Global Light Weapons Market Size By Type (Heavy machine guns, MANPAT, Infantry Mortar, Anti-Tank Weapons, Recoilless Rifles, Launchers, Light Cannon, Anti-Tank Missiles, MANPADS, Grenade, Landmines), Guidance (Guided, Unguided), Application (Defense, Homeland Security), By Region, And Segment Forecasts, By Geographic Scope And Forecast to 2033

Industry: Aerospace & DefenseGlobal Light Weapons Market Insights Forecasts to 2033

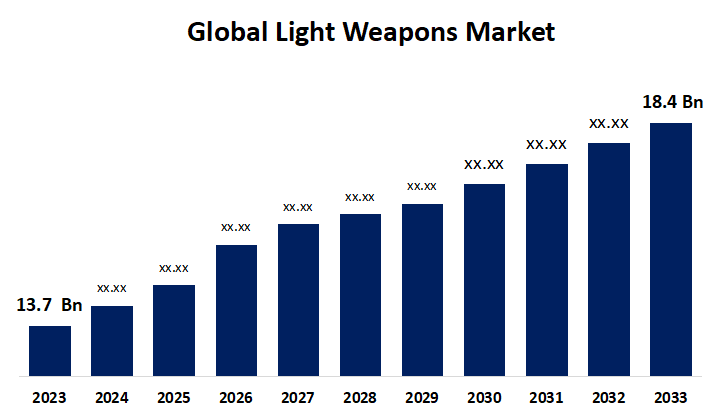

- The Global Light Weapons Market Size was valued at USD 13.7 Billion in 2023.

- The Market Size is Growing at a CAGR of 2.99% from 2023 to 2033

- The Worldwide Light Weapons Market Size is expected to reach USD 18.4 Billion by 2033

