Global Oily Waste Can Market Size, Share, and COVID-19 Impact Analysis, By Material (Metal and Plastic), By Closure (Up to 6 Gallons, 7 to 14 Gallons and Above 14 Gallons), By End Use (Automotive, Manufacturing and Warehousing, Mining and Construction, Marine, and Other Industrial), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Oily Waste Can Market Size Insights Forecasts to 2035

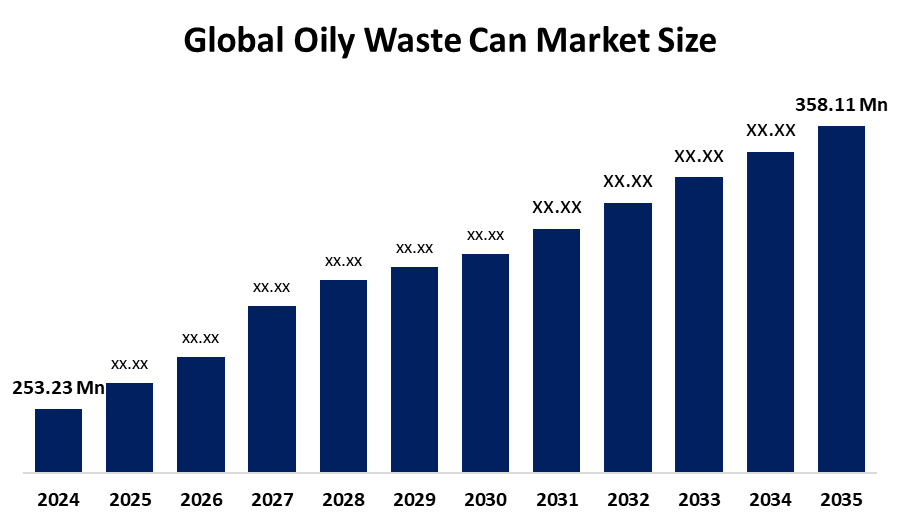

- The Global Oily Waste Can Market Size Was Estimated at USD 253.23 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 3.2% from 2025 to 2035

- The Worldwide Oily Waste Can Market Size is Expected to Reach USD 358.11 Million by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a Research Report Published by Spherical Insights and Consulting, The Global Oily Waste Can Market Size was worth around USD 253.23 Million in 2024 and is predicted to Grow to around USD 358.11 Million by 2035 with a compound annual growth rate (CAGR) of 3.2% from 2025 to 2035. The oily waste can market is expanding because industrial safety regulations have become more stringent, and workers now understand fire risks better, while businesses in manufacturing, automotive and construction need to dispose of hazardous oil-soaked waste according to established regulations.

Market Overview

The Global Oily Waste Can Market Size comprises specialized metal containers designed for the safe storage and disposal of oil-soaked rags, flammable wipes, and combustible industrial waste. Manufacturing plants, automotive workshops, oil and gas facilities, marine operations and chemical industries use these cans to decrease fire risks while meeting safety standards. Authorities enforce hazardous waste regulations through their fire safety requirements, which drive market expansion according to Environmental Protection Agency and Occupational Safety and Health Administration regulations. Oily waste production increases because global industrial output and vehicle manufacturing have reached production levels above 90 million units each year in recent years.

The growing workplace safety awareness, together with industrialization in the Asia Pacific, creates new business opportunities. The market growth for commercial and heavy industrial sectors is driven by corrosion-resistant self-closing lid designs and compliance-certified container development. The Lagos State Government established household-use cooking oil collection kiosks across the state through its February 2026 partnership with the Ministry of the Environment and Water Resources and LASEPA. The initiative, which receives support from Shell Foundation and operates through Ororo Waste Management, aims to decrease pollution while creating a $20 million biofuel market opportunity.

Report Coverage

This research report categorizes the oily waste can market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the oily waste can market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the oily waste can market.

Oily Waste Can Market Report Coverage

| Report Coverage | Details |

|---|---|

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 3.2% |

| 2035 Value Projection: | USD 358.11 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Material, By Closure |

| Companies covered:: | Justrite Mfg. Co., LLC, Eagle Manufacturing Company, Safetyware Group Berhad, Veolia Environment S.A., DENIOS, Inc., ESNICO Industry Co., Ltd., SYSBEL Industry & Technology Co., Ltd., DRIZIT Environmental, VWR International, LLC, HAZERO Company, Genex Container Pvt. Ltd., TENAQUIP Limited, Acklands Grainger, Brady Corporation, and other key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global oily waste can market is driven by stringent environmental regulations on hazardous waste disposal and rising industrialization worldwide. Agencies such as the Environmental Protection Agency mandate proper storage of oil-soaked rags and flammable waste, which creates a need for safety containers that meet regulations. The automotive servicing and manufacturing sectors experienced fast expansion, which led to an increase in vehicle production that reached 90 million units worldwide. The expansion of oil and gas operations, together with marine business activities, creates more oily waste materials. The Occupational Safety and Health Administration establishes workplace safety regulations, which drive companies to develop waste management solutions that prevent fire hazards, thus creating business opportunities in industrial and commercial facilities around the world.

