North America Ligation Devices Market Size, Share, and COVID-19 Impact Analysis, By Product Type (Endoscopic Band Ligation Systems, Ligation Clips and Clip Appliers, Ligating Loops and Snares, Accessories & Procedure Kits, and Others), By Application (Gastroenterology & Colorectal, General & Laparoscopic Surgery, Gynecology, Urology, and Others), and North America Ligation Devices Market Insights, Industry Trend, Forecasts to 2035

Industry: HealthcareNorth America Ligation Devices Market Insights Forecasts to 2035

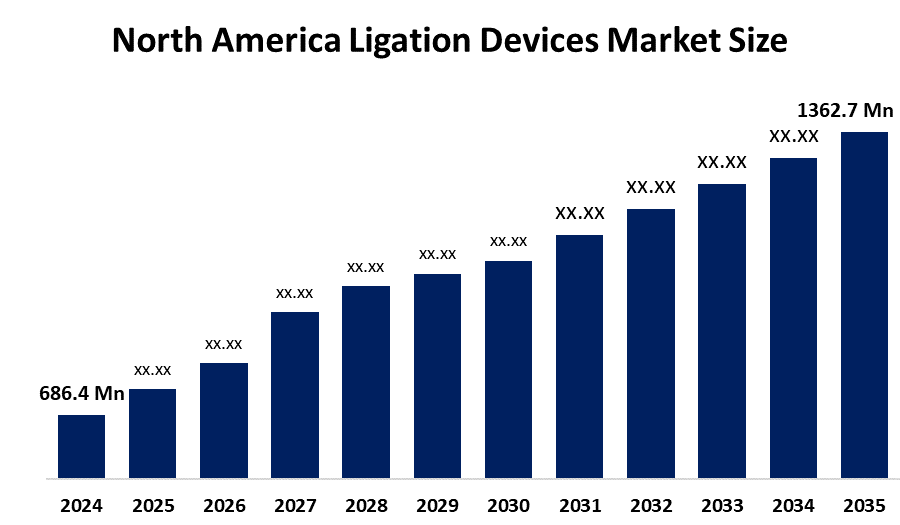

- The North America Ligation Devices Market Size Was Estimated at USD 686.4 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 6.43% from 2025 to 2035

- The North America Ligation Devices Market Size is Expected to Reach USD 1,362.7 Million by 2035

Get more details on this report -

According to a Research Report Published by Spherical Insights & Consulting, the North America Ligation Devices Market is anticipated to reach USD 1,362.7 million by 2035, growing at a CAGR of 6.43% from 2025 to 2035. The primary drivers of the market are the rise in minimally invasive surgeries, the growth of outpatient/day-care procedures, technological advancements in ligation tools, and the increasing demand for single-use consumables

Market Overview

The North American ligation devices market is a healthcare industry segment that provides surgical equipment and consumables used to tie off or seal blood arteries, ducts, or tissues during surgeries to control bleeding or shut structures. It includes goods like clip appliers, ligating clips, endoscopic band ligators, and loops, which are commonly used in gynecological, cardiothoracic, gastrointestinal, urology, and general surgery. Moreover, Ligation devices allow for the controlled occlusion of arteries, ducts, and tissue pedicles during surgical and endoscopic procedures, resulting in hemostasis and secure anatomy. Endoscopic band ligators, mechanical clips and appliers (through and above the scope), ligating loops and snares, and adjunctive equipment and kits are among the product families. Surgeons in North America assess jaw geometry, closing force, clip memory, rotational precision, and compatibility with conventional scopes and trocars. Infection-control policy, reprocessing cost, per-case economics, and the availability of sizes for different tissue thicknesses are additional important decision factors. As physicians strive to improve operating room efficiency and safety, ergonomic devices and durable consumables become important to achieving consistent results. In addition, with advanced healthcare infrastructure, high surgical volumes, and growing adoption of minimally invasive techniques, North America holds the largest global share, making it a key driver of innovation and revenue in this field.

In July 2025, Johnson & Johnson completed the acquisition of a smaller US-based company specializing in biodegradable ligation devices, within the report's prediction period. This decision demonstrates the company's strategic commitment to promoting sustainable and eco-friendly surgical technology, bolstering its market position through investing in novel solutions that correspond with rising environmental concerns.

Report Coverage

This research report categorises the market for the North America ligation devices market based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the North America ligation devices market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the North America ligation devices market.

