North America Rapid Tests Market Size, Share, and COVID-19 Impact Analysis, By Product (Instruments, Consumables, and Others), By Technology (Molecular Diagnostics, Immunoassay, and Others), By End User (Hospitals and Clinics, Laboratories, At Home Testing, and Others), and North America Rapid Tests Market Insights, Industry Trend, Forecasts to 2035

Industry: HealthcareNorth America Rapid Tests Market Insights Forecasts to 2035

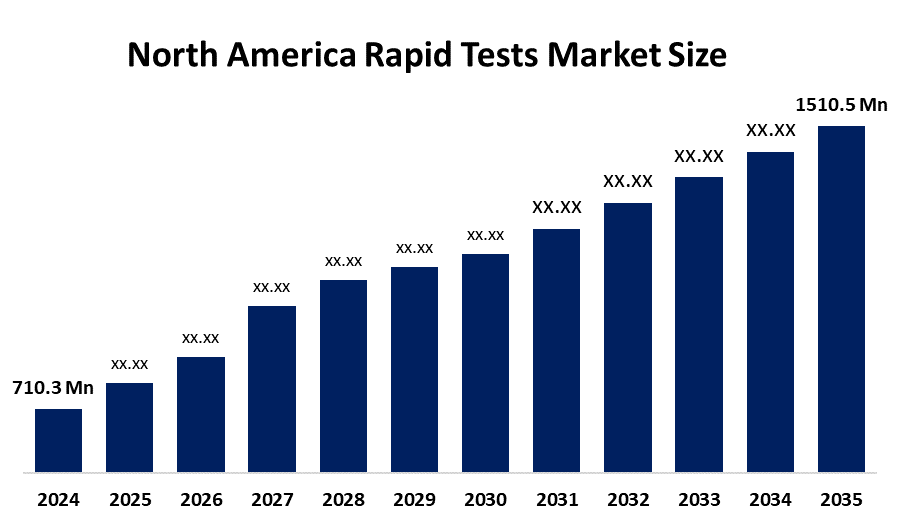

- The North America Rapid Tests Market Size Was Estimated at USD 710.3 Million in 2024

- The Market Size is Expected to Grow at a CAGR of Around 7.07% from 2025 to 2035

- The North America Rapid Tests Market Size is Expected to Reach USD 1510.5 Million by 2035

Get more details on this report -

According to a research report published by Spherical Insights & Consulting, The North America Rapid Tests Market Size is anticipated to reach USD 1510.5 Million by 2035, Growing at a CAGR of 7.07% from 2025 to 2035. The market is driven by the rising prevalence of chronic diseases, such as diabetes and cardiovascular diseases, streamlined regulatory pathway, and the IoT of diagnostic devices.

Market Overview

The North America rapid tests market refers to the development and commercialisation of medical diagnostic tools providing results within minutes at the point-of-care, which is experiencing robust growth, maintaining its position as the world's largest regional market. This sector is characterised by a shift toward decentralised, patient-centric care through innovations such as AI-integrated diagnostic algorithms, microfluidic lab-on-a-chip platforms, and multiplex panels capable of detecting multiple pathogens simultaneously.

Government incentives play a pivotal role in this expansion; agencies like BARDA provide significant funding for at-home molecular testing, while the FDA has streamlined regulatory pathways to fast-track the approval of next-generation assays. Furthermore, public health initiatives and grants for national screening programs targeting conditions like HIV, Hepatitis, and antimicrobial resistance ensure a steady pipeline of support. The primary driving factors include a rising prevalence of chronic and infectious diseases, an ageing population requiring frequent monitoring, and an increasing consumer preference for the privacy and convenience of at-home testing kits. Combined with a strong healthcare infrastructure and favourable reimbursement policies, these elements propel the market toward increased accessibility and technological sophistication, solidifying rapid testing as a cornerstone of modern North American healthcare delivery.

Report Coverage

This research report categorises the North America rapid tests market based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the North America rapid tests market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the North America rapid tests market.

North America Rapid Tests Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 710.3 Million |

| Forecast Period: | 2024-2035 |

| Forecast Period CAGR 2024-2035 : | CAGR of 7.07% |

| 2035 Value Projection: | USD 1510.5 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 105 |

| Segments covered: | By Product, By Technology |

| Companies covered:: | Abbott Laboratories, Roche Diagnostics, Cepheid, Becton, Dickinson and Company, Quidel Ortho Corporation, Thermo Fisher Scientific, Bio-Rad Laboratories, Hologic, BioMerieux, Meridian Biosciences, Chembio Diagnostics, Access Bio, Others, and |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The North America rapid tests market is driven by factors such as an ageing population with a high prevalence of chronic conditions, such as diabetes and cardiovascular diseases, necessitates frequent, real-time monitoring. The consumerization of medicine is also a significant driver, as tech-savvy patients increasingly adopt at-home diagnostic kits for everything from infectious diseases to hormone tracking. Technological synergy is further accelerating this growth, with microfluidics and AI-driven smartphone integration transforming simple assays into sophisticated diagnostic tools. From a regulatory standpoint, the expansion of CLIA waivers and supportive FDA pathways has lowered market entry barriers, encouraging a surge in private investment. Additionally, the legacy of recent global health crises has permanently altered public health protocols, making rapid multiplex screening for respiratory pathogens a standard clinical expectation.

