Middle East & Africa LPG Market Size, Share, and COVID-19 Impact Analysis, By Source (Refinery, Associated Gas, and Non-Associated Gas), By Application (Domestic, Agriculture, Industrial, Transportation, and Chemical), and Middle East & Africa LPG Market Insights, Industry Trends, Forecast to 2035

Industry: Chemicals & MaterialsMiddle East & Africa LPG Market Insights Forecasts to 2035

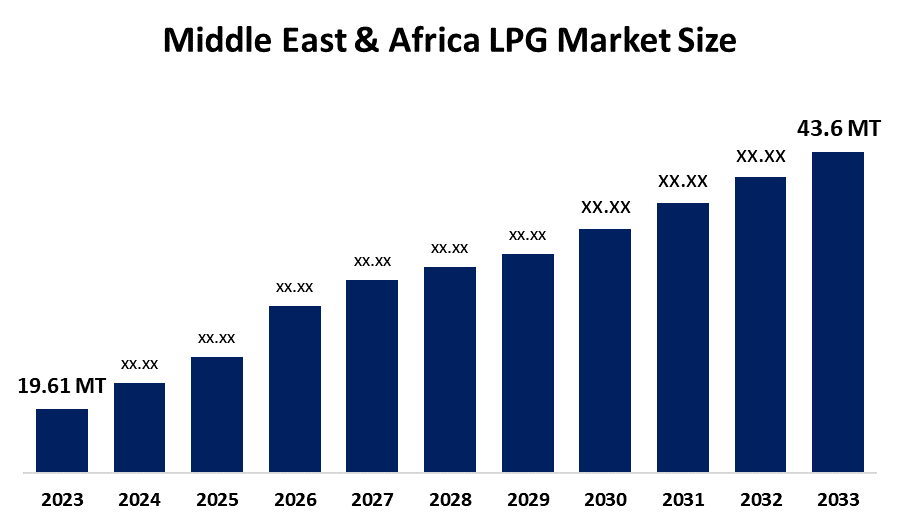

- The Middle East & Africa LPG Market Size Was Estimated at 19.61 Million Tonnes in 2024

- The Market Size is Expected to Grow at a CAGR of Around 7.53% from 2025 to 2035

- The Middle East & Africa LPG Market Size is Expected to Reach 43.6 Million Tonnes by 2035

Get more details on this report -

According to a research report published by Spherical Insights & Consulting, The Middle East & Africa LPG Market Size Is Anticipated To Reach 43.6 Million Tonnes By 2035, Growing At A CAGR Of 7.53% From 2025 To 2035. The market is driven by the growing awareness of environmental issues and the need for sustainable energy solutions. Advancements in technology are enhancing the efficiency of LPG production and distribution, thereby making it more accessible to a broader audience

Market Overview

The LPG Market includes processes that produce, distribute, and consume flammable hydrocarbon gases that exist as propane and butane. The Middle East Gulf area exported liquefied petroleum gas (LPG) at record levels during the second quarter of the year, according to shipping analytics company Vortexa, which showed a 12.9% increase beyond the previous record high. The transition to cleaner energy sources has resulted in greater use of LPG as a suitable replacement for conventional fuels.

B International Shipping & Logistics established a joint venture partnership with Al Seer Marine in June 2025, which they named ASBI Shipping FZCO. Al Seer Marine and B International Shipping & Logistics launched a new JV, securing an AED 660 million LPG charter deal with BGN.

The World Liquid Gas Association (WLGA) aims to expand access to clean cooking solutions for all African countries through its distribution of liquefied petroleum gas (LPG) services. The project has committed $2.2 billion, and $470 million has been allocated to the clean cooking fuel deployment program, which will be spread across 22 African countries.

Report Coverage

This research report categorises the Middle East & Africa LPG market based on various segments and regions, and forecasts revenue growth and analyses trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the Middle East & Africa LPG market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the Middle East & Africa LPG market.

