North America Preclinical in vivo Imaging Market, Share, and COVID-19 Impact Analysis, By Modality (Optical Imaging, Nuclear Imaging, Micro-MRI, Micro CT, Micro-Ultrasound, Photo acoustic, Magnetic Particle Imaging Systems), By Reagent Type (Optical Imaging Reagents, Nuclear Imaging Reagents, MRI Contrast Agents, Ultrasound Contrast Agents, CT Contrast Agents ), By End Use (Pharma and Biotech Companies, Contract Research Organizations, and Others), and North America Preclinical In vivo Imaging Market Insights, Industry Trend, Forecasts to 2035

Industry: HealthcareNorth America in vivo Imaging Market Insights Forecasts to 2035

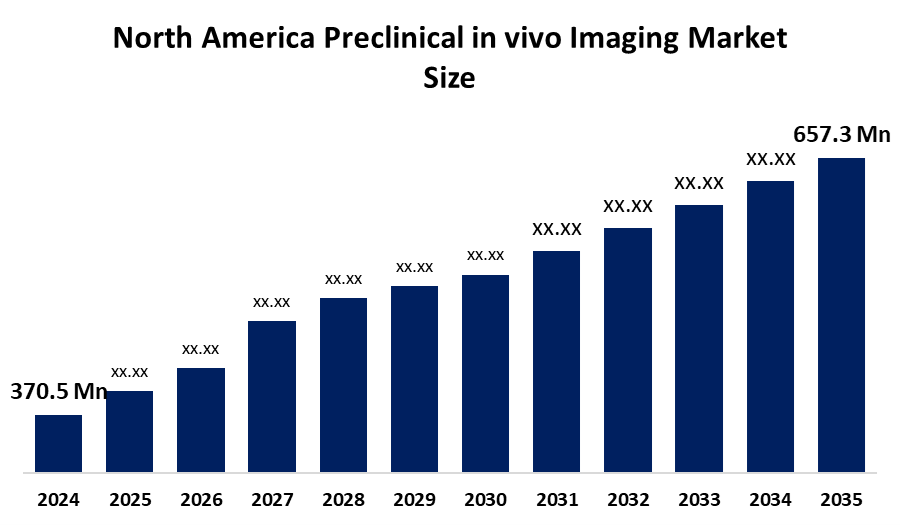

- The North America Preclinical in Vivo Imaging Market Size Was Estimated at USD 370.5Million in 2024

- The Market Size is Expected to Grow at a CAGR of Around 5.62% from 2025 to 2035

- The North America Preclinical in vivo Imaging Market Size is Expected to Reach USD 675.3 Million by 2035

Get more details on this report -

According to a research report published by Spherical Insights & Consulting, the North America preclinical in vivo Imaging market size is anticipated to reach USD 675.3 million by 2035, growing at a CAGR of 5.62% from 2025 to 2035. The in vivo Imaging market in North America is driven by increased innovation in drug discovery with the adoption of AI, development of novel antiviral compounds and favourable government policies to inhibit the disease.

Market Overview

The North American preclinical in vivo imaging market is referred to a powerhouse of biomedical research, defined by the non-invasive visualization and monitoring of biological processes within living animal models to bridge the gap between laboratory discovery and clinical application. This sector is currently defined by high-speed innovations, particularly the integration of artificial intelligence (AI) for automated image quantification and the rise of multimodal systems (like PET/MRI and SPECT/CT) that offer simultaneous functional and anatomical data.

The market is strongly supported by government, with agencies like the National Institutes of Health (NIH) and the Canadian Institutes of Health Research (CIHR) providing massive R&D grants. Programs such as the Small Business Innovation Research (SBIR) also provide critical funding to startups, ensuring a steady pipeline of new tech. The primary driving factors include a rising prevalence of chronic diseases such as cancer and neurodegenerative disorders which demand more sophisticated drug testing. Furthermore, a growing emphasis on longitudinal studies (observing the same subject over time) is pushing labs to replace traditional, invasive methods with high-resolution in vivo imaging to improve data accuracy and meet ethical animal welfare standards.

Report Coverage

This research report categorizes the North America preclinical in vivo imaging market based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the North America market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the North America in vivo preclinical imaging market.

North America Preclinical in vivo Imaging Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 370.5 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 5.62% |

| 2035 Value Projection: | USD 675.3 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 215 |

| Tables, Charts & Figures: | 116 |

| Segments covered: | By Modality, By End Use |

| Companies covered:: | Bruker Corporation, Revvity, Fujifilm Visual Sonics, Siemens Healthineers, Mediso Ltd, MILabs, MR Solutions, Spectral Imaging, Trifoil Imaging, Aspect Imaging, Cubresa, Li-Cor Biosciences, Thermo Fisher Scientific, Lantheus Holdings, Agilent Technologies, Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The North American preclinical in vivo imaging sector is driven by a convergence of technological maturity and shifting R&D paradigms. A primary catalyst is the region’s aggressive pharmaceutical pipeline, where the imperative to reduce drug attrition rates has made high-resolution longitudinal monitoring a necessity rather than a luxury. By allowing researchers to observe biological responses within the same living subject over extended periods, these systems align with the 3Rs of animal welfare reducing the total number of subjects while enhancing data statistical power. Furthermore, the integration of artificial intelligence and machine learning into imaging software has revolutionized data throughput, enabling the rapid quantification of complex biomarkers that were previously labour-intensive to analyse. This is strengthened by a robust influx of federal funding and private equity aimed at tackling the rising burden of age-related chronic conditions, such as Alzheimer's and various metastatic cancers.