Restraining Factors

The North America rapid tests market is constrained by factors such as the stringent regulatory environment; the FDA’s rigorous approval processes for next-generation molecular assays can lead to prolonged development timelines and high entry costs. Furthermore, persistent concerns regarding the diagnostic accuracy and sensitivity of rapid kits, specifically the risk of false results compared to laboratory PCR tests, hinder widespread clinical adoption for critical conditions.

Market Segmentation

The North America rapid tests market share is classified into product, technology, and end user.

- The consumables segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The North America rapid tests market is segmented by product into instruments, consumables, and others. Among these, the consumables segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period. This is due to the recurring necessity of test kits, reagents, and strips across both professional and home settings. diagnostic instruments, which are one-time capital investments, and consumables are high-volume, single-use items that generate a continuous revenue stream, particularly as testing frequencies for chronic and infectious diseases rise.

- The immunoassay segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period.

Based on technology, the North America rapid tests market is segmented into molecular diagnostics, immunoassay, and others. Among these, the immunoassay segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Because of cost-effectiveness, established regulatory tracks, and the lack of complex infrastructure required for operation, the immunoassay is the preferred choice for everything from pregnancy tests to rapid antigen screening.

- The hospitals and clinics segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The North America rapid tests market is segmented by end user into hospitals and clinics, laboratories and others. Among these, the hospitals and clinics segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period. Because of the sheer volume of patients requiring immediate bedside diagnostics to inform urgent clinical decisions, and the integration of rapid testing into standard emergency and outpatient protocols across North American healthcare networks.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the North America rapid tests market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Abbott Laboratories

- Roche Diagnostics

- Cepheid

- Becton, Dickinson and Company

- Quidel Ortho Corporation

- Thermo Fisher Scientific

- Bio-Rad Laboratories

- Hologic

- BioMerieux

- Meridian Biosciences

- Chembio Diagnostics

- Access Bio

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments:

- In September 2025, Quidel Ortho’s Launched the QUICKVUE Influenza + SARS Test. This lateral-flow test provides results in 10 minutes.

- In July 2025, Bio-Rad completed the acquisition of Stilla Technologies to strengthen Bio-Rad’s intellectual property in rapid molecular detection.

- In January 2025, Hologic finalised its acquisition of Gynesonics, a medical device company focused on minimally invasive treatments for women’s health, further diversifying its rapid diagnostic and surgical portfolio.

Market Segment

This study forecasts revenue at the North America, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the North America rapid tests market based on the below-mentioned segments:

North America Rapid Tests Market, By Product

- Instruments

- Consumables

North America Rapid Tests Market, By Technology

- Molecular Diagnostics

- Immunoassay

- Others

North America Rapid Tests Market, By End User

- Hospitals and Clinics

- Laboratories

- At Home Testing

- Others

Frequently Asked Questions (FAQ)

-

Q What is the projected market size and growth rate for the North America rapid tests market?A. The market is expected to grow from USD 710.3 million in 2024 to approximately USD 1,510.5 million by 2035. This represents a steady Compound Annual Growth Rate (CAGR) of 7.07% during the forecast period of 2025–2035.

-

Q. Which product segment holds the largest share in the market?A. The Consumables segment accounted for the largest revenue share in 2024. This dominance is driven by the recurring need for single-use items such as test kits, reagents, and strips, which generate a continuous revenue stream compared to the one-time capital investment required for instruments.

-

Q. What are the primary factors driving market growth in North America?A. Several key factors are propelling the market forward: • Demographics: An ageing population requiring frequent monitoring for chronic conditions like diabetes and cardiovascular diseases. • Technological Innovation: Integration of IoT and AI into diagnostic devices, along with microfluidic "lab-on-a-chip" platforms. • Consumer Trends: A rising preference for the privacy and convenience of at-home testing kits. • Government Support: Funding from agencies like BARDA and streamlined FDA regulatory pathways for faster approvals.

-

Q. Which technology is currently dominating the North American landscape?A. Immunoassay technology is the dominant segment. It is widely preferred due to its cost-effectiveness, established regulatory history, and the minimal infrastructure required for operation, making it ideal for both clinical and home-based applications.

-

Q. Who are the leading end-users of rapid tests in this region?A. The Hospitals and Clinics segment remains the primary end-user. This is attributed to the high volume of patients requiring immediate results for urgent clinical decisions and the integration of rapid diagnostics into standard emergency and outpatient care protocols.

-

Q. What are the main challenges or restraints facing the market?A. Growth is primarily hindered by: • Stringent Regulations: Rigorous FDA approval processes can lead to high development costs and longer timelines. • Accuracy Concerns: Potential issues regarding the sensitivity and specificity of rapid tests—specifically the risk of false results compared to gold-standard PCR lab tests—can slow down clinical adoption.

Need help to buy this report?