smaller spacecraft.

Insights by Type Size

The radiation hardened segment accounted for the largest market share over the forecast period 2023 to 2033. Radiation-resistant semiconductor components are becoming more and more necessary as space missions get more complicated and explore harsher environments. Critical systems including scientific instruments, onboard computers, communication systems, and navigation systems depend on these parts. The need for radiation-hardened semiconductor components has increased due to the growing number of satellites being deployed for both government and commercial uses. The dependability and durability of satellite systems functioning in the radiation-heavy space environment depend on these components. Commercial satellite operators, space tourism businesses, and other private organisations engaged in space exploration and satellite deployment have raised their need for radiation-hardened semiconductor components as a result of the commercialization of space activities.

Insights by Component

The integrated circuits segment accounted for the largest market share over the forecast period 2023 to 2033. A broad variety of integrated circuits (ICs) designed for space applications are required due to the increasing demand for satellites for communication, Earth observation, navigation, scientific research, and national security. Microprocessors, memory chips, digital signal processors (DSPs), and specialised interface and control circuits are examples of these ICs. High-performance integrated circuits (ICs) that can handle intricate modulation schemes, error correcting coding, and signal processing algorithms are necessary for the development of modern communication systems for satellite payloads and ground stations. The communication linkages between satellites and terrestrial networks are made dependable and effective by these ICs. To withstand the effects of ionising radiation in the space environment, integrated circuits (ICs) utilised in space applications need to be radiation-hardened. In order to reduce the impacts of radiation, such as single-event effects (SEEs) and total ionising dose (TID) effects, radiation-hardened integrated circuits (ICs) use materials and design elements.

Recent Market Developments

- In September 2023, a strategic agreement was inked between UK firm Space Forge and Northrop Grumman. The agreement backs the company's intention to use compound semiconductor substrates in low-Earth orbit.

Competitive Landscape

Major players in the market

- Teledyne Technologies Incorporated

- Infineon Technologies AG

- Texas Instruments Incorporated

- Microchip Technology Inc.

- Cobham Advanced Electronic Solutions Inc.

- STMicroelectronics International N.V.

- Solid State Devices Inc.

- Honeywell International Inc.

- Xilinx Inc.

- BAE System Plc

- TE Connectivity

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Space Semiconductor Market, Application Analysis

- Satellite

- Launch Vehicles

- Deep Space Probe

- Rovers and Landers

- Others

Space Semiconductor Market, Type Analysis

- Radiation Hardened Grade

- Radiation Tolerant Grade

- Others

Space Semiconductor Market, Component Analysis

- Integrated Circuits

- Discrete Semiconductors Devices

- Optical Devices

- Microprocessor

- Memory, Sensors

- Others

Space Semiconductor Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the Space Semiconductor Market?The global Space Semiconductor Market is expected to grow from USD 2.6 billion in 2023 to USD 3.3 billion by 2033, at a CAGR of 2.41% during the forecast period 2023-2033.

-

2. Who are the key market players of the Space Semiconductor Market?Some of the key market players of the market are Teledyne Technologies Incorporated, Infineon Technologies AG, Texas Instruments Incorporated, Microchip Technology Inc., Cobham Advanced Electronic Solutions Inc., STMicroelectronics International N.V., Solid State Devices Inc., Honeywell International Inc., Xilinx Inc., BAE System Plc, TE Connectivity.

-

3. Which segment holds the largest market share?The satellite segment holds the largest market share and is going to continue its dominance.

-

4. Which region is dominating the Space Semiconductor Market?North America is dominating the Space Semiconductor Market with the highest market share.

Need help to buy this report?