South America Methanol Market Size, Share, and COVID-19 Impact Analysis, By Feedstock (Natural Gas and Coal), By Derivatives (Formaldehyde, MTO/MTP, Gasoline, MTBE, MMA, Acetic Acid and Biodiesel), and South America Methanol Market Insights, Industry Trends, Forecast to 2035.

Industry: Chemicals & MaterialsSouth America Methanol Market Insights Forecasts to 2035

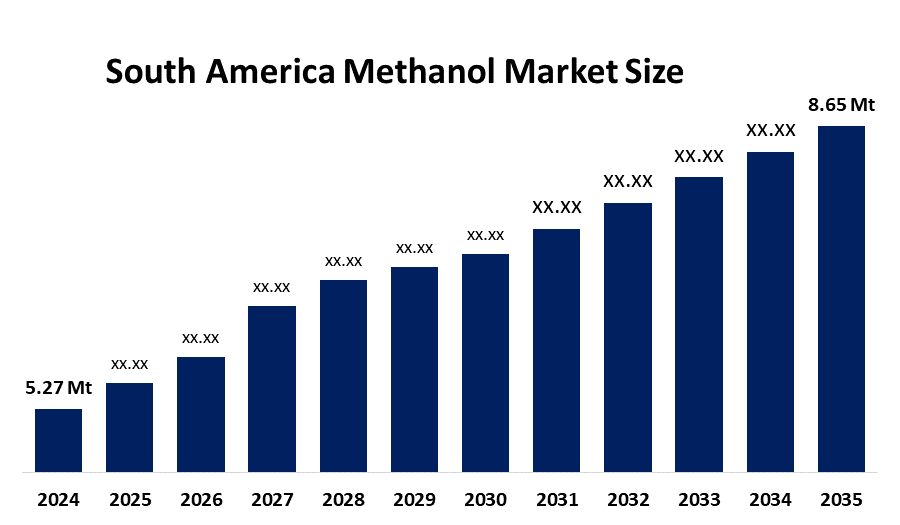

- The South America Methanol Market Size Was Estimated at 5.27 Million Tonnes in 2024

- The Market Size is Expected to Grow at a CAGR of Around 4.61% from 2025 to 2035

- The South America Methanol Market Size is Expected to Reach 8.65 Million Tonnes by 2035

Get more details on this report -

According to a research report published by Spherical Insights & Consulting, The South America Methanol Market Size is anticipated to reach 8.65 Million tonnes by 2035, Growing at a CAGR of 4.61% from 2025 to 2035. The market is driven by the rising demand for bio-based chemical commodities across various end-user industries, like automotive, construction, paints and coatings, etc., are set to drive South America Methanol during the forecast period.

Market Overview

The market includes the manufacturing, distribution, and usage of methanol, which exists as a colorless liquid. The Brazilian market experiences fast growth in the usage of bio-methanol and green methanol because companies must comply with sustainability regulations and invest in renewable energy sources. The substance has gained popularity as a cleaner-burning replacement for heavy fuel oil, which enables compliance with International Maritime Organization (IMO) standards.

Brazil emerged as the leading contributor, supported by extensive fuel-blending initiatives and the growing needs of its chemical manufacturing industry. The regional market strength receives additional support through government policies, which create a stable environment for downstream operations.

Brazil's biodiesel blend mandate which requires a 1% annual increase from its current 15% level until late 2025, will lead to higher methanol consumption which local users will require between 80,000 and 100,000 metric tons each year. Austrian investors are planning a USD 75 million green methanol plant aimed at the European export market. The Paysandú eFuels facility will become South America most extensive e-methanol production plant which will produce 700000 tonnes of e-methanol annually.

Report Coverage

This research report categorises the South America methanol market based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the South America methanol market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the South America methanol market.

South America Methanol Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | 5.27 Million tonnes |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 4.61% |

| 2035 Value Projection: | 8.65 Million tonnes |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 95 |

| Segments covered: | By Feedstock, By Derivatives |

| Companies covered:: | Petrobras, Methanol Holdings Ltd, GPC Quimica, OCI N.V., Methanex Corporation, Proman, SABIC, BASF SE, Braskem, Bolivia, Others, and Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The methanol market in South America is driven by the rising need for methanol as a cleaner substitute for fossil fuels drives demand for methanol in gasoline blending operations including M3 to M15 blends, and in marine applications that need to fulfill new emission regulations. The market expansion occurs due to advancements in low-emission fuel technologies and the adoption of methanol-based components in lightweight vehicle design.