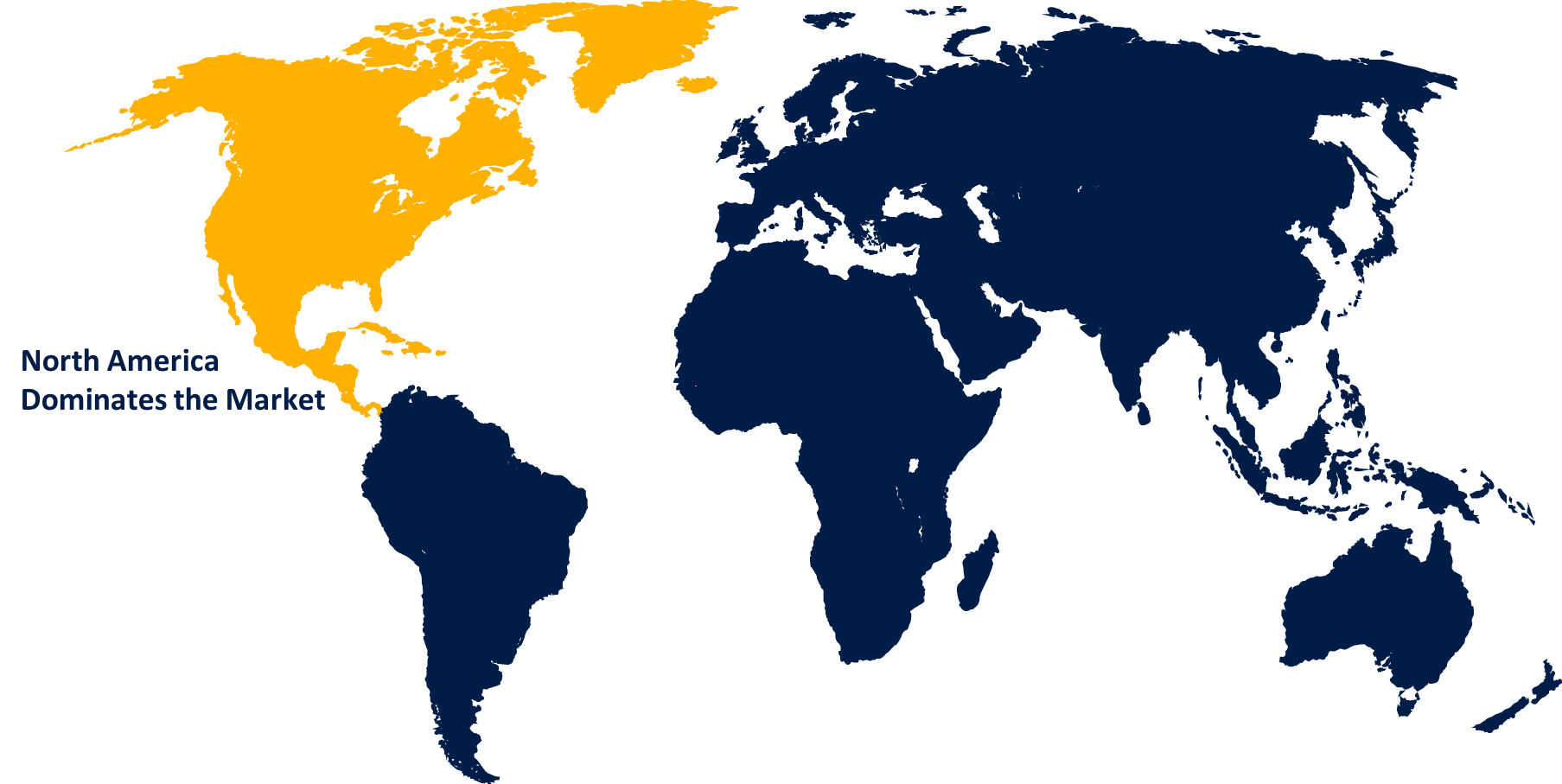

- Asia Pacific is Expected to Grow the fastest during the forecast period

Get more details on this report -

The global Light Weapons Market is expected to reach USD 18.4 billion by 2033, at a CAGR of 2.99% during the forecast period 2023 to 2033.

For a variety of purposes, such as combat operations, homeland security, and law enforcement duties, the military and law enforcement agencies are primary users of light weapons. Growth in the market is frequently driven by demand from these industries, particularly when there are more security threats or armed conflicts. The need for light weapons among civilians is also considerable, especially in areas with a high gun culture or high rates of handgun ownership. Gun ownership among civilians is influenced by a number of factors, including hunting, sport shooting, and self-defense. The GDP growth rate, disposable income levels, and consumer buying habits are examples of economic factors that might affect how affordable and widely available light weapons are. While economic success may spur market expansion, economic downturns may result in lower consumer spending on firearms.

Light Weapons Market Value Chain Analysis

Suppliers supply the raw materials needed to make firearms, including wood, polymers, metals (such as steel and aluminium), and other components. Suppliers supply the raw materials needed to make firearms, including wood, polymers, metals (such as steel and aluminium), and other components. Barrels, triggers, sights, grips, magazines, and other specialty parts and components are supplied by component suppliers and are used in the manufacturing of firearms. These suppliers might be integrated into bigger gun manufacturers or they might be independent companies with a focus on particular parts for firearms. In order to get firearms from manufacturers to dealers, law enforcement, and other final users, distributors are essential. Logistics firms oversee the handling, distribution, and storage of weapons and associated gear, guaranteeing prompt and effective delivery. End users are people who buy and employ light weapons for a variety of objectives, such as law enforcement agencies, military groups, and other entities. Firearms may be needed by end users for military operations, hunting, target practice, self-defense, law enforcement, or collection.

Light Weapons Market Opportunity Analysis

For law enforcement and military applications in particular, smart weapons provide improved security and accountability features. Government organisations may spend money on high-tech weapons to increase worker safety and operational effectiveness. Due to worries about illegal access and gun safety, the civilian sector is seeing an increase in demand for smart weapons. Customers may be ready to pay more for firearms with cutting-edge safety and identification features, especially in areas with tight gun laws. Legislation encouraging or requiring the use of smart gun technology may be introduced in some areas in an effort to reduce gun violence and enhance public safety. Manufacturers of firearms can enter new markets and obtain a competitive edge by creating inventive, legally compatible smart firearms.