Middle East & Africa LPG Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | 19.61 Million Tonnes |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR Of 7.53% |

| 2035 Value Projection: | 43.6 Million Tonnes |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 90 |

| Segments covered: | By Application , By Source |

| Companies covered:: | Saudi Aramco ADNOC OQ SAOC TotalEnergies SE Shell Plc Kuwait National Petroleum Company ENOC Group AI Fanar Gas Group Benelux Overseas DMCC Others Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The LPG market in Middle East & Africa is driven by the African nations and Middle Eastern governments use LPG subsidies to decrease their dependence on charcoal and wood, which are harmful to the environment. The SADC region uses LPG as its main cooking fuel to replace wood-fired cooking methods. The Middle East industrialization process needs LPG as its essential raw material for producing plastics and polymers because it delivers better operational efficiency and budget-friendly manufacturing methods. The fast expansion of urban populations creates a need for easy-to-use energy sources that people can use for cooking and heating purposes in areas without access to piped natural gas.

Restraining Factors

The LPG market in Middle East & Africa is restrained by the absence of adequate storage facilities and distribution systems, with transportation infrastructure resulting in supply chain interruptions that especially affect remote and rural regions. The developing health and safety issues force companies to spend large amounts of money on cylinder control and leak detection systems, which creates financial challenges for established markets.

Market Segmentation

The Middle East & Africa LPG market share is categorised into source and application.

- The refinery segment accounted for the largest share in 2024 and is expected to grow at a significant CAGR during the forecast period.

The Middle East & Africa LPG Market Size is segmented by source into refinery, associated gas, and non-associated gas. Among these, the refinery segment accounted for the largest share in 2024 and is expected to grow at a significant CAGR during the forecast period. The segmental growth is driven by the established infrastructure of the plant, with its reliable production system. Refinery LPG generally comprises by-products from crude oil processing, making it a reliable source that dominates the market landscape. The system operates because it has strong operational systems that people use in different business areas. The segment achieves advantages through its use of advanced refining technologies which improve production output.

- The domestic segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on application, the Middle East & Africa LPG Market Size is segmented into domestic, agriculture, industrial, transportation, and chemical. Among these, the domestic segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The growth of the segment is driven by the LP gas competing with traditional fuels that use wood, charcoal and coal for their residential needs. The traditional fuels that customers buy in small amounts because they have restricted spending capacity. The section hindrance for introducing LPG to these consumers can be a challenge. The Internet of Things (IoT) creates business models that enable household customers with restricted incomes to purchase their gas needs in small amounts.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Middle East & Africa LPG market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborate analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Saudi Aramco

- ADNOC

- OQ SAOC

- TotalEnergies SE

- Shell Plc

- Kuwait National Petroleum Company

- ENOC Group

- AI Fanar Gas Group

- Benelux Overseas DMCC

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the Middle East & Africa, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Middle East & Africa LPG market based on the below-mentioned segments:

Middle East & Africa LPG Market, By Source

- Refinery

- Associated Gas

- Non-Associated Gas

Middle East & Africa LPG Market, By Application

- Domestic

- Agriculture

- Industrial

- Transportation

- Chemical

Frequently Asked Questions (FAQ)

-

What is the Middle East & Africa LPG market size?The Middle East & Africa LPG market size is expected to grow from 19.61 million tonnes in 2024 to 43.6 million tonnes by 2035, growing at a CAGR of 7.53% during the forecast period 2025-2035

-

What is LPG, and its primary use?LPG is a flammable hydrocarbon gas (mainly propane and butane). It is primarily used for cooking, heating, transportation fuel, and industrial applications

-

What are the key growth drivers of the market?Market growth is driven by the increasing demand for clean energy and government LPG subsidy programs. Rapid urbanization and industrial growth also boost LPG consumption across the region

-

What factors restrain the Middle East & Africa LPG market?The market is restrained by the lack of storage and distribution infrastructure, especially in rural areas. Additionally, high safety costs and transportation challenges impact market growth.

-

What recent developments are influencing the market?Joint ventures like the partnership between Al Seer Marine and logistics firms are expanding LPG shipping capacity. Initiatives by organizations aim to improve clean cooking access across African countries

-

Who are the key players in the Middle East & Africa LPG market?Key companies include Saudi Aramco, ADNOC, and OQ SAOC, TotalEnergies SE, Shell Plc, Kuwait National Petroleum Company, ENOC Group, and AI Fanar Gas Group.

Need help to buy this report?