Restraining Factors

The methanol market in South America is restrained by the industry controls the market, so methanol cannot establish itself as a competing fuel option. The insufficient storage and handling facilities, with the absence of dedicated transportation infrastructure, result in higher distribution expenses while preventing widespread product distribution.

Market Segmentation

The South America methanol market share is categorised into feedstock and derivatives.

- The natural gas segment accounted for the largest share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The South America methanol market is segmented by feedstock into natural gas and coal. Among these, the natural gas segment accounted for the largest share in 2024 and is expected to grow at a significant CAGR during the forecast period. The growth of the segment is driven by Natural gas serves as the primary feedstock worldwide because it constitutes more than 60 to 90 percent of production in South American regions that possess large natural gas reserves. The established Steam Methane Reforming (SMR) infrastructure together with reduced extraction expenses. Gas-based production maintains higher environmental cleanliness than coal because it meets regional emission standards and corporate sustainability objectives.

- The gasoline segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on derivatives, the South America methanol market is segmented into formaldehyde, MTO/MTP, gasoline, MTBE, MMA, acetic acid and biodiesel. Among these, the gasoline segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segmental growth is driven by Brazil stands as the world's largest methanol consumer which provides the country with its unique competitive advantage. the government has implemented regulations that establish mandatory biodiesel blending requirements for diesel fuel.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the South America methanol market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Petrobras

- Methanol Holdings Ltd

- GPC Quimica

- OCI N.V.

- Methanex Corporation

- Proman

- SABIC

- BASF SE

- Braskem

- Bolivia

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the South America, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the South America methanol market based on the below-mentioned segments:

South America Methanol Market, By Feedstock

- Natural Gas

- Coal

South America Methanol Market, By Derivatives

- Formaldehyde

- MTO/MTP

- Gasoline

- MTBE

- MMA

- Acetic Acid

- Biodiesel

Frequently Asked Questions (FAQ)

-

1. What is the market size of the South America methanol market in 2024 and its future projection?A: The South America methanol market size is expected to grow from 5.27 million tonnes in 2024 to 8.65 million tonnes by 2035, growing at a CAGR of 4.61% during the forecast period 2025-2035

-

2. What are the major restraints in the market?A: Growth is driven by increasing demand for cleaner fuel alternatives, especially in gasoline blending and marine fuel applications. Adoption of low-emission technologies and regulatory compliance further support market expansion.

-

3. Which country is the leading contributor in the region?Brazil leads the market due to strong fuel-blending initiatives and growing chemical industry demand. Government policies and sustainability efforts further strengthen its dominance.

-

4. What role does biodiesel policy play in methanol demand?A: Brazil’s biodiesel mandate, increasing annually from 15%, is expected to drive additional methanol demand of 80,000–100,000 metric tons per year. This significantly boosts consumption in fuel applications.

-

5. Why is natural gas preferred over coal for methanol production?A: Natural gas is more environmentally friendly and aligns with emission standards. It also benefits from established infrastructure and cost-efficient extraction compared to coal.

-

6. Why does the gasoline segment dominate the derivatives category?A: High transportation fuel demand and regulatory support for cleaner fuels drive gasoline blending. Brazil’s large consumption and fuel policies further strengthen this segment.

-

7. What are the major restraints in the market?A: The market faces challenges such as limited infrastructure for storage and transportation. High distribution costs and a lack of dedicated logistics hinder widespread adoption.

-

8. Who are the key players in the South America methanol market?A: Major companies include Petrobras, Methanex Corporation, OCI N.V., BASF SE, and Braskem. These players focus on expansion, partnerships, and innovation.

-

9. What investment developments are occurring in the market?A: A USD 75 million green methanol plant is being planned by Austrian investors. Additionally, the Paysandú eFuels facility will produce 700,000 tonnes of e-methanol annually.

Need help to buy this report?