Japan Viral Vector and Plasmid DNA Manufacturing Market Size, Share, By Vector Type (Adenovirus, Retrovirus, Adeno-associated Virus, Lentivirus, Plasmids, and Others), By Manufacturing Stage (Upstream Processing, Vector Amplification & Expansion, Vector Recovery/Harvesting, Downstream Processing, Purification, and Fill-finish), By Application (Gene Therapy, Cell Therapy, Vaccinology, Antisense & RNAi, and Research Applications), By End Use (Pharmaceutical and Biopharmaceutical Companies and Research Institutes), By Disease (Cancer, Genetic Disorders, Infectious Diseases, and Others), Japan Viral Vector and Plasmid DNA Manufacturing Market Insights, Industry Trend, Forecasts to 2035.

Industry: HealthcareJapan Viral Vector and Plasmid DNA Manufacturing Market Insights Forecasts to 2035

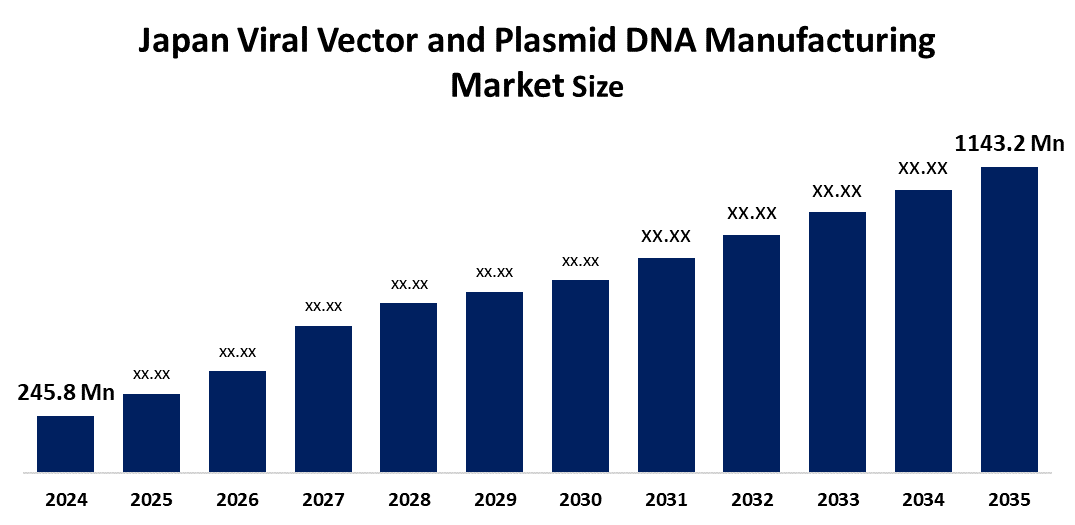

- Japan Viral Vector and Plasmid DNA Manufacturing Market Size 2024: USD 245.8 Mn

- Japan Viral Vector and Plasmid DNA Manufacturing Market Size 2035: USD 1143.2 Mn

- Japan Viral Vector and Plasmid DNA Manufacturing Market CAGR 2024: 15%

- Japan Viral Vector and Plasmid DNA Manufacturing Market Segments: Vector Type, Manufacturing Stage, Application, End Use, and Disease

Get more details on this report -

The Japan market for viral vector and plasmid DNA production operates according to GMP standards to create viral vectors and plasmid DNA which serve as genetic delivery systems for advanced therapeutic applications. The components play an essential role in gene therapy applications and cell therapy treatments and oncological treatments and rare genetic disorder therapies and vaccine development and research purposes. The manufacturing process requires operators to maintain controlled conditions while performing cell culture and vector amplification and purification and sterile fill-finish procedures. The market demonstrates growth because Japan experiences rapid development of gene therapy pipelines and increasing adoption of regenerative medicine products.

Japan depends on imported bioreactor systems which provide high-performance capabilities and chromatography equipment and specialized single-use technologies for its vector production needs. The industry achieves better yield and improved safety and more consistent production through ongoing development of suspension-based cell platforms and high-efficiency transfection methods and closed automated processing systems and advanced purification technologies. The Pharmaceuticals and Medical Devices Act (PMD Act) and regenerative medicine regulations mandate strict GMP standards for advanced therapy manufacturing. The vector manufacturing infrastructure in Japan will experience substantial growth because of increasing funding for oncology gene therapies and development of local CDMO centers and establishment of production capacity for late-stage clinical and commercial operations.

Market Dynamics of the Japan Viral Vector and Plasmid DNA Manufacturing Market:

The Japan viral vector and plasmid DNA manufacturing market is driven by increasing outsourcing of vector production to specialized GMP facilities, rising demand for clinical-grade plasmid backbones for investigational new drug submissions, and higher regulatory scrutiny on vector characterization and quality documentation. Sponsors are prioritizing validated manufacturing platforms to reduce development risk and accelerate clinical progression timelines.

The Japan viral vector and plasmid DNA manufacturing market faces restraints due to long technology transfer timelines between innovators and manufacturers, limited large-scale viral vector production capacity, and high batch failure risks associated with contamination or low transfection efficiency. Complex comparability requirements during process scale-up also increase operational burden and cost exposure.

The Japan viral vector and plasmid DNA manufacturing market presents future opportunities through establishment of modular manufacturing facilities, localization of raw material supply chains, and integration of digital bioprocess monitoring systems for predictive quality control. Expansion of early-phase biotech startups in Japan and government-backed regenerative medicine clusters is expected to stimulate new vector production demand.

