North America Branded Generics Market Size, Share, and COVID-19 Impact Analysis, By Application (Cardiovascular Diseases, Pain Management and Anti-inflammatory, Oncology, Diabetes, Neurology, Gastrointestinal Diseases, Dermatology, and Others), By Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Direct Tenders, and Others), and North America Branded Generics Market Insights, Industry Trend, Forecasts to 2035

Industry: HealthcareNorth America Branded Generics Market Insights Forecasts to 2035

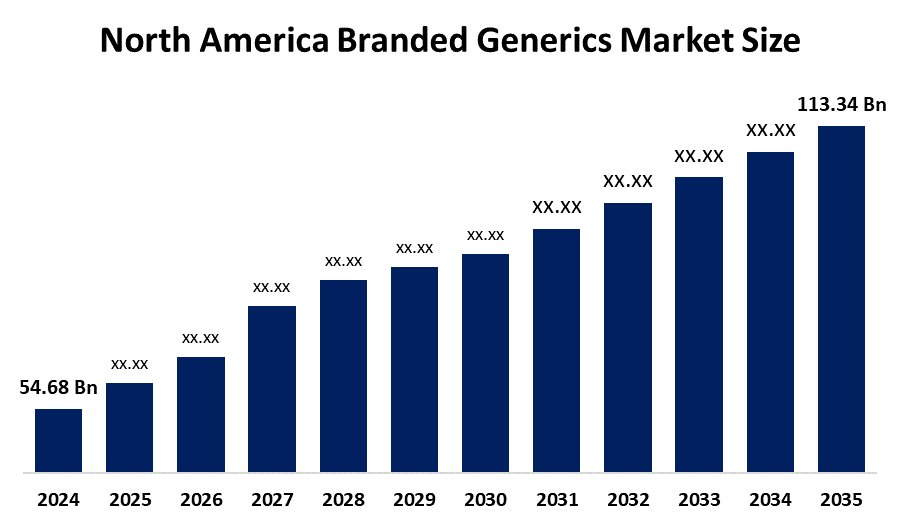

- The North America Branded Generics Market Size Was Estimated at USD 54.68 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 6.85% from 2025 to 2035

- The North America Branded Generics Market Size is Expected to Reach USD 113.34 Billion by 2035

Get more details on this report -

According to a Research Report Published by Spherical Insights & Consulting, The North America Branded Generics Market Size is Anticipated to Aeach USD 113.34 Billion by 2035, Growing at a CAGR of 6.85% from 2025 to 2035. The primary drivers of the market are rising chronic disease prevalence, cost-effective drug demand, patent expirations of blockbuster drugs, government initiatives to reduce healthcare costs, and strong distribution networks across hospitals and pharmacies.

Market Overview

The North American branded generics industry integrates the affordability of generic pharmaceuticals with the trust and recognition of branded products. These medicines are bioequivalent to innovator treatments but differentiated through branding efforts, making them appealing for patients, healthcare providers, and insurers seeking cost-effective and trusted solutions. Furthermore, spans therapeutic areas such as oncology, cardiovascular diseases, diabetes, neurology, and dermatology, with distribution via hospitals, retail pharmacies, online platforms, and drug stores, supported by patent expirations, rising chronic disease prevalence, and government initiatives to reduce healthcare costs. Moreover, North America follows, owing to increased demand for chronic disease medicines, expanded healthcare coverage, and robust distribution networks. Europe is experiencing sustained expansion, aided by generic medicine substitution rules, cost-cutting measures, and an increasing emphasis on healthcare efficiency. Emerging markets in Latin America, the Middle East, and Africa are gradually adopting due to improved healthcare infrastructure, increased regulatory harmonization, and expanded pharmaceutical production capabilities. In addition, Governments and healthcare payers are strongly advocating the use of branded generics through policies, reimbursement structures, and generic replacement programs in order to reduce healthcare costs, increase access to treatment, and enhance patient compliance. These metrics are increasing market usage across numerous therapeutic domains, including cardiovascular, diabetes, cancer, and central nervous system illnesses.

Viatris' August 2025 FDA clearance marks a significant milestone for branded generics in North America, since it introduces the first generic version of Iron Sucrose Injection. This advancement focuses on iron deficiency anemia in patients with chronic kidney disease, making intravenous iron therapy more inexpensive.

Report Coverage

This research report categorises the market for the North America Branded Generics Market Size based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the North America branded generics market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the North America branded generics market.

