Global Precision Diagnostics Market Size, Share, and COVID-19 Impact Analysis, By Type (Genetic Tests, Esoteric Tests, and Others), By Application (Oncology, Cardiovascular, Immunology, Neurology, and Others), By End User (Hospitals, Clinical Laboratories, and Homecare), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033.

Industry: HealthcareGlobal Precision Diagnostics Market Insights Forecasts to 2033

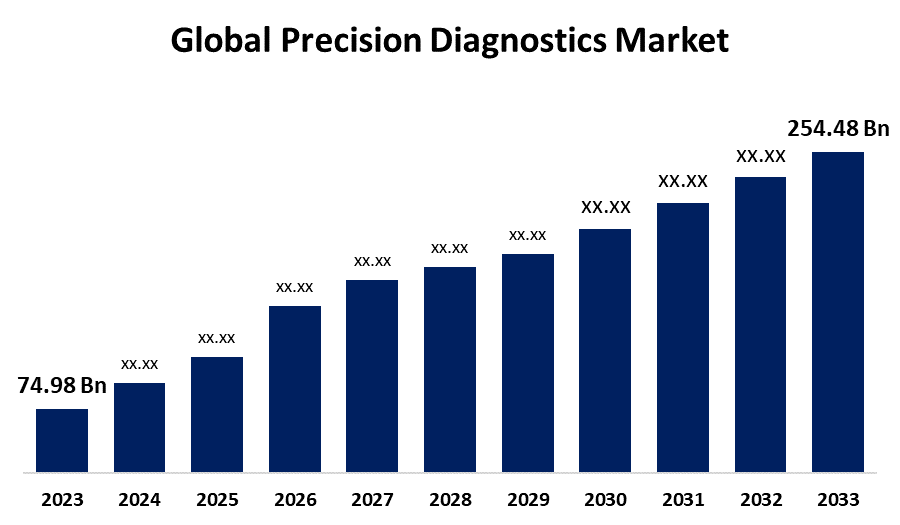

- The Global Precision Diagnostics Market Size was Valued at USD 74.98 Billion in 2023

- The Market Size is Growing at a CAGR of 13% from 2023 to 2033

- The Worldwide Precision Diagnostics Market Size is Expected to Reach USD 254.48 Billion by 2033

- Asia Pacific is Expected to Grow the fastest during the forecast period.

Get more details on this report -

The Global Precision Diagnostics Market Size is Anticipated to Exceed USD 254.48 Billion by 2033, Growing at a CAGR of 13% from 2023 to 2033.

Market Overview

Precision diagnostics, which is also referred to as personalized diagnostics or precision medicine diagnostics, is a field of medicine that combines cutting-edge diagnostic tools and techniques to customize medical interventions, therapies, and decisions for specific patients. It uses a variety of tests, including esoteric and genetic testing, and is mostly used to treat diabetes and cancer. Since it is important to obtain complete information on each patient's genetic composition, molecular traits, and state of health, a range of diagnostic techniques, including genetic testing, molecular profiling, imaging, and other modern diagnostic modalities, are used. It offers precise and focused information that improves the understanding of a patient's illness or condition, the prediction of their reaction to particular medicines, and the creation of individualized treatment regimens for them. The market for precision diagnostics is expanding as a result of the increased need for precision medicine introduced by the rising incidence of rare neurological illnesses and the rising prevalence of cancer. The accuracy and efficiency of these tests have increased due to technological advancements in diagnostic platforms and tools, such as artificial intelligence and machine learning algorithms. Additionally, the market is continuing to rise because of patients' and healthcare professionals' increasing awareness of and use of precision diagnostic techniques.

Report Coverage

This research report categorizes the market for the global precision diagnostics market based on various segments and regions forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the global precision diagnostics market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the global precision diagnostics market.