Restraining Factors

The global oily waste can market faces restraints from high product costs and limited awareness in small-scale industries. The Environmental Protection Agency requires businesses to comply with its regulations, which results in increased costs for their operations. The manufacturing expenses of steel production have been affected by price fluctuations, which resulted in a 20% cost increase. This situation restricts budget-constrained enterprises from adopting the product.

Market Segmentation

The oily waste can market share is classified into material, closure, and end use.

- The metal segment dominated the market in 2024, approximately 69% and is projected to grow at a substantial CAGR during the forecast period.

Based on the material, the oily waste can market is divided into metal and plastic. Among these, the metal segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The metallic oily waste cans provide better value because their steel and iron construction creates strong waste storage containers that protect hazardous materials during transportation. The product serves daily industrial operations because it provides both economic value and environmentally friendly characteristics. The rising demand for metal cans stems from increasing public knowledge about safe packaging materials that do not cause cancer.

- The up to 6 gallons segment accounted for the largest share in 2024, approximately 28% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the closure, the oily waste can market is divided into up to 6 gallons, 7 to 14 gallons and above 14 gallons. Among these, the up to 6 gallons segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The demand for 6-gallon cans develops because these containers enable companies to handle their storage needs through easy access during production and warehouse activities. The product features a small design that prevents fire hazards while enabling organizations to meet safety requirements, decrease spills and boost operational efficiency with uninterrupted business operations, which leads to widespread use in industrial settings.

