Global Polyetheramine Market Size, Share, and COVID-19 Impact Analysis, By Type (Monoamine, Diamine, and Triamine), By Application (Polyurea, Fuel Additives, Composites, Epoxy Coatings, Adhesives and Sealants, and Others), By End-User (Automotive, Building and Construction, Wind Energy, Electronics and Electrical, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Polyetheramine Market Size Insights Forecasts to 2035

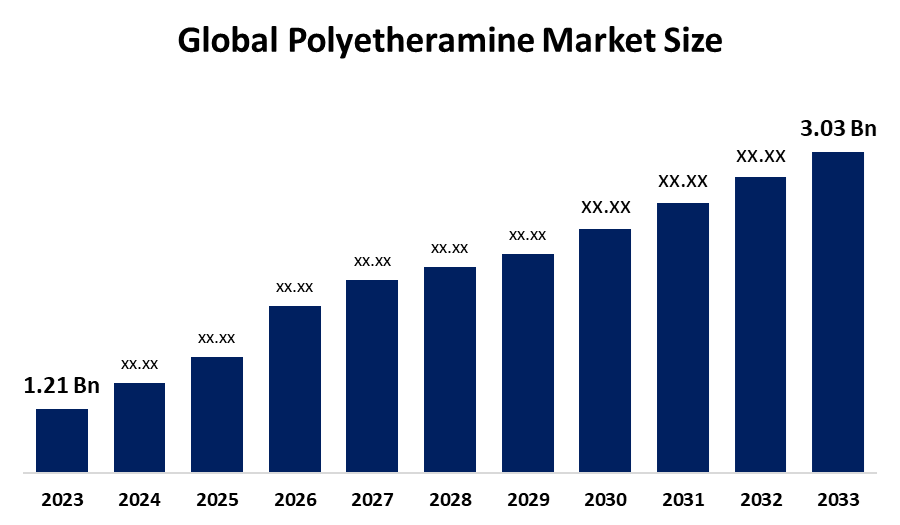

- The Global Polyetheramine Market Size Was Estimated at USD 1.21 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 8.7% from 2025 to 2035

- The Worldwide Polyetheramine Market Size is Expected to Reach USD 3.03 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a Research Report Published by Spherical Insights and Consulting, The Global Polyetheramine Market Size was worth around USD 1.21 Billion in 2024 and is predicted to Grow to around USD 3.03 Billion by 2035 with a compound annual growth rate (CAGR) of 8.7% from 2025 to 2035. The worldwide Polyetheramine Market Size experiences growth because demand for high-performance epoxy coatings in construction projects, the wind energy infrastructure market and the automotive/EV industry requires lightweight composites that provide exceptional durability and flexibility and quick curing time.

Market Overview

Polyetheramine is a chemical product defined by a polyether backbone with primary amino groups, serving as a critical high-performance curing agent and modifier in epoxy systems and polyurea formulations. The low viscosity and simple processing make polyetheramine suitable for use in multiple applications, which include epoxy coatings, structural composites, adhesives and sealants, fuel additives and wind energy components. The wind energy sector is experiencing major growth, with installed capacity reaching 743 GW, and turbine blades longer than 100 meters require polyetheramine-cured epoxies to ensure mechanical strength and durability during large-scale processing. According to the International Energy Agency, renewable power additions increased by 50% to reach 510 GW in 2023, which establishes a continuing need for materials that require advanced development.

The construction industry drives market growth because U.S. construction spending increased by 6.4% between May 2023 and May 2024, which created higher demand for epoxy flooring and polyurea coatings. The market needs bio-based polyetheramines because they cut carbon emissions while their use extends to 3D printing lightweight electric vehicle parts and modern adhesive development. The Asia-Pacific region controlled 53.42% of the market in 2025 because companies expanded their operations through projects like BASF’s Nanjing plant, which is now able to produce 18,800 tons of products each year. The market presents opportunities through bio-based products and 3D printing applications, and the increasing funding for e-mobility projects.

Report Coverage

This research report categorizes the Polyetheramine Market Size based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Polyetheramine Market Size. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Polyetheramine Market Size.