Japan Viral Vector and Plasmid DNA Manufacturing Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 245.8 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 15% |

| 2035 Value Projection: | USD 1143.2 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 220 |

| Tables, Charts & Figures: | 89 |

| Segments covered: | By Vector Type, By Manufacturing Stage, By Application, By End Use, By Disease |

| Companies covered:: | FUJIFILM Diosynth Biotechnologies, Takara Bio Inc., Astellas Pharma Inc., AGC Biologics, Lonza Group, Charles River Laboratories, and others. |

| Pitfalls & Challenges: | COVID-19 Impact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Market Segmentation

The Japan viral vector and plasmid DNA manufacturing market share is classified into vector type, manufacturing stage, application, end use, and disease.

By Vector Type:

The Japan viral vector and plasmid DNA manufacturing market is divided by vector type into adenovirus, retrovirus, adeno-associated virus, lentivirus, plasmids, and others. Among these, the adeno-associated virus segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The adeno-associated virus segment dominates due to its strong safety profile, low immunogenicity, stable gene expression capability, broad tissue targeting efficiency, and increasing regulatory approvals of AAV-based gene therapies requiring scalable and high-purity manufacturing capacity.

By Manufacturing Stage:

The Japan viral vector and plasmid DNA manufacturing market is divided by manufacturing stage into upstream processing, vector amplification & expansion, vector recovery/harvesting, downstream processing, purification, and fill-finish. Among these, the upstream processing segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The upstream processing segment dominates due to high resource utilization in cell culture development, transfection optimization, bioreactor scaling, media consumption, and process development activities essential for achieving targeted vector yield and consistency.

By Application:

The Japan viral vector and plasmid DNA manufacturing market is divided by application into gene therapy, cell therapy, vaccinology, antisense & RNAi, and research applications. Among these, the gene therapy segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The gene therapy segment dominates due to expanding clinical pipelines, increasing commercialization of approved therapies, demand for high-titer vector production, long-term genetic correction strategies, and significant investment in rare disease and oncology-focused therapeutic development programs.

By End Use:

The Japan viral vector and plasmid DNA manufacturing market is divided by end use into pharmaceutical and biopharmaceutical companies and research institutes. Among these, the pharmaceutical and biopharmaceutical companies segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The pharmaceutical and biopharmaceutical companies segment dominates due to large-scale commercial manufacturing requirements, in-house GMP facility investments, contract manufacturing partnerships, regulatory submission responsibilities, and increasing biologics and advanced therapy product pipelines.

By Disease:

The Japan viral vector and plasmid DNA manufacturing market is divided by disease into cancer, genetic disorders, infectious diseases, and others. Among these, the cancer segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The cancer segment dominates due to rising oncology gene therapy trials, increasing CAR-T and oncolytic virus development programs, higher funding allocation for cancer innovation, and strong demand for scalable viral vector production to support immuno-oncology therapeutic commercialization.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the Japan viral vector and plasmid DNA manufacturing market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in Japan Viral Vector and Plasmid DNA Manufacturing Market:

- FUJIFILM Diosynth Biotechnologies

- Takara Bio Inc.

- Astellas Pharma Inc.

- AGC Biologics

- Lonza Group

- Charles River Laboratories

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the Japan, regional, and country levels from 2020 to 2035. Decisions Advisors has segmented the Japan viral vector and plasmid DNA manufacturing market based on the below-mentioned segments:

Viral Vector and Plasmid DNA Manufacturing Market, By Vector Type

- Adenovirus

- Retrovirus

- Adeno-associated Virus

- Lentivirus

- Plasmids

- Others

Viral Vector and Plasmid DNA Manufacturing Market, By Manufacturing Stage

- Upstream Processing

- Vector Amplification & Expansion

- Vector Recovery/Harvesting

- Downstream Processing

- Purification

- Fill-finish

Viral Vector and Plasmid DNA Manufacturing Market, By Application

- Gene Therapy

- Cell Therapy

- Vaccinology

- Antisense & RNAi

- Research Applications

Viral Vector and Plasmid DNA Manufacturing Market, By End Use

- Pharmaceutical and Biopharmaceutical Companies

- Research Institutes

Viral Vector and Plasmid DNA Manufacturing Market, By Disease

- Cancer

- Genetic Disorders

- Infectious Diseases

- Others

Frequently Asked Questions (FAQ)

-

What is the Japan viral vector and plasmid DNA manufacturing market size?The market was valued at USD 245.8 million in 2024 and is projected to reach USD 1,143.2 million by 2035, growing at a CAGR of 15% during 2025-2035.

-

What are the key growth drivers of the market?Growth is driven by expanding gene therapy and cell therapy pipelines, rising oncology research, increasing demand for GMP-grade viral vectors and plasmid DNA, and higher outsourcing to specialized CDMOs.

-

What factors restrain the market?Major restraints include limited large-scale production capacity, high manufacturing and compliance costs, complex technology transfer timelines, contamination risks, and stringent regulatory comparability requirements.

-

Who are the key players in the market?Key companies include FUJIFILM Diosynth Biotechnologies, Takara Bio Inc., Astellas Pharma Inc., AGC Biologics, Lonza Group, Charles River Laboratories, and others.

-

Who are the target audiences for this report?Market players, investors, end-users, government authorities, consulting and research firms, venture capitalists, and value-added resellers (VARs).

Need help to buy this report?