Global Light Weapons Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2023 |

| Market Size in 2023: | USD 13.7 billion |

| Forecast Period: | 2023-2033 |

| Forecast Period CAGR 2023-2033 : | 2.99% |

| 2033 Value Projection: | USD 18.4 billion |

| Historical Data for: | 2019-2022 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Type, By Region, By Geographic Scope |

| Companies covered:: | Lockheed Martin, Raytheon, General Dynamics, BAE Systems, Thales Group, Alliant Techsystems, Saab, Rheinmetall, Cockerill Maintenance & Ingenierie, and Heckler & Koch Defense and Other Key Vendors. |

| Pitfalls & Challenges: | COVID-19 Empact,Challenges, Future, Growth, & Analysis |

Get more details on this report -

Market Dynamics

Light Weapons Market Dynamics

Weapons are widely available and reasonably priced, which will fuel market expansion.

Weapons can become more accessible due to their widespread availability and inexpensive cost, especially in areas with loose laws or porous borders. This accessibility may encourage both the growth of firearms and illegal trafficking in addition to law-abiding persons making legitimate purchases. The availability of low-cost firearms can lead to an increase in crime and violence because it can make it simpler for offenders to acquire weapons for crimes like armed robbery, gang violence, and terrorism. Communities and countries may have to deal with serious social, economic, and security ramifications from this. In the market for light weapons, lower entry barriers and more competition could encourage producers to innovate, differentiate their products, and take cost-cutting steps. In this context, businesses who can manufacture firearms of superior quality at competitive rates while adhering to regulatory standards are likely to prosper.

Restraints & Challenges

Manufacturers, governments, and international organisations have ethical concerns about the use of light weapons in armed conflicts and violations of human rights. Businesses that deal with light weapons must follow moral business conduct, uphold human rights standards, and refrain from recklessly transferring or selling weapons to fuel war or cause misery for others. The worldwide reach of the light weapons industry exposes businesses to supply chain risks, such as interruptions in the availability of components, raw materials, and manufacturing capacity. Supply chains can be disrupted by political unrest, natural disasters, trade disputes, and sanctions, which can cause delays, cost overruns, and operational difficulties for industry participants. The market for light weapons is characterised by fierce rivalry among producers and price-sensitive customer demand, which puts pressure on pricing and profit margins.

Regional Forecasts

North America Market Statistics

Get more details on this report -

North America is anticipated to dominate the Light Weapons Market from 2023 to 2033. North America, and especially the United States, have a substantial civilian gun ownership population and a robust weapons culture. The desire for light weapons such as handguns, rifles, and shotguns for activities like self-defense, hunting, target practice, and collecting is fueled by this culture. In order to protect public safety and fight crime, law enforcement agencies in North America are substantial users of light weapons. Weapons including handguns, patrol rifles, and tactical shotguns are frequently purchased by police departments, sheriff's offices, and federal law enforcement agencies. Law enforcement needs specialised weapons and equipment to handle a variety of operational scenarios. This includes less-lethal weapons and tactical accessories.

Asia Pacific Market Statistics

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. To strengthen their defence capacities, a number of Asia-Pacific nations are funding military modernization initiatives. To equip its armed forces, this involves buying light weapons including rifles, machine guns, handguns, and grenade launchers. Expanding defence budgets in nations like Australia, Japan, South Korea, China, India, and South India support the expansion of the light weapons market in the region. Military and paramilitary forces in the Asia-Pacific area are driven to acquire light weapons due to geopolitical tensions, territorial conflicts, and security threats. The need for guns and related equipment is fueled by ongoing hostilities and boundary disputes in places like the Korean Peninsula and the South China Sea.