Polyetheramine Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 1.21 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 8.7% |

| 2035 Value Projection: | USD 3.03 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 230 |

| Tables, Charts & Figures: | 120 |

| Segments covered: | By Type, By Application |

| Companies covered:: | Clariant AG, Huntsman Corporation, BASF SE, Evonik Industries AG, Wuxi Acryl Technology Co., Ltd., Qingdao IRO Surfactant Co., Ltd., The Aurora Chemical Co. Ltd., Yantai Minsheng Chemicals Co., Ltd., Zibo Xinye Chemical Co., Ltd, Yangzhou Chenhua New Material Co., Ltd., PALMER HOLLAND, Yantai Dasteck Chemicals Co., Ltd., and other key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global Polyetheramine Market Size exists because the automotive and construction industries require high-performance adhesives, which serve as sealants and coatings for their applications. The automotive industry produced about 93 million vehicles during 2023, which created an increased demand for lightweight composites and strong epoxy systems. The construction industry benefits from protective coatings and flooring applications, which use polyetheramines, as worldwide infrastructure spending exceeded USD 13 trillion during 2024. The oil and gas exploration market will expand through upstream investments, which will reach USD 500 billion during 2024, which creates additional demand for fuel additives and pipeline coatings. The industrial sector expansion leads to an increase in global polyetheramine consumption.

Restraining Factors

The global Polyetheramine Market Size faces restraints from high production costs and raw material price volatility (e.g., propylene oxide), which squeezed manufacturer margins by 38% between 2021 and 2023. Stringent environmental regulations, such as REACH, increase compliance costs, while technical limitations, such as poor UV stability, restrict use in premium coatings.

Market Segmentation

The Polyetheramine Market Size share is classified into type, application, and end-user.

- The diamine segment dominated the market in 2024, approximately 51% and is projected to grow at a substantial CAGR during the forecast period.

Based on the type, the Polyetheramine Market Size is divided into monoamine, diamine, and triamine. Among these, the diamine segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment maintains its leading position because it functions as the primary element of epoxy systems that produce high strength, flexibility, and thermal resistance. The construction and wind energy sectors use diamine-based polyetheramines because they provide excellent performance for coatings, adhesives and composite materials. The industrial sector worldwide experiences increased material adoption because infrastructure development and the need for long-lasting weatherproof products keep growing.

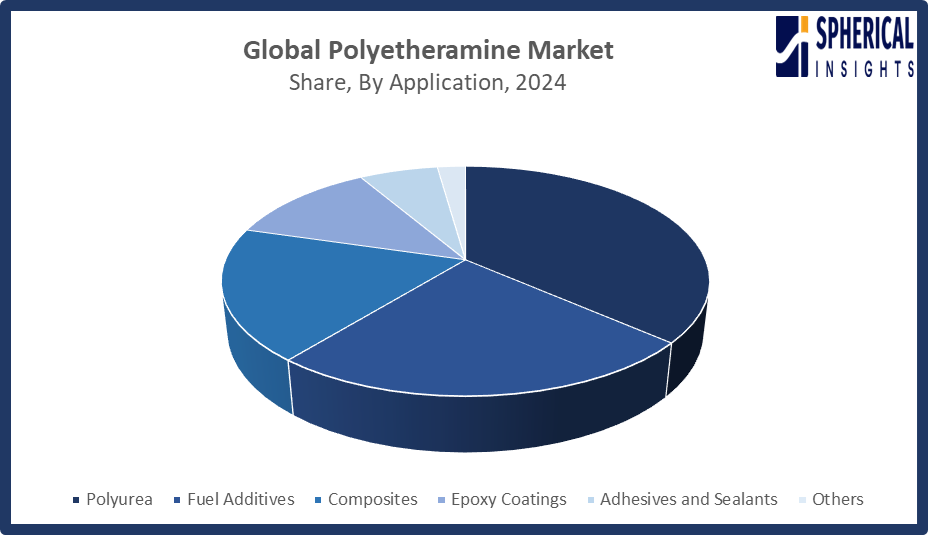

The polyurea segment accounted for the largest share in 2024, approximately 36% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the Polyetheramine Market Size is divided into polyurea, fuel additives, composites, epoxy coatings, adhesives and sealants, and others. Among these, the polyurea segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The increasing use of polyetheramine for polyurea coatings, linings and elastomers led to this material dominance. The material provides fast curing and high abrasion resistance together with strong chemical protection, making it suitable for industrial applications in flooring, pipelines and tanks. The segment experienced growth because the construction, automotive and marine industries required systems that offered durable and corrosion-resistant solutions with fast return on investment.