North America Ligation Devices Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 686.4 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 6.43% |

| 2035 Value Projection: | USD 1,362.7 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 230 |

| Tables, Charts & Figures: | 120 |

| Segments covered: | By Product Type, By Application |

| Companies covered:: | Capsa Healthcare, GCX Corporation (includes JACO), Ergotron, Midmark Corporation, Harloff Manufacturing, ITD GmbH, AFC Industries, Enovate Medical, and Other Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The North American ligation devices market is driven by a number of linked variables, including a consistent increase in surgical procedures across specialties such as gynecology, cardiothoracic, gastrointestinal, and urology, which has helped the region acquire 42.9% of the global share by 2024. The growing desire for minimally invasive techniques such as laparoscopic and endoscopic surgeries, which are prized for their faster recovery and lower costs, has increased demand for advanced instruments such as band ligators, clips, and vessel-sealing devices. In addition, Technological advancements, particularly integrated clip systems that provide more precision and efficiency, as well as the widespread use of disposable devices to reduce infection concerns, have boosted market growth and income potential.

Restraining Factors

The North America ligation devices market faces restraints such as high device costs, strict regulatory requirements, limited adoption in smaller facilities, competition from alternative surgical techniques, and risks associated with device malfunctions or recalls.

Market segmentation

The North America ligation devices market share is classified into product type and application.

- The endoscopic band ligation systems segment held a substantial share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period.

The North America ligation devices market is divided by product type into endoscopic band ligation systems, ligation clips and clip appliers, ligating loops and snares, accessories & procedure kits, and others. Among these, the endoscopic band ligation systems segment held a substantial share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The segment is widely used in gastrointestinal procedures. Their dominance stems from the significant occurrence of conditions such as polyps, hemorrhoids, and varices, where these devices are considered the standard treatment approach, ensuring consistent demand and clinical reliance.

- The gastroenterology & colorectal segment dominated the market in 2024 and is anticipated to grow at a substantial CAGR over the forecast period.

The North America ligation devices market is segmented by application into gastroenterology & colorectal, general & laparoscopic surgery, gynecology, urology, and others. Among these, the gastroenterology & colorectal segment dominated the market in 2024 and is anticipated to grow at a substantial CAGR over the forecast period. This is the dominant segment, driven by accounting for roughly 30% of revenue in 2024. This dominance is fueled by the widespread occurrence of gastrointestinal conditions such as polyps, colorectal cancer, and hemorrhoids. The segment’s growth is further supported by the extensive use of endoscopic band ligators, loops, and clips, which are essential tools in performing minimally invasive procedures.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within North America ligation devices market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Capsa Healthcare

- GCX Corporation (includes JACO)

- Ergotron

- Midmark Corporation

- Harloff Manufacturing

- ITD GmbH

- AFC Industries

- Enovate Medical

- Others

Recent Developments:

- In June 2025, Johnson & Johnson’s Ethicon division has introduced the ETHICON™ 4000 Stapler, featuring proprietary 3D Stapling Technology designed to improve staple line integrity, reduce leaks and bleeding, and enhance surgical precision. Alongside this launch, Ethicon is also exploring biodegradable options, signaling a move toward more sustainable surgical solutions

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at North America, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the North America ligation devices market based on the below-mentioned segments:

North America Ligation Devices Market, By Product Type

- Endoscopic Band Ligation Systems

- Ligation Clips and Clip Appliers

- Ligating Loops and Snares

- Accessories & Procedure Kits

- Others

North America Ligation Devices Market, By Application

- Gastroenterology & Colorectal

- General & Laparoscopic Surgery

- Gynecology

- Urology

- Others

Frequently Asked Questions (FAQ)

-

Q: What is the current and forecasted size of the North America ligation devices market?A: The market was valued at approximately USD 686.4 million in 2024 and is projected to grow at a CAGR of 6.43%, reaching around USD 1,362.7 million by 2035.

-

Q: What are the primary product types in the North America ligation devices market?A: The primary product types are endoscopic band ligation systems, ligation clips and clip appliers, ligating loops and snares, accessories & procedure kits, and others. Among these, the endoscopic band ligation systems segment held a substantial share in 2024. The segment is driven by widely used in gastrointestinal procedures.

-

Q: What is the main application type in the market?A: The main application type is gastroenterology & colorectal, general & laparoscopic surgery, gynecology, urology, and others. Among these, the gastroenterology & colorectal segment dominated the market in 2024. This is the dominant segment driven by accounting for roughly 30% of revenue in 2024. This dominance is fueled by the widespread occurrence of gastrointestinal conditions such as polyps, colorectal cancer, and hemorrhoids.

-

Q: What are the key driving factors for market growth?A: Growth is driven by the rise in minimally invasive surgeries, the growth of outpatient/day-care procedures, technological advancements in ligation tools, and the increasing demand for single-use consumables.

-

Q: What challenges does the market face?A: Challenges include high device costs, strict regulatory requirements, limited adoption in smaller facilities, competition from alternative surgical techniques, and risks associated with device malfunctions or recalls.

-

Q: Who are some key players in the market?A: Key companies include Capsa Healthcare, GCX Corporation (includes JACO), Ergotron, Midmark Corporation, Harloff Manufacturing, ITD GmbH, AFC Industries, Enovate Medical, Others.

Need help to buy this report?