Global Obesity GLP-1 Market Size, Share, and COVID-19 Impact Analysis, By Drug Type (Semaglutide, Tirzepatide, Liraglutide, and Emerging Oral GLP-1s), By Route of Administration (Parenteral and Oral), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: HealthcareKey Market Trends & Opportunities

The obesity GLP-1 market has a number of opportunities to grow, due to the expanding manufacturing, development of oral formulations, combination therapies, and management of long-term treatment costs.

- Research on newer agents emphasizing weight loss and cardiovascular outcomes

- Investment in manufacturing for addressing significant demand-supply mismatch

Global Obesity GLP-1 Market Insights Forecasts to 2035

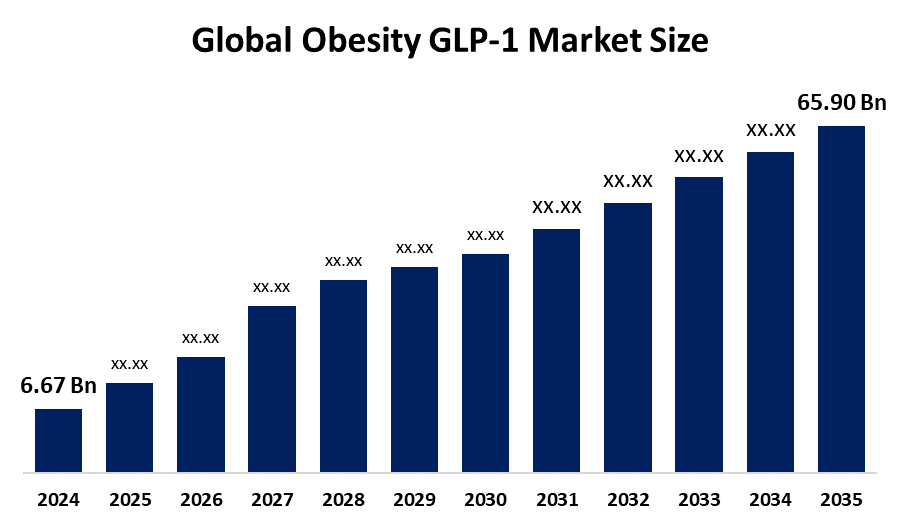

- The Global Obesity GLP-1 Market Size Was Estimated at USD 6.67 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 23.15% from 2025 to 2035

- The Worldwide Obesity GLP-1 Market Size is Expected to Reach USD 65.90 Billion by 2035

Get more details on this report -

Major Players

Novo Nordisk A/S, Eli Lilly and Company, Amgen, Viking Therapeutic, AstraZeneca, Roche (Carmot Therapeutics), Boehringer Ingelheim, Pfizer Inc., Altimmune, Inc., and Structure Therapeutics

Market Overview

The global industry of obesity GLP-1 is a rapidly expanding pharmaceutical sector driven by high efficacy, weekly injection drugs, primarily Wegovy (semaglutide) and Zepbound (tirzepatide), mimicking gut hormones to suppress appetite. GLP-1 receptor agonists provide significant, long-term weight loss (15-25% on average) by regulating food intake in the brain. Obesity is a global epidemic which results in increased morbidity and mortality and so timely treatment is of paramount importance. Treatment with novel agents targeting the GLP-1 receptor (liraglutide and semaglutide) leads to clinically meaningful and sustained weight loss.

Innovation and market expansion are anticipated as a result of major players' growing R&D expenditures and expanding partnerships. For instance, in October 2025, Knownwell picked up $25 million in fresh funding, riding the wave of investment in obesity care. CVS Health Ventures led the round with participation from MassMutual Catalyst Fund and Intermountain Ventures.

Report Coverage

This research report categorizes the obesity GLP-1 market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the obesity GLP-1 market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the obesity GLP-1 market.

Global Obesity GLP-1 Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 6.67 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 23.15% |

| 2035 Value Projection: | USD 65.90 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 112 |

| Segments covered: | By Drug Type, By Route of Administration and By Region |

| Companies covered:: | Novo Nordisk A/S, Eli Lilly and Company, Amgen, Viking Therapeutic, AstraZeneca, Roche (Carmot Therapeutics), Boehringer Ingelheim, Pfizer Inc., Altimmune, Inc., Structure Therapeutics, Others |

| Pitfalls & Challenges: | Covid 19 Impact Challanges, Future, Growth and Analysis |

Get more details on this report -

Driving Factors

Increasing prevalence of obesity

According to the WHO, in the year 2022, 2.5 billion adults (18 years and older) were overweight, and in 2024, 35 million children under the age of 5 were overweight. An increased global obesity is the primary driving factor of obesity GLP-1 market demand.