Get more details on this report -

- The wind energy segment accounted for the highest market revenue in 2024, approximately 30% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end-user, the Polyetheramine Market Size is divided into automotive, building and construction, wind energy, electronics and electrical, and others. Among these, the wind energy segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The wind energy segment achieved maximum market expansion as worldwide installations increased to 117 GW of new capacity during 2024, which brought total cumulative capacity above 740 GW. The need for high-performance polyetheramine-based epoxy composites used in light and strong wind structures increased because turbine blades now measure more than 100 meters.

Regional Segment Analysis of the Polyetheramine Market Size

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

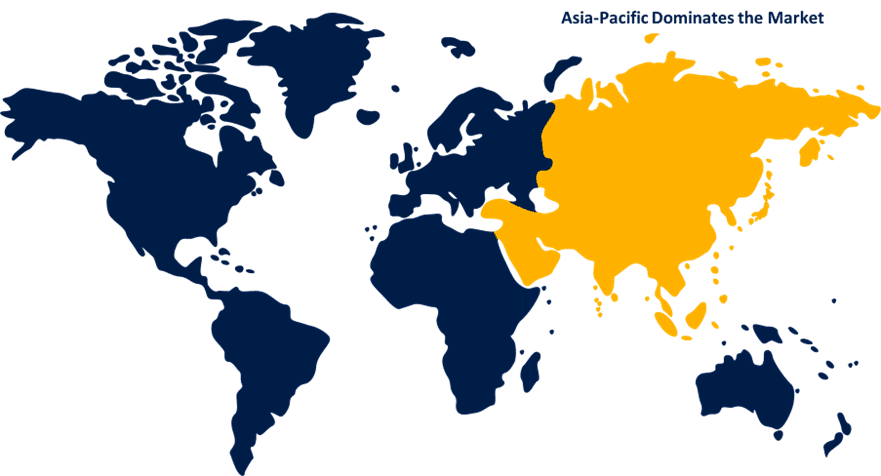

Asia Pacific is anticipated to hold the largest share of the Polyetheramine Market Size over the predicted timeframe.

Get more details on this report -

Asia Pacific is anticipated to hold the largest share of the Polyetheramine Market Size over the predicted timeframe. Asia Pacific is anticipated to hold the largest share of the Polyetheramine Market Size, contributing approximately 53% of global revenue in 2024, driven by rapid industrialization and renewable energy expansion. China leads the market because its wind capacity reached 440 GW, which allows for the production of composite blades. India's installation of 25 GW of renewable energy capacity during 2024 created increased demand for epoxy curing agents and coatings. Japan and South Korea make their contributions through their production of advanced automotive and electronics items. The regional polyetheramine consumption receives continuous support from increasing infrastructure investments and the rapid growth of construction activities in these nations. In February 2026, the Government of India allocated INR 20,000 crore (USD 2.4 billion) in the Union Budget 2026-27 to support CCUS and Chemical Parks, strengthening sustainable chemical manufacturing and domestic specialty chemical supply chains, including polyetheramine materials.

North America is expected to grow at a rapid CAGR in the Polyetheramine Market Size during the forecast period. The North American market for polyetheramine products is expected to have a 24% share growth due to increasing renewable energy development, infrastructure improvements and oil and gas sector spending. The United States leads regional growth because it has installed more than 100 GW of wind energy capacity, which creates a market need for epoxy composite materials. US construction expenditure saw a roughly 6% annual increase during 2024, which resulted in higher demand for coatings and polyurea products. The Canadian wind energy sector and infrastructure development projects create a stronger need for high-performance polyetheramine materials in the region.

The Polyetheramine Market Size in Europe shows continuous development because of strict environmental rules that require low-VOC materials, and because of substantial investments in wind power and renewable energy infrastructure. Germany leads as the top country because more than 60% of epoxy-based wind turbine blade adhesives use polyetheramines to achieve durability. The country's market growth is further propelled by robust automotive and industrial manufacturing sectors demanding high-performance coatings and adhesives.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Polyetheramine Market Size, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Clariant AG

- Huntsman Corporation

- BASF SE

- Evonik Industries AG

- Wuxi Acryl Technology Co., Ltd.