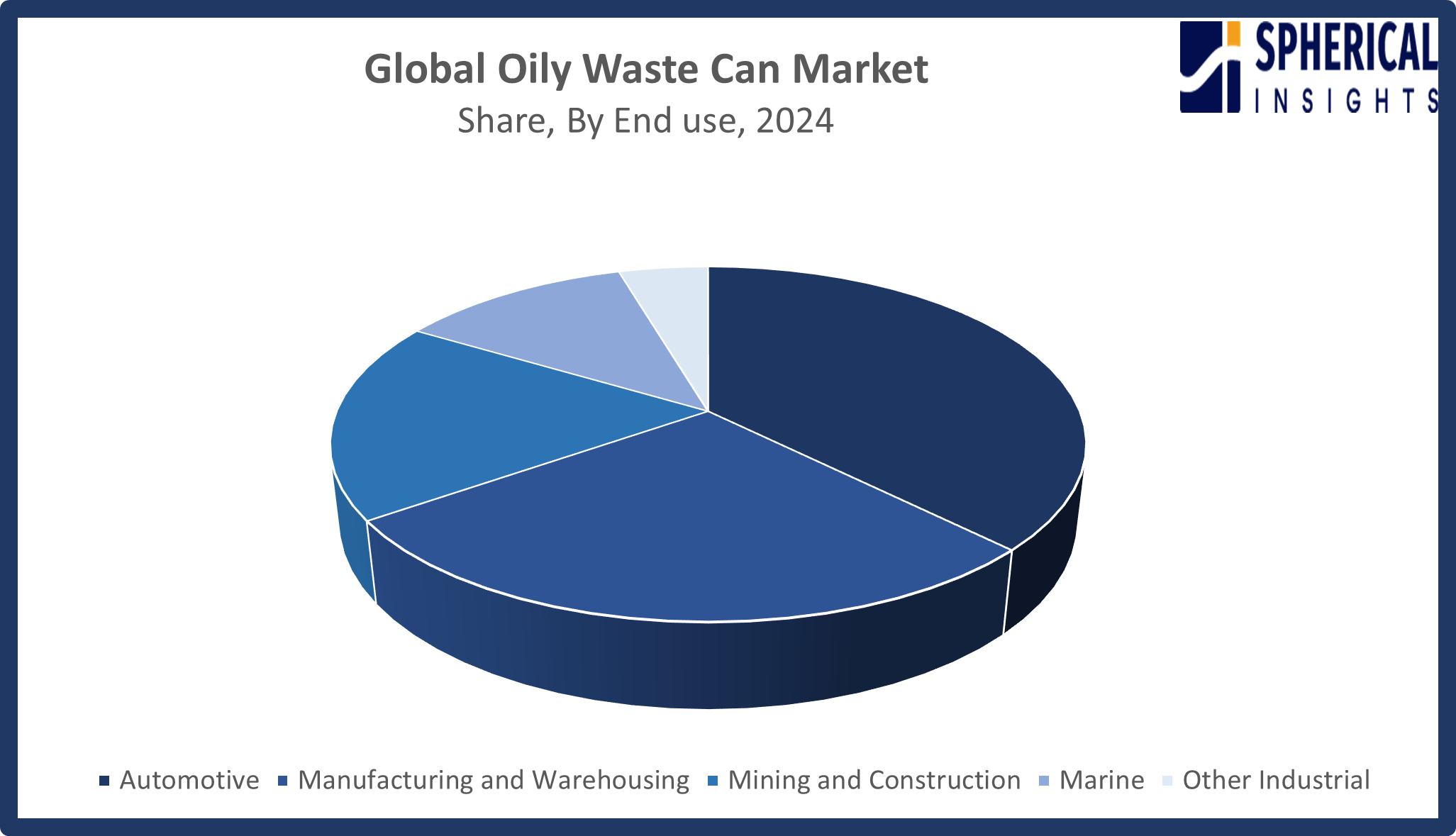

- The manufacturing and warehousing segment accounted for the highest market revenue in 2024, approximately 37% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end use, the oily waste can market is divided into automotive, manufacturing and warehousing, mining and construction, marine, and other industrial. Among these, the manufacturing and warehousing segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The manufacturing and warehousing industries generate high quantities of oily and combustible waste, which drives growth in this market segment. The usage of standardized cans protects against fire hazards while stopping contamination and maintaining safety requirements. The industrial development process requires companies to improve their safety practices, which leads to higher operational productivity through increased industrial expansion activities that boost market demand for their products.

Get more details on this report -

Regional Segment Analysis of the Oily Waste Can Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

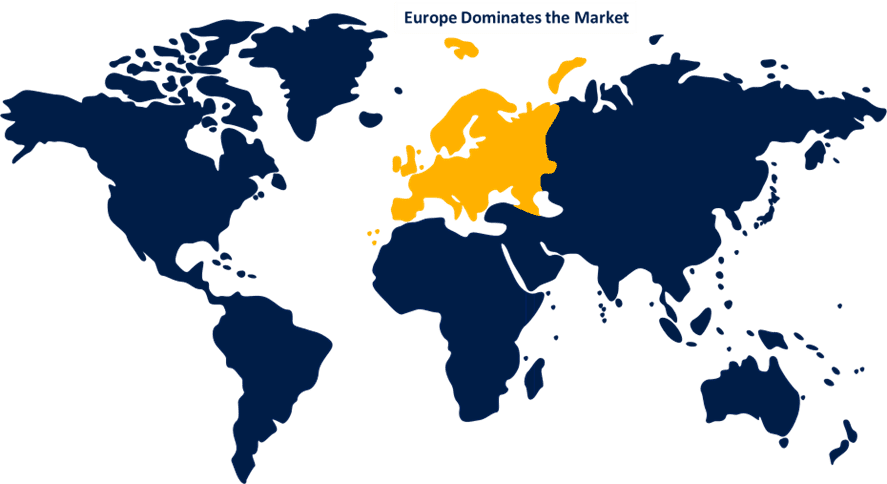

Europe is anticipated to hold the largest share of the oily waste can market over the predicted timeframe.

Get more details on this report -

Europe is anticipated to hold the largest share of the oily waste can market over the predicted timeframe. The European market will become the largest global oily waste can market during 2024 because industrial facilities need to adopt the safe disposal of flammable materials, which arises from strict workplace safety and hazardous waste regulations. Europe maintained 44.8% of worldwide market revenue during 2024 because established industrial sectors in Germany and the United Kingdom required compliance with fire safety standards and environmental protection. The strong system of regulations, together with active manufacturing operations, creates ongoing needs for certified oily waste containment products that meet compliance requirements throughout the region.

North America is expected to grow at a rapid CAGR in the oily waste can market during the forecast period. The oily waste can market will experience rapid growth in North America because companies need to follow workplace safety rules and fire-hazard regulations, which OSHA and EPA enforce, to gain approval for their operations. The United States and Canada’s expanding industrial activities, including automotive, manufacturing, and maintenance sectors, further drive demand for fire-resistant, certified waste cans, supporting faster market growth. The North American market maintains more than 30% market share because safety awareness and regulatory requirements together create strong growth throughout the region. Under Senate Bill 158 (2021), California’s DTSC must issue triennial Hazardous Waste Reports and, from March 2025, submit a comprehensive Management Plan to the Board of Environmental Safety, updated October 29, 2025.