Strong clinical evidence

Several emerging oral compounds for weight reduction are currently under clinical evaluation, including oral glucagon-like peptide 1 (GLP-1) receptor agonists. Recently, a new drug application for oral semaglutide, would be the first oral drug authorized for long-term weight management.

Strong investment in next-generation GLP-1 combinations

An increasing investment in increasing emphasis on improving weight loss efficacy, with increased emphasis on developing formulations, is propelling the market. For instance, in October 2024, Kailera Therapeutics launched into the increasingly crowded obesity space with a portfolio of assets acquired from China and $400 million in Series A funds

Restraining Factors

Limited reimbursement policies

Reimbursement for GLP-1 agonists for obesity is evolving but remains heavily restricted due to high costs, with only 1 in 5 US state Medicaid programs covering anti-obesity medications as of 2023. Coverage often requires strict BMI criteria and documentation of lifestyle intervention.

Market Segment Insights

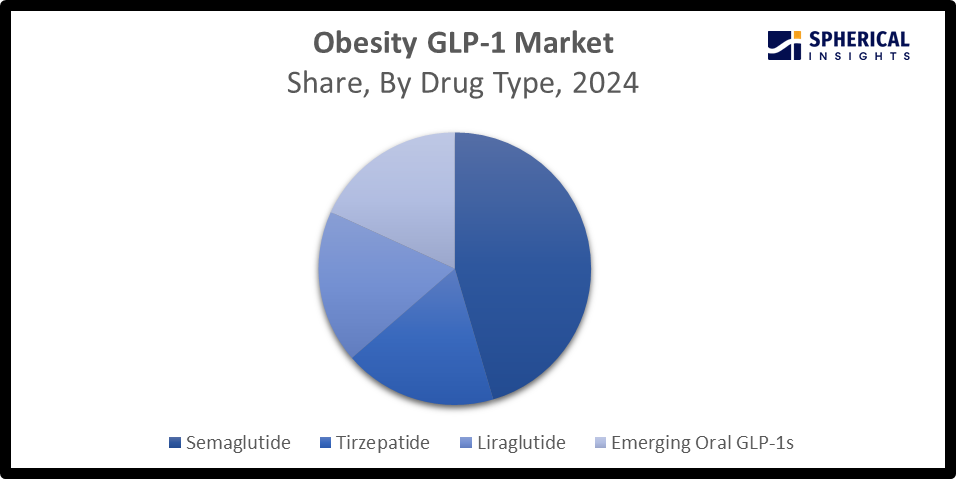

By Drug Type: Semaglutide (Dominant) versus Tirzepatide (Fastest Growing)

The semaglutide segment dominated the market with the largest over 50.0% in 2024, due to its robust clinical efficacy in glycemic control and weight loss. Semaglutide is a highly effective GLP-1 receptor agonist that treats obesity by suppressing appetite and increasing satiety. It mimics the GLP-1 hormone, reducing caloric intake and managing obesity-related comorbidities. While the tirzepatide segment is growing at the fastest CAGR, owing to the dual GIP and GLP-1 receptor mechanism that offers better results for weight loss. Tirzepatide is a highly effective, once-weekly dual agonist that significantly reduces body weight, often exceeding 20% in adults with obesity or overweight, with safety profile similar to other incretin-based therapies.

Get more details on this report -

By Route of Administration: Parenteral (Dominant) versus Oral (Fastest Growing)

The parenteral segment dominated the market with the largest share of over 80.0% in 2024, due to its precise dosing, rapid absorption, and sustained therapeutic effects. Parenteral GLP-1 receptor agonists are highly effective medications for obesity management, primarily administered via subcutaneous injection for promoting weight loss, reducing appetite and increasing satiety. The oral segment is growing rapidly in the market, owing to the growing need for convenient, needle-free treatment options that improve patient adherence. For instance, oral semaglutide (Rybelsus) is the first GLP-1 receptor agonist available as a daily pill for chronic weight management. It acts as an appetite suppressant and aids weight loss, similar to injectable counterparts.

Regional Segment Analysis of the Obesity GLP-1 Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the obesity GLP-1 market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of over 50.0% in the obesity GLP-1 market over the predicted timeframe. The market ecosystem in North America is strong, with increasing obesity prevalence and growing insurance coverage for weight management drugs. Further, the demand for obesity GLP-1 has been driven by the obesity focused label expansion and coverage gains, as well as cardiometabolic outcome-based guideline inclusion. The United States is the dominant country in the North America obesity GLP-1 market, owing to massive demand for both injectable and new oral treatment, with significant growth in insurance coverage and lowered prices.