- Qingdao IRO Surfactant Co., Ltd.

- The Aurora Chemical Co. Ltd.

- Yantai Minsheng Chemicals Co., Ltd.

- Zibo Xinye Chemical Co., Ltd

- Yangzhou Chenhua New Material Co., Ltd.

- PALMER HOLLAND

- Yantai Dasteck Chemicals Co., Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In November 2025, the European Commission advanced its Clean Industrial Deal to strengthen low-carbon industry competitiveness. The initiative supports clean technology procurement, targets nearly 100 GW annual renewable additions, and provides funding via the EU Innovation Fund and Industrial Decarbonisation Bank, boosting demand for advanced composite materials in wind and infrastructure sectors.

- In July 2025, Evonik Industries shifted its Crosslinkers epoxy curing agent plants in Marl, Clayton, Isehara, Los Angeles, and Singapore to 100% renewable electricity. The move cuts Scope 1 and 2 emissions by about one-third annually, supporting its 25% reduction target by 2030 and climate neutrality by 2050.

- In December 2023, BASF completed a specialty amines capacity expansion at its Geismar, Louisiana, site. The upgrade increases production of Baxxodur polyetheramines and Lupragen amine catalysts, supporting wind, coatings, adhesives, and polyurethane applications, while advancing low-VOC and sustainable formulation solutions.

- In February 2023, Huntsman Corporation launched new products at the European Coatings Show, including POLYRESYST IC6005, a low-VOC intumescent polyurethane system for fire protection. The company also introduced a bio-based coating and JEFFAMINE M-3085 amine, expanding its advanced polyetheramine portfolio for dispersants and epoxy applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Polyetheramine Market Size based on the below-mentioned segments:

Global Polyetheramine Market Size, By Type

- Monoamine

- Diamine

- Triamine

Global Polyetheramine Market Size, By Application

- Polyurea

- Fuel Additives

- Composites

- Epoxy Coatings

- Adhesives and Sealants

- Others

Global Polyetheramine Market Size, By End-User

- Automotive

- Building and Construction

- Wind Energy

- Electronics and Electrical

- Others

Global Polyetheramine Market Size, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. How is the rising demand for wind energy impacting the consumption of polyetheramines in composite rotor blades?Rising wind energy demand boosts polyetheramine use in composite rotor blades; global wind capacity topped 743 GW in 2024, requiring larger blades cured with polyetheramine-based epoxies for durability and strength.

-

2. What role do polyetheramines play in the formulation of low-VOC, eco-friendly coatings and adhesives?Polyetheramines enhance low-VOC, eco-friendly coatings and adhesives by improving adhesion, cure efficiency, and durability; demand for such sustainable formulations is growing with global low-VOC regulation adoption increasing over 15% annually.

-

3. How are raw material price fluctuations (like propylene oxide) affecting polyetheramine production costs and market pricing?Fluctuating raw material prices, particularly propylene oxide, have increased polyetheramine production costs by about 20-30% between 2021 and 2024, leading to higher market pricing and tighter margins for manufacturers.

-

4. What are the latest technological innovations in bio-based or sustainable polyetheramine production?Recent innovations include bio-based polyetheramine production using renewable feedstocks and biomass-balanced processes, reducing carbon footprint by up to 70-100%, while supporting industry sustainability goals and low-VOC formulation trends.

-

5. How are Chinese manufacturers like Wuxi Acryl and Yangzhou Chenhua expanding their production capacities to challenge global leaders?Chinese manufacturers are taking a strategic, risk-averse approach to expansion. Wuxi Acryl reduced its planned new capacity by 50% (from 20,000 to 10,000 tons) and delayed completion to December 2026. Conversely, Yangzhou Chenhua focuses on innovation, aiming to boost utilization rates by expanding small variety polyether amines for niche applications.

-

6. How is the trend toward lightweighting in the automotive and aerospace industries boosting polyetheramine demand?The lightweighting trend in automotive and aerospace is boosting polyetheramine demand for high-performance composites, with global composite use projected to grow 8% annually through 2030, reducing weight and improving fuel efficiency.

Need help to buy this report?