The oily waste can market in the Asia Pacific experienced significant expansion due to industrial growth and manufacturing development in China and India created hazardous waste and oily waste disposal needs. The region requires certified waste cans because safety awareness increases and international fire-safety standards become accepted. The hazardous waste sector drives strong growth in the entire industrial and hazardous waste management markets of the Asia Pacific. The Ministry of Environment in India published the Solid Waste Management Rules 2026 in February 2026, which require four-stream segregation and digital reporting and polluter-pays accountability to improve hazardous waste compliance across the country starting from April 1.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the oily waste can market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Justrite Mfg. Co., LLC

- Eagle Manufacturing Company

- Safetyware Group Berhad

- Veolia Environment S.A.

- DENIOS, Inc.

- ESNICO Industry Co., Ltd.

- SYSBEL Industry & Technology Co., Ltd.

- DRIZIT Environmental

- VWR International, LLC

- HAZERO Company

- Genex Container Pvt. Ltd.

- TENAQUIP Limited

- Acklands Grainger

- Brady Corporation

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In July 2025, the European Commission unveiled the EU Chemicals Industry Action Plan to enhance competitiveness and sustainability. The plan introduces fiscal incentives, simplified regulations, and support for clean technologies, strengthening production of key chemical intermediates, including glacial acetic acid, while promoting decarbonisation and industrial resilience across Europe

- In December 2024, QMRE partnered with Eagle Technology to deploy the first VÍXLA thermolysis system in Hoo, targeting 6,600 tonnes of annual plastic waste processing. Each unit converts 1kg of plastic into 1 litre of pyro-oil. At full scale, 100 sites could recycle 600,000 tonnes annually.

- In January 2024, Eagle Technology globally launched Víxla at EXPO360 Bio in Nantes. The decentralized chemical recycling system converts plastic waste into high-quality energy, reducing transport needs and environmental impact. Víxla has attracted strong global interest as a sustainable solution to the growing plastic waste crisis.

- In July 2021, SYSBEL launched Oily Waste Cans to address safe temporary storage of hazardous and flammable waste from industrial and laboratory activities. Designed to prevent fire risks and chemical leaks, the cans comply with OSHA and CE standards, featuring wide openings and high-visibility warning colors.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the oily waste can market based on the below-mentioned segments:

Global Oily Waste Can Market, By Material

- Metal

- Plastic

Global Oily Waste Can Market, By Closure

- 6 Gallons

- 7 to 14 Gallons

- Above 14 Gallons

Global Oily Waste Can Market, By End Use

- Automotive

- Manufacturing and Warehousing

- Mining and Construction

- Marine

- Other Industrial

Global Oily Waste Can Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What role do innovations in fire-resistant and self-closing lid technologies play in enhancing product adoption?Innovations in fire-resistant materials and self-closing lid technologies significantly enhance oily waste can safety and compliance. Facilities using these features report up to 30% fewer fire incidents and 25% lower insurance costs, boosting product adoption across industrial and commercial sectors.

-

2. How do stringent environmental and fire safety regulations impact the growth of the global oily waste can market?Stringent environmental and fire safety regulations drive market growth by requiring compliant waste containment; facilities adhering to these standards show up to 40% reduction in hazardous incidents, increasing the demand for oily waste.

-

3. What is driving the shift toward color-coded waste cans for easier waste segregation?The shift toward color-coded waste cans is driven by stricter segregation regulations and efficiency goals, with facilities reporting up to 25% faster sorting accuracy, improving compliance and reducing cross-contamination risks in waste management.

-

4. How are smart waste management and IoT-enabled monitoring systems transforming the market landscape?Smart waste management and IoT-enabled monitoring systems are transforming the market by increasing collection efficiency and predictive maintenance; facilities using these technologies report up to 35% reduction in overflow incidents and 20% lower operational costs, enhancing safety and overall waste handling performance.

-

5. What factors are driving the growth of the Oily Waste Can market?The need for agricultural fumigation, crop protection, growing electronics and semiconductor applications, use as a reducing agent in the chemical and metal sectors, and new prospects in sophisticated technologies and renewable energy are the main factors propelling the Oily Waste Can market.

-

6. What role does antimicrobial coating technology play in new waste can designs?Antimicrobial coating technology in oily waste cans inhibits bacterial growth and contamination, enhancing hygiene and workplace safety. Facilities adopting these coatings report up to 50% fewer microbial surface incidents, improving sanitation and reducing maintenance costs in industrial and commercial environments.

-

7. How does increasing workplace safety awareness influence purchasing decisions in industrial facilities?Increasing workplace safety awareness drives purchasing of compliant waste solutions, with companies reporting up to 45% fewer safety violations after adopting certified oily waste cans, making safety performance a key procurement criterion.

-

8. How are lean manufacturing practices affecting waste can capacity preferences in factories?Lean manufacturing practices favor smaller, more frequent waste disposal, increasing demand for up to 6-gallon cans, and factories report 20-30% faster waste handling and improved workflow efficiency with compact capacities.

Need help to buy this report?