Global Refractory Material Market Size, Share, and COVID-19 Impact Analysis, Russia-Ukraine War Impact, Tariff Analysis, By Chemistry (Acidic, Basic, and Neutral), By Chemical Composition (Alumina, Silica, Magnesia, Fireclay, and Others), By Form (Shaped, and Unshaped), By End Use (Metals & Metallurgy, Cement, Glass & Ceramics, Power Generation, and Others), By Sales Channels (Direct, and Indirect), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Advanced MaterialsRefractory Material Market Summary, Size & Emerging Trends

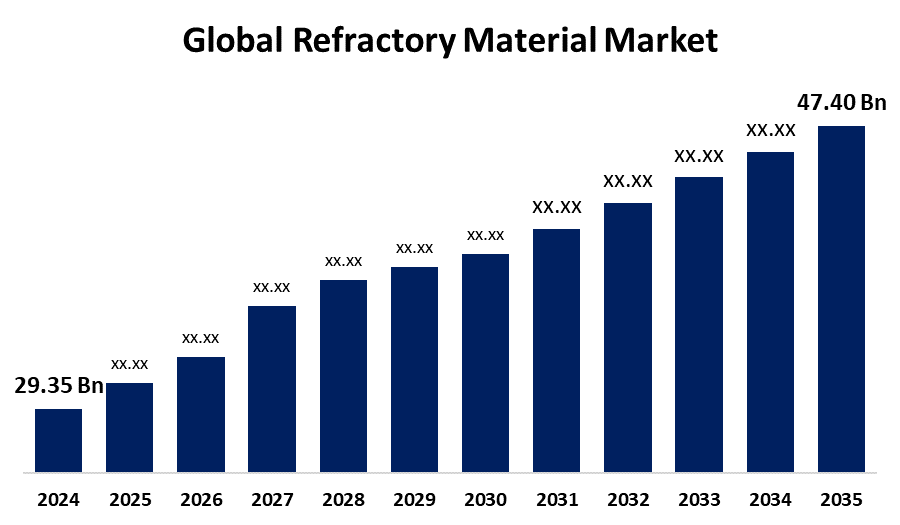

According to Spherical Insights, The Global Refractory Material Market Size is Expected to Grow from USD 29.35 Billion in 2024 to USD 47.40 Billion by 2035, at a CAGR of 4.45% during the forecast period 2025-2035. Technology breakthroughs, expanding infrastructure development in emerging nations across the globe, and rising demand in the steel, cement, and glass industries all present substantial opportunities for the refractory material market.

Key Market Insights

Get more details on this report -

- Asia Pacific is expected to account for the largest share in the refractory material market during the forecast period.

- In terms of chemistry, the basic segment is projected to lead the refractory material market in terms of equipment throughout the forecast period

- In terms of chemical composition, the alumina segment captured the largest portion of the market

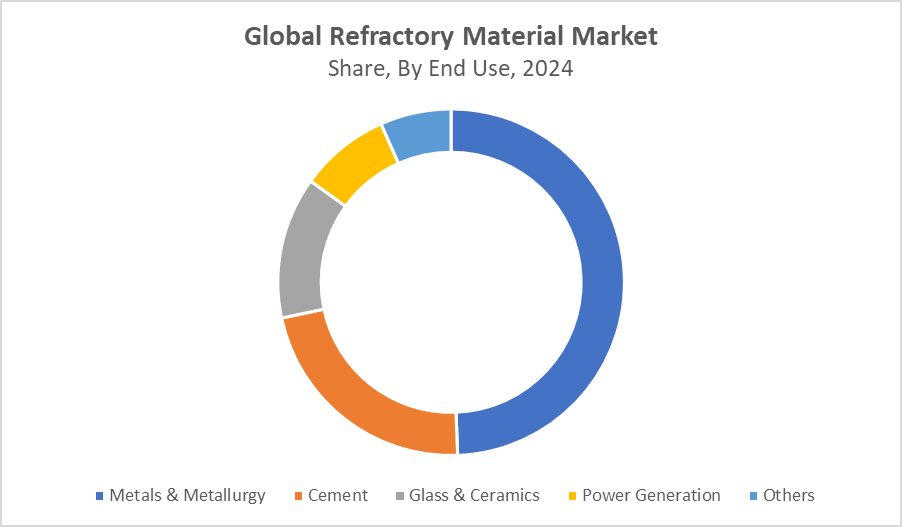

- In terms of end use, the metals & metallurgy segment captured the largest portion of the market

Global Market Forecast and Revenue Outlook

- 2024 Market Size: USD 29.35 Billion

- 2035 Projected Market Size: USD 47.40 Billion

- CAGR (2025-2035): 4.45%

- Asia Pacific: Largest market in 2024

- North America: Fastest growing market

Refractory Material Market

The global industry that produces, distributes, and sells refractory materials, specialized materials that are extremely resistant to heat, corrosion, and mechanical wear, is known as the refractory material market. These materials are crucial for protecting equipment and ensuring operational efficiency in sectors including steel, cement, glass, and petrochemicals that need high-temperature operations. The refractory material market includes a range of refractory products, each with a unique industrial purpose, such as silica, magnesite, fireclay, and high alumina refractories. The growing need for refractory materials is a result of rising industrialization, increased infrastructure development, and improvements in manufacturing technology.