Global Precision Diagnostics Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 74.98 Billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 13% |

| 2033 Value Projection: | USD 254.48 Billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 265 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Type, By Application, By End User, By Region |

| Companies covered:: | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Thermo Fisher Scientific Inc., bioMérieux SA, Becton, Dickinson, and Company, Danaher Corporation, Quest Diagnostics, Diatech Pharmacogenetics, Swiss Precision Diagnostics, Koninklijke Philips N.V, Lantheus Medical Imaging, Inc., HALO Precision Diagnostics, Inc, Agilent Technologies Inc., and Others |

| Pitfalls & Challenges: | Covid-19 Empact, Challenges, Growth, Analysis. |

Get more details on this report -

Driving Factors

Diagnostic tests that are precise and timely are becoming increasingly necessary as chronic diseases like cancer, heart problems, and infectious infections become more common. Better early detection and disease management are made possible by precision diagnostics' increased sensitivity and specificity. Through early disease detection, precision diagnostics can lower healthcare expenditures by preventing late-stage interventions and increasing the likelihood of a successful course of treatment. An important factor driving the market is the focus on early disease identification that some nations are providing with financial assistance from the government and private investments.

Restraining Factors

High research and development (R&D) expenses have the potential to prevent the progress of precision diagnostics despite their enormous opportunity in many areas of modern medicine and so restrict market growth. The market's growth is being impacted by the tests' natural ineffectiveness the rapid turnaround times for the results, and the growing demand for diagnostic kits.

Market Segmentation

The global precision diagnostics market share is classified into type, application, and end-user.

- The genetic tests segment dominates the market with the largest market share through the forecast period.

Based on the type, the global precision diagnostics market is categorized into genetic tests, esoteric tests, and others. Among these, the genetic tests segment dominates the market with the largest market share through the forecast period. When a greater number of individuals are aware of the need for early disease diagnosis, the genetic tests portion of the market. This test is useful in many fields of medicine as it searches for variations or mutations in the DNA. Genetic testing, for instance, can identify a hereditary disorder like Huntington's disease or Fragile X syndrome as well as provide information regarding a person's risk of acquiring cancer.

- The oncology segment is anticipated to grow at the fastest CAGR growth through the forecast period.

Based on the application, the global precision diagnostics market is categorized into oncology, cardiovascular, immunology, neurology, and others. Among these, the oncology segment is anticipated to grow at the fastest CAGR growth through the forecast period. The range of oncology diagnostic and treatment options has rapidly changed in recent years due to precision medicine. For a variety of reasons, cancer is the focus of numerous precision medicine organizations. Cancer is a disease of the genome, and tumors can be studied to understand the genetic alterations associated with a particular cancer patient.

- The clinical laboratories segment accounted for the largest revenue share through the forecast period.

Based on the end-user, the global precision diagnostics market is categorized into hospitals, clinical laboratories, and home care. Among these, the clinical laboratories segment accounted for the largest revenue share through the forecast period. With the rising expense of healthcare and the demand for more easily accessible diagnostic services, disruptive innovations are becoming more common in the era of precision diagnostics. These innovations upend established markets and establish new ones by offering unique values. Clinical laboratories are equipped with highly modern technologies that present advantageous growth potential compared to hospitals and home care.

Regional Segment Analysis of the Global Precision Diagnostics Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