Asia Pacific is expected to grow at a rapid CAGR of about 16.0% in the obesity GLP-1 market during the forecast period. The Asia Pacific area has a thriving market for obesity GLP-1 due to the region’s increasing obesity rate, treatment accessibility, and increasing physician familiarity with GLP-1 medications. Due to their governments' increasing investment in healthcare infrastructure, there is increasing market growth. China is the leading country in the Asia Pacific market, holding the dominant share, owing to the increasing prevalence of type 2 diabetes, along with the growing urbanization and ageing population.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Obesity GLP-1 market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Novo Nordisk A/S

- Eli Lilly and Company

- Amgen

- Viking Therapeutic

- AstraZeneca

- Roche (Carmot Therapeutics)

- Boehringer Ingelheim

- Pfizer Inc.

- Altimmune, Inc.

- Structure Therapeutics

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Industry Development

- In February 2026, Pfizer Inc. announced positive topline results from the Phase 2b VESPER-3 study investigating monthly maintenance dosing of its fully-biased, ultra-long-acting, injectable GLP-1 receptor agonist (RA) PF’3944 (MET-097i) in adults with obesity or overweight without type 2 diabetes.

- In February 2026, Novo Nordisk launched its first-ever big game commercial featuring the new once-daily Wegovy (semaglutide) tablets 25 mg. Wegovy pill is used with a reduced calorie diet and increased physical activity for adults with obesity, or with overweight who also have weight-related medical problems, to help them lose weight and keep it off.

- In September 2025, Pfizer announced a plan to buy Metsera, a little-known US biotech startup, for $4.9 bn (£3.6bn).

- In December 2024, Eli Lilly and Company announced a $3 billion expansion to its injectable product manufacturing site. The facility produces glucagon-like peptide-1 (GLP-1) drug products, which are used to treat diabetes and obesity.

- In June 2024, Eli Lilly and Company announced detailed results from ACHIEVE-1, a Phase 3 trial evaluating the safety and efficacy of orforglipron compared to placebo in adults with type 2 diabetes and inadequate glycemic control with diet and exercise alone.

- In May 2024, Hims & Hers Health, Inc., the leading health and wellness platform, announced the addition of GLP-1 injections to its comprehensive weight loss portfolio, giving customers an affordable way to consistently access safe, high-quality weight loss treatment.

- In May 2024, Roundhill Investments, an ETF sponsor focused on innovative financial products, announced the launch of the Roundhill GLP-1 & Weight Loss ETF (OZEM), which began trading on Nasdaq.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the obesity GLP-1 market based on the below-mentioned segments:

Global Obesity GLP-1 Market, By Drug Type

- Semaglutide

- Tirzepatide

- Liraglutide

- Emerging Oral GLP-1s

Global Obesity GLP-1 Market, By Route of Administration

- Parenteral

- Oral

Global Obesity GLP-1 Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the obesity GLP-1 market?The global Obesity GLP-1 market size is expected to grow from USD 6.67 Billion in 2024 to USD 65.90 Billion by 2035, at a CAGR of 23.15% during the forecast period 2025-2035.

-

2. Which region holds the largest share of the obesity GLP-1 market?North America is anticipated to hold the largest share of the Obesity GLP-1 market over the predicted timeframe.

-

3. What is the forecasted CAGR of the Global Obesity GLP-1 Market from 2024 to 2035?The market is expected to grow at a CAGR of around 23.15% during the period 2024–2035.

-

4. Who are the top companies that are involved in the Global Obesity GLP-1 Market?Key players include Novo Nordisk A/S, Eli Lilly and Company, Amgen, Viking Therapeutic, AstraZeneca, Roche (Carmot Therapeutics), Boehringer Ingelheim, Pfizer Inc., Altimmune, Inc., and Structure Therapeutics.

-

5. What are the main drivers in the obesity GLP-1 market?An increasing prevalence of diabetes and investment in next-generation GLP-1 combinations, are major market growth drivers of the obesity GLP-1 market.

-

6. What challenges are limiting the adoption of obesity GLP-1?Factors like the increased cost and limited reimbursement policies remain key restraints in the obesity GLP-1 market.

-

7. What are the key trends in the obesity GLP-1 market?Increasing research on newer agents focusing on weight loss and cardiovascular, along with investment in drug manufacturing, are major key trends in the obesity GLP-1 market.

Need help to buy this report?