The global market for refractory materials is expanding due to rising investments in the iron and steel sectors. Strong railroads and building infrastructure might give the iron and steel sector another boost, which would fuel the expansion of the refractory material market. In order to guarantee thermal stability, refractory materials are used extensively in the glassmaking process. This is anticipated to support the growth of the refractory materials market.

Refractory Material Market Trends

- Global market expansion is driven by the steel, cement, and glass industries' growing demand.

- Performance and energy efficiency are improved by the growing use of cutting-edge and environmentally friendly refractory materials.

- Market expansion is driven by growing infrastructural and industrial modernization investments in emerging economies.

- Future market developments are influenced by technological advancements and an emphasis on ecologically friendly production methods.

Global Refractory Material Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 29.35 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 4.45% |

| 2035 Value Projection: | USD 47.40 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 230 |

| Tables, Charts & Figures: | 121 |

| Segments covered: | By Chemistry, By Chemical Composition, By Form, By End Use, By Sales Channels and By Region |

| Companies covered:: | AGC Inc., Lanexis Enterprises (P) Ltd., RHI Magnesita GmbH, IFGL Refractories Limited., Calderys, Saint-Gobain, SHINAGAWA REFRACTORIES CO., LTD., Morgan Advanced Materials plc, Krosaki Harima Corporation, Vitcas, Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis. |

Get more details on this report -

Refractory Material Market Dynamics

Driving Factors: Demand from key industries drives refractory market.

Growing demand from important end-use sectors like steel, cement, glass, and petrochemicals, where high-temperature processes require robust and heat-resistant materials, is the main factor propelling the refractory material market. Rapid infrastructural development and industrialization, especially in emerging nations, increase production capacity and technical breakthroughs, which further fuel market expansion. Tight environmental laws also promote the use of sustainable and energy-efficient refractory materials, which leads to advancements in manufacturing techniques and material composition. Another factor driving the usage of high-performance refractory materials in heavy industries is the growing emphasis on improving operational efficiency and decreasing downtime.

Restrain Factors: High costs limit refractory market adoption widely.

The market for refractory materials is constrained by a number of reasons that hinder its expansion. Widespread adoption is restricted by high production and raw material costs, particularly for small and medium-sized businesses. Manufacturers must pay more to comply with environmental rules about the recycling and disposal of refractory waste. Traditional refractory products are also challenged by the existence of substitute materials and technologies that provide better performance or lower pricing.

Opportunity: Rising demand from industries creates growth opportunities.

The market for refractory materials offers substantial opportunities due to rising demand from developing sectors such as petrochemicals, steel, cement, and glass. A significant investment opportunity is presented by emerging economies' increasing industrialization and infrastructure development. Furthermore, technological developments make it possible to create novel, eco-friendly, and energy-efficient refractory materials, which helps to address sustainability issues. The market's opportunities are further fueled by heavy industries' growing emphasis on improving operational efficiency and lowering maintenance costs. Additionally, the move toward specialized refractory solutions made for certain industrial uses opens up new market opportunities.

Challenges: Multiple challenges hinder refractory market’s steady growth.

The refractory material market is confronted with a number of challenges that hinder its expansion and advancement. Manufacturers face uncertainty due to supply chain disruptions and fluctuating raw material prices. Operational costs and compliance challenges are increased by high production prices and strict environmental requirements. The market also faces competition from cutting-edge technologies and substitute materials that can provide better performance or financial benefits. Demand is also impacted by economic downturns and shifts in important end-use sectors like steel and cement.

Global Refractory Material Market Ecosystem Analysis

The ecosystem of the worldwide refractory material market includes manufacturers, distributors, end-use industries, research institutes, regulatory agencies, and suppliers of raw materials. Demand is driven by important industries that mostly depend on high-performance refractory products for high-temperature operations, including steel, cement, glass, and petrochemicals. To satisfy changing industrial demands, manufacturers prioritize cost-effectiveness, sustainability, and innovation. The availability of raw materials, environmental laws, and energy prices all have a big impact on market dynamics. The ecosystem is further shaped by industry stakeholder collaboration, technology developments, and strategic alliances, which guarantee competitiveness, supply chain stability, and long-term growth in international markets.

Global Refractory Material Market, By Chemistry

The basic segment led the refractory material market, generating the largest revenue share. Magnesia, dolomite, and chromite make up the majority of basic refractories, which are growing at the fastest rate due to their high refractoriness under load and robust resistance to basic slags. Their fundamental nature, which prevents corrosion from basic slags and atmospheres, makes them essential in the production of steel and non-ferrous metal processing.

The acidic segment in the refractory material market is expected to grow at the fastest CAGR over the forecast period. The acidic chemistry segment growth is attributed to the increasing demand for acidic refractories, which are characterized by their high silica content and excellent resistance to acidic slags and environments.