North America Branded Generics Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 54.68 Billion |

| Forecast Period: | 2024-2035 |

| Forecast Period CAGR 2024-2035 : | CAGR of 6.85% |

| 2035 Value Projection: | USD 113.34 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 140 |

| Tables, Charts & Figures: | 108 |

| Segments covered: | By Application, By Distribution Channel |

| Companies covered:: | Viatris, Teva Pharmaceuticals, Sun Pharmaceutical Industries, Sandoz (Novartis spin off), Apotex Inc., Lupin Pharmaceuticals, Dr. Reddy’s Laboratories,and Other Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The North America Branded Generics Market Size is driven by a number of causes, including the expiration of major medication patents, an increase in chronic conditions such as diabetes, cardiovascular disease, and cancer, and growing demand to cut healthcare costs. Governments and insurers promote the use of branded generics because they combine affordability and brand awareness, while strong distribution networks via hospitals, pharmacies, and online platforms ensure widespread availability. Branded generics play an important role in the region's pharmaceutical landscape, providing cost-effective treatment and driving market growth. Over the last decade, the wave of lost exclusivity across big medicines has produced periodic windows of opportunity for generic competitors and new entrants, changing pricing dynamics, increasing integration in generics manufacturing, and speeding geographic development into emerging markets. Indeed, the size of earnings at stake from expired patents is frequently the economic basis for investing in expensive generics and biosimilars.

Restraining Factors

The North America branded generics market faces key restraints such as intense price competition, regulatory complexities, supply chain challenges, brand loyalty to innovator drugs, and quality concerns from global manufacturing hubs.

Market segmentation

The North America Branded Generics Market share is classified into application and distribution channel.

- The cardiovascular diseases segment held a substantial share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period.

The North America Branded Generics Market Size is divided by application into cardiovascular diseases, pain management, anti-inflammatory, oncology, diabetes, neurology, gastrointestinal diseases, dermatology, and others. Among these, the cardiovascular diseases segment held a substantial share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The segment is driven by Conditions such as hypertension, coronary artery disease, and heart failure, which are extremely common and necessitate long-term care. The chronic nature of many disorders creates a long-term demand for low-cost pharmaceuticals, making branded generics an appealing alternative for patients and healthcare systems looking for cost-effective therapies while maintaining faith in established brands.

- The retail pharmacies segment dominated the market in 2024 and is anticipated to grow at a substantial CAGR over the forecast period.

The North America Branded Benerics Market Size is segmented by distribution channel into retail pharmacies, hospital pharmacies, direct tenders, and others. Among these, the retail pharmacies segment dominated the market in 2024 and is anticipated to grow at a substantial CAGR over the forecast period. This is the dominant segment because it serves as the most convenient and accessible point of sale for patients, particularly those managing chronic diseases like cardiovascular disease and diabetes. Their ubiquitous presence, longer operation hours, and connection with insurance and reimbursement systems make them the preferred channel for both prescribers and patients, resulting in consistent demand and high prescription volumes when compared to hospital pharmacies or direct tenders.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within North America Branded Generics Market Size, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

-

Viatris

-

Teva Pharmaceuticals

-

Sun Pharmaceutical Industries

-

Sandoz (Novartis spin-off)

-

Apotex Inc.

-

Lupin Limited

-

Dr. Reddy’s Laboratories

-

Others

Recent Developments:

- In August 2025, Teva Pharmaceuticals achieved a major milestone with the FDA approval and U.S. launch of the first-ever generic GLP-1 therapy indicated for weight loss. This generic version of Liraglutide Injection (reference drug: Saxenda) is expected to significantly expand access to obesity treatments by lowering costs in a therapeutic class that has seen explosive demand.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at North America, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the North America branded generics market based on the below-mentioned segments:

North America Branded Generics Market, By Application

- Cardiovascular Diseases

- Pain Management

- Anti-Inflammatory

- Oncology, Diabetes

- Neurology

- Gastrointestinal Diseases

- Dermatology

- Others

North America Branded Generics Market, By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Direct Tenders

- Others

Frequently Asked Questions (FAQ)

-

What is the current and forecasted size of the North America branded generics market?The market was valued at approximately USD 54.68 billion in 2024 and is projected to grow at a CAGR of 6.85%, reaching around USD 113.34 billion by 2035.

-

What are the applications in the North America branded generics market?The primary applications are cardiovascular diseases, pain management, anti-inflammatory, oncology, diabetes, neurology, gastrointestinal diseases, dermatology, and others. Among these, the cardiovascular diseases segment held a substantial share in 2024. The segment is driven by Conditions such as hypertension, coronary artery disease, and heart failure, which are extremely common and necessitate long-term care.

-

What is the main distribution channel in the market?The main distribution channels are retail pharmacies, hospital pharmacies, direct tenders, and others. Among these, the retail pharmacies segment dominated the market in 2024. This is the dominant segment because it serves as the most convenient and accessible point of sale for patients, particularly those managing chronic diseases like cardiovascular disease and diabetes.

-

What are the key driving factors for market growth?Growth is driven by the rising chronic disease prevalence, cost-effective drug demand, patent expirations of blockbuster drugs, government initiatives to reduce healthcare costs, and strong distribution networks across hospitals and pharmacies.

-

What challenges does the market face?Challenges include intense price competition, regulatory complexities, supply chain challenges, brand loyalty to innovator drugs, and quality concerns from global manufacturing hubs.

-

Who are some key players in the market?Key companies include Viatris, Teva Pharmaceuticals, Sun Pharmaceutical Industries, Sandoz (Novartis spin-off), Apotex Inc., Lupin Pharmaceuticals, Dr. Reddy’s Laboratories, Others.

Need help to buy this report?