Restraining Factors

The North America preclinical in vivo imaging market is constrained by factors such as massive capital expenditure required for high-end multimodal systems, which often exceeds the financial reach of smaller academic labs and emerging start-ups. Beyond the initial purchase, these facilities face exorbitant recurring expenses for specialized maintenance and the handling of sensitive reagents. Furthermore, the market contends with an intensifying regulatory landscape; stringent ethical standards and animal rights advocacy are increasingly pushing researchers toward alternative in vitro models,

Market Segmentation

The North America preclinical in vivo imaging market share is classified into modality, reagents, and end user

- The optical imaging segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The North America preclinical in vivo market is segmented by modality into optical imaging, nuclear imaging, micro-MRI, micro-CT, micro-ultrasound, photo acoustic, magnetic particle imaging systems. Among these, the optical imaging segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period. Because the optical systems are significantly cheaper to purchase and maintain than nuclear or magnetic resonance system, they are the most frequently used for cancer research, allowing scientists to track tumour growth and gene expression in real-time across dozens of subjects simultaneously, and optical Imaging does not require the handling of radioactive isotopes or the heavy shielding infrastructure, making it more accessible to a wider range of laboratories.

- The optical imaging reagent segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period.

Based on reagent type, the North America preclinical in vivo market is segmented into optical imaging reagents, nuclear imaging reagents, MRI contrast agents, ultrasound contrast agents, CT contrast agents. Among these, the optical imaging reagent segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Optical imaging reagent is the most widely used due to its cost-effectiveness. Consequently, the volume of reagents used such as bioluminescent reporters for cancer tracking is significantly higher than that of specialized radioactive tracers. optical dyes and luciferins are non-radioactive, have a long shelf life, and do not require on-site cyclotrons or specialized lead-shielding infrastructure, making them the default choice for academic and small-to-midsize biotech labs.

- The pharma and biotech segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The North America preclinical in vivo market is segmented by end user into pharma and biotech companies, contract research organizations, and others. Among these, the pharma and biotech segment accounted for the largest revenue market share in 2024 and is expected to grow at a significant CAGR during the forecast period. Because large pharmaceutical and biotechnology companies have the capital to invest in multi-modal systems (e.g., PET-CT) to ensure their drug candidates are safe before entering human trials.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the North America preclinical in vivo market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Bruker Corporation

- Revvity

- Fujifilm Visual Sonics

- Siemens Healthineers

- Mediso Ltd

- MILabs

- MR Solutions

- Spectral Imaging

- Trifoil Imaging

- Aspect Imaging

- Cubresa

- Li-Cor Biosciences

- Thermo Fisher Scientific

- Lantheus Holdings

- Agilent Technologies

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the North America, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the North America preclinical in vivo imaging market based on the below-mentioned segments:

North America Preclinical in Vivo Imaging Market, By Modality

- Optical Imaging

- Nuclear Imaging

- Micro-MRI

- Micro CT

- Micro-Ultrasound

- Photo acoustic

- Magnetic Particle Imaging Systems

North America Preclinical in Vivo Imaging Market, By Reagent Type

- Optical Imaging Reagents

- Nuclear Imaging Reagents

- MRI Contrast Agents

- Ultrasound Contrast Agents

- CT Contrast Agents

North America Preclinical in Vivo Imaging Market, End User

- Pharma and biotech companies

- Contract research organisations

- Others

Frequently Asked Questions (FAQ)

-

Q1: What is the projected market size and growth rate for the North America preclinical in vivo imaging market?A: The market size was estimated at USD 370.5 million in 2024 and is projected to reach USD 675.3 million by 2035. This represents a compound annual growth rate (CAGR) of 5.62% during the forecast period from 2025 to 2035.

-

Q2: Which modality segment currently dominates the North American market?A: The Optical Imaging segment accounted for the largest revenue share in 2024. Its dominance is driven by its cost-effectiveness, ease of maintenance compared to nuclear or MRI systems, and its ability to perform high-throughput screening for tumour growth and gene expression without the need for radioactive isotopes.

-

Q3: Why is the Optical Imaging Reagents segment leading the market by reagent type?A: This segment dominates because optical reagents (like bioluminescent reporters) are used in high volumes, particularly in oncology research. They are preferred by academic and mid-size labs because they have a long shelf life, are non-radioactive, and do not require expensive shielding or on-site cyclotrons.

-

Q4: Who are the primary end users of preclinical in vivo imaging systems in North America?A: The Pharma and Biotechnology Companies segment holds the largest market share. These entities have the necessary capital to invest in advanced multimodal systems (such as PET-CT) to ensure drug safety and efficacy before moving into human clinical trials.

Need help to buy this report?