Segmentation Analysis

Insights by Type

The anti tank weapons segment accounted for the largest market share over the forecast period 2023 to 2033. In order to combat new threats, several nations are investing in modernising their military forces, which includes obtaining cutting-edge anti-tank weapons. In order to neutralise these targets, military vehicles that are armoured more extensively require more powerful anti-tank weapons.The market for anti-tank weapons has surged as a result of growing geopolitical tensions in several countries. Acquiring anti-tank missiles, rockets, and other munitions is one way that nations hoping to protect themselves from non-state actors or neighbouring states try to strengthen their defences. The desire for anti-tank weapons that can successfully resist a wide range of threats, including armoured vehicles, fortifications, and infrastructure targets, has increased due to the emergence of hybrid warfare tactics, which combine conventional and unconventional approaches.

Insights by Guidance

The guided segment accounted for the largest market share over the forecast period 2023 to 2033. Compared to unguided munitions, guided weapons have more accuracy and precision, which makes them extremely effective against particular targets. This capacity to target precisely reduces collateral damage and improves operational effectiveness, especially when interacting with moving or fortified targets or in urban situations. As a component of their efforts to modernise their armed forces, numerous nations are investing in guided weapons systems. Modern guided missiles, rockets, and projectiles are being created or purchased in order to improve military power and preserve a technological advantage over possible enemies. Numerous guided weaponry systems are engineered to possess multiple roles, enabling them to target and destroy a range of targets, such as armoured cars, aeroplanes, ships, and fortified bunkers. Because of their adaptability, guided weapons can be used for a variety of missions and operational settings.

Insights by Application

The defence segment accounted for the largest market share over the forecast period 2023 to 2033. Global military modernization initiatives are being undertaken by numerous nations due to the convergence of geopolitical pressures, emerging technologies, and changing security concerns. Defence forces aim to enhance their armament with cutting-edge light weapons as part of these modernization programmes in order to keep a competitive advantage in combat. Defence personnel involved in counterterrorism operations are requesting more light weapons as a result of the worldwide threat posed by terrorism. Precision strikes on terrorist targets and threat neutralisation in urban areas require specialised weapons, like assault rifles, sniper rifles, and grenade launchers. The creation of light weapons specifically designed for urban combat scenarios has become necessary because to the rising urbanisation of conflict zones.

Recent Market Developments

- In January 2021, Bharat Electronics Limited (BEL) signed an agreement with the Indian Navy to provide light amplification through the stimulation of laser dazzler emission. The company will provide the Navy with 20 laser dazzlers as per the contract.

Competitive Landscape

Major players in the market

- Lockheed Martin

- Raytheon

- General Dynamics

- BAE Systems

- Thales Group

- Alliant Techsystems

- Saab

- Rheinmetall

- Cockerill Maintenance & Ingenierie

- Heckler & Koch Defense

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Light Weapons Market, Type Analysis

- Heavy machine guns

- MANPAT

- Infantry Mortar

- Anti-Tank Weapons

- Recoilless Rifles

- Launchers

- Light Cannon

- Anti-Tank Missiles

- MANPADS

- Grenade

- Landmines

Light Weapons Market, Guidance Analysis

- Guided

- Unguided

Light Weapons Market, Application Analysis

- Defense

- Homeland Security

Light Weapons Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.What is the market size of the Light Weapons Market?The global Light Weapons Market is expected to grow from USD 13.7 billion in 2023 to USD 18.4 billion by 2033, at a CAGR of 2.99% during the forecast period 2023-2033.

-

2. Who are the key market players of the Light Weapons Market?Some of the key market players of the market are Lockheed Martin, Raytheon, General Dynamics, BAE Systems, Thales Group, Alliant Techsystems, Saab, Rheinmetall, Cockerill Maintenance & Ingenierie, Heckler & Koch Defense.

-

3.Which segment holds the largest market share?The guided segment holds the largest market share and is going to continue its dominance.

-

4.Which region is dominating the Light Weapons Market?North America is dominating the Light Weapons Market with the highest market share.

Need help to buy this report?