Global Refractory Material Market, By Chemical Composition

The alumina segment held the largest market share in the refractory material market. Alumina's remarkable mechanical strength, high melting point, and thermal stability are what propel the market. The alumina segment's dominance has been strengthened by the development of manufacturing technologies and the growing need for high-performance materials across industrial sectors, making it a major market growth driver.

The magnesia segment in the refractory material market is projected to register the fastest CAGR. The basic nature of magnesium-based refractories, which prevent corrosion from basic slags and atmospheres, makes them popular in the production of steel, cement, and nonferrous metals.

Global Refractory Material Market, By End Use

The metals & metallurgy segment held the largest market share in the refractory material market. The extensive usage of refractory materials in high-temperature operations such metal smelting, refining, and casting is the main reason for the metals and metallurgy segment. Refractories are necessary to line kilns, ladles, and furnaces, guaranteeing both operational safety and efficiency.

Get more details on this report -

The cement segment in the refractory material market is projected to register the fastest CAGR. Equipment used in cement manufacturing is constantly subjected to high temperatures, chemical abrasion, and mechanical stress, particularly in rotary kilns, preheaters, and clinker coolers.

Asia Pacific is expected to account for the largest share of the refractory material market during the forecast period. The growing demand for iron and steel from a variety of end industries, including all of the industrial, construction and infrastructure, automotive, and others, has led to an increase in production capacity among iron and steel producers in the Asia-Pacific region, where refractory materials are commonly used for temperature stability reasons.

Get more details on this report -

China is experiencing steady growth in the refractory material market. Refractory material manufacturers are being forced to provide high-quality refractory materials for use in furnaces, kilns, incinerators, and other high-temperature applications due to the rapidly growing china refractory material market.

North America is expected to grow at the fastest CAGR in the refractory material market during the forecast period. The steel, cement, glass, and petrochemical industries, all of which are significant users of refractory materials, benefit greatly from the region's strong industrial infrastructure. Demand is anticipated to be greatly increased by ongoing expenditures in energy projects, manufacturing facilities, and infrastructural expansion.

United States is the largest market for refractory material is primarily due to its robust industrial sector, including steel, cement, glass, and petrochemical industries, which heavily depend on refractory products. Additionally, the country’s strong focus on technological advancement, infrastructure development, and the presence of major manufacturers further support market growth and dominance.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the refractory material market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

WORLDWIDE TOP KEY PLAYERS IN THE REFRACTORY MATERIAL MARKET INCLUDE

- AGC Inc.

- Lanexis Enterprises (P) Ltd.

- RHI Magnesita GmbH

- IFGL Refractories Limited.

- Calderys

- Saint-Gobain

- SHINAGAWA REFRACTORIES CO., LTD.

- Morgan Advanced Materials plc

- Krosaki Harima Corporation

- Vitcas

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Product Launches in Refractory Material

- In November 2024, RHI Magnesita launched a new contract model for refractory materials called "4PRO." Through a more comprehensive and modern approach, the model is intended to guide high-temperature industries such as steel, cement, glass, non-ferrous metals, etc., toward a sustainable and technologically advanced future.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the refractory material market based on the below-mentioned segments:

Global Refractory Material Market, By Chemistry

- Acidic

- Basic

- Neutral

Global Refractory Material Market, By Chemical Composition

- Alumina

- Silica

- Magnesia

- Fireclay

- Others

Global Refractory Material Market, By Form

- Shaped

- Unshaped

Global Refractory Material Market, By End Use

- Metals & Metallurgy

- Cement

- Glass & Ceramics

- Power Generation

- Others

Global Refractory Material Market, By Sales Channel

- Direct

- Indirect

Global Refractory Material Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the CAGR of the refractory material market over the forecast period?The global Refractory Material market is projected to expand at a CAGR of 4.45% during the forecast period.

-

2. What is the market size of the refractory material market?The global refractory material market size is expected to grow from USD 29.35 billion in 2024 to USD 47.40 billion by 2035, at a CAGR of 4.45% during the forecast period 2025-2035.

-

3. Which region holds the largest share of the refractory material market?Asia Pacific is anticipated to hold the largest share of the refractory material market over the predicted timeframe.

-

4. Who are the top 10 companies operating in the global refractory material market?Key players include AGC Inc., Lanexis Enterprises (P) Ltd., RHI Magnesita GmbH, IFGL Refractories Limited., Calderys, Saint-Gobain, SHINAGAWA REFRACTORIES CO., LTD., Morgan Advanced Materials plc, Krosaki Harima Corporation, Vitcas, and Others.

-

5. What factors are driving the growth of the refractory material market?The growth of the refractory material market is driven by rising demand in steel and cement industries, advancements in manufacturing technologies, infrastructure development, and increasing usage in non-metallic materials processing.

-

6. What are the main challenges restricting wider adoption of the refractory material market?The refractory material market faces challenges such as high production costs, environmental regulations, limited raw material availability, complex manufacturing processes, and the need for frequent maintenance and replacement in high-temperature industrial applications.

Need help to buy this report?