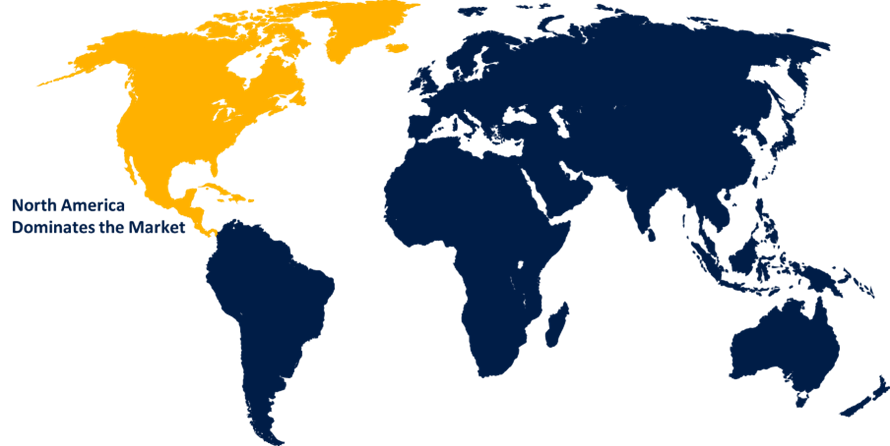

North America is anticipated to hold the largest share of the global precision diagnostics market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the global precision diagnostics market over the predicted timeframe. The global market share is expected to be taken by North America. This dominance can be attributed to the growing number of public-private partnerships. The United States of America is well-known for its cutting-edge healthcare system and large biotechnology research industries. Personalized diagnostics technologies have been improved through ongoing investments and advancements in these fields, rendering them more dependable and efficient. The market has grown greatly as a result of government initiatives in North America to improve the quality and accessibility of healthcare as well as funding for diagnostics-related research and development.

Asia Pacific is expected to grow at the fastest CAGR growth of the global precision diagnostics market during the forecast period. The need for better diagnostic techniques that offer specific treatment options is driven by the rising prevalence of chronic diseases like diabetes and cancer in this region. This rapid growth is partly due to patients' and healthcare providers' increasing awareness of and acceptance of precision diagnostics. The market expansion is further supported by government programs targeted at adopting new healthcare technologies and improvements in healthcare infrastructure, primarily in developing nations like China and India.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global precision diagnostics market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers AG

- Thermo Fisher Scientific Inc.

- bioMérieux SA

- Becton, Dickinson, and Company

- Danaher Corporation

- Quest Diagnostics

- Diatech Pharmacogenetics

- Swiss Precision Diagnostics

- Koninklijke Philips N.V

- Lantheus Medical Imaging, Inc.

- HALO Precision Diagnostics, Inc

- Agilent Technologies Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In January 2024, Siemens Healthineers & the Indian Institute of Science launched a collaborative laboratory for AI in Precision Medicine. The lab's official name is the Siemens Healthineers-Computational Data Sciences Collaborative Laboratory for AI in Precision Medicine. The lab's main focus is on developing open-source AI tools to analyze neurological diseases. This collaboration is a significant development in AI research for India, specifically targeting neurovascular diseases.

- In June 2023, Diatech Pharmacogenetics, a provider of molecular diagnostic tools, signed a collaborative agreement with Janssen Pharmaceutica NV, a pharmaceutical business, to improve access to precision medicine for patients with bladder cancer. Diatech Pharmacogenetics, one of Europe's leading precision medicine firms, develops and manufactures In Vitro Diagnostic (IVD) oncology tests for a variety of solid tumors and blood cancers.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2033. Spherical Insights has segmented the global precision diagnostics market based on the below-mentioned segments:

Global Precision Diagnostics Market, By Type

- Genetic Tests

- Esoteric Tests

- Others

Global Precision Diagnostics Market, By Application

- Oncology

- Cardiovascular

- Immunology

- Neurology

- Others

Global Precision Diagnostics Market, By End User

- Hospitals

- Clinical Laboratories

- Homecare

Global Precision Diagnostics Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. Which are the key companies that are currently operating within the market?Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens Healthineers AG, Thermo Fisher Scientific Inc., bioMérieux SA, Becton, Dickinson and Company, Danaher Corporation, Quest Diagnostics, Diatech Pharmacogenetics, Swiss Precision Diagnostics, Koninklijke Philips N.V,Lantheus Medical Imaging, Inc., HALO Precision Diagnostics, Inc., Agilent Technologies Inc., and Others.

-

2. What is the size of the global precision diagnostics market?The Global Precision Diagnostics Market Size is Expected to Grow from USD 74.98 Billion in 2023 to USD 254.48 Billion by 2033, at a CAGR of 13% during the forecast period 2023-2033.

-

3. Which region is holding the largest share of the market?North America is anticipated to hold the largest share of the global precision diagnostics market over the predicted timeframe.

Need help to buy this report?