Iran Phenol Market Size, Share, By Derivative Type (Bisphenol A, Phenolic Resins, Caprolactum, Alkyl Phenols, And Others), By End Use (Chemicals, Constructions, Automotive, Electronic Communication, Pharmaceuticals, And Others), And Iran Phenol Market Insights, Industry Trend, Forecasts to 2035

Industry: Chemicals & MaterialsIran Phenol Market Insights Size Forecasts to 2035

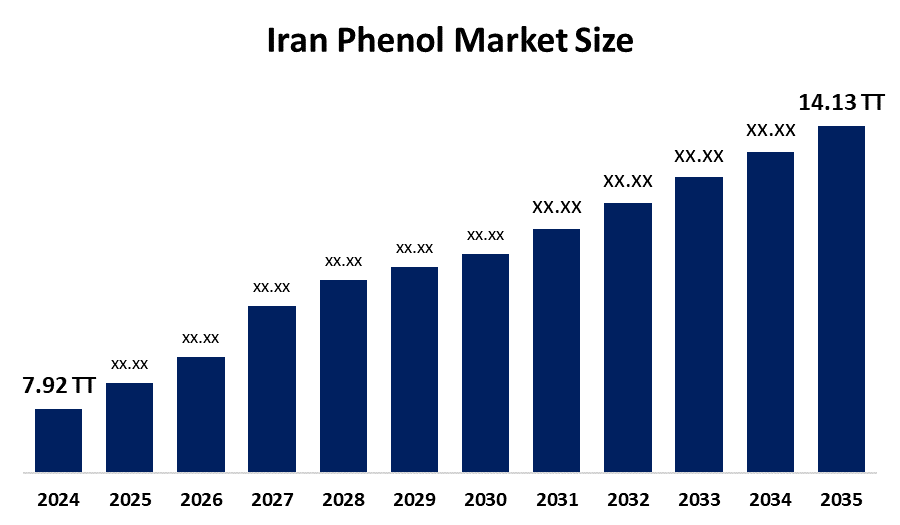

- Iran Phenol Market Size 2024: 7.92 Thousand Tonnes

- Iran Phenol Market Size 2035: 14.13 Thousand Tonnes

- Iran Phenol Market CAGR 2024: 5.4%

- Iran Phenol Market Segments: Derivative Type and End Use

Get more details on this report -

The Iran Phenol Market Size encompasses the various aspects of its production and consumption of phenol and its derivatives. Phenol is an important organic intermediate that serves as the basis for many products that include phenolic resin, bisphenol A, polycarbonate, epoxy resin, pharmaceuticals, agrochemicals and specialty chemicals. The primary source of phenol is through the oxidation of cumene and is used as a key building block for plastics, coatings, adhesives, etc., to produce many of the materials used in industrial production, which add up to an important piece of the overall petrochemical industry in Iran.

The phenol in Iran are backed by government support, including the state-owned National Petrochemical Company (NPC), facilitating stalled petrochemical projects and boosting exports as part of the Seventh National Development Plan. The total petrochemical production capacity reaching nearly 100 million tons per year and exports of petrochemical products valued at around $13 billion, underpinning the demand for aromatic intermediates like phenol and illustrates the importance of the sector to national economic targets.

As technology advances, Iran’s phenol providers are now using large, integrated phenol-acetone plants that combine upstream feedstock production with downstream refining, transportation costs are decreased while yield efficiencies are improved resulting in a more competitive operation compared to stand-alone plants. In addition to these integrated facilities, trends in digital process control, automation, and safety optimization are also being applied more broadly in chemical production hubs to increase environmental compliance and operational reliability. The general trend for chemical companies in Iran is to use these advanced technologies to increase competitiveness and sustainability throughout the industry.

Market Dynamics of the Iran Phenol Market:

The Iran phenol market is driven by the expanding demand for phenol derivatives, growing end user sectors, rise in phenol consumption, domestic industrial capacity building, globalization of Iran’s chemical producers further support market growth, state-led policies to secure supply chains, encourage large-scale refining complexes underpin expansion, and Iran’s expanding export orientation in chemical intermediates has contributed to sustained phenol industry activity and investment.

The Iran phenol market is restrained by the oversupply and weak downstream demand, price depressions and cyclical downturns challenges, weakening effective demand, creating supply-chain feedback that depressed phenol prices, environmental regulation, and raw material price volatility also add cost pressures.

The future of Iran phenol market is bright and promising, with versatile opportunities emerging from the continuous change toward producing higher value derivative and specialized commercial chemicals product use of phenol has an opportunity for value-added growth, particularly in producing advanced resin systems, engineering plastic and high-performance materials. Phenolic resin market expansion as a result of increased global demand for resins used in the renewable energy, electronics and automotive vehicle weight reduction industries create new potential end-use markets. Opportunities also exist for sustainable and bio-based phenol production, which would support Iran’s broader goals around carbon reduction and green industrial development.

Market Segmentation

The Iran phenol market share is classified into derivative type and end use.

By Derivative Type:

The Iran phenol market is divided by derivative type into bisphenol A, phenolic resins, caprolactum, alkyl phenols, and others. Among these, the bisphenol A segment held the largest revenue market share in 2024 and is predicted to grow at a remarkable CAGR during the forecast period. Rapid expansion of downstream industries, global manufacturing hub, demand for high-performance engineering plastics, urbanization, and growing requirement for bisphenol A all contribute to the bisphenol A segment's largest share and higher spending on phenol when compared to other derivative type.

By End Use:

The Iran phenol market is divided by end use into chemicals, construction, automotive, electronic communication, pharmaceuticals, and others. Among these, the chemical segment dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The chemical segment dominates because it is an indispensable raw material for producing high-demand, downstream chemical derivatives, essential for Iran’s massive manufacturing sectors, large scale domestic production and integration, and rapid growth in end use industries in Iran.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the Iran phenol market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in Iran Phenol Market:

- Arak Petrochemical Company

- National Petrochemical Company

- Isfahan Petrochemical Company

- Bandar Imam Petrochemical Co.

- Khuzestan Petrochemical Co.

- Others

Recent Developments in Iran Phenol Market:

- In August 2025, the National Petrochemical Company of Iran announced plans to raise total nominal petrochemical production capacity by late March 2026. The expansion aimed to increase the production of downstream products like Bisphenol A and Phenol-Formaldehyde reins, which are heavily used in the local construction and automotive sectors.

- In March 2025, Iran is actively launching new projects to boost downstream petrochemical products, including phenol derivatives. The focus is on reducing reliance on raw commodity sales and moving towards higher-value products like phenol.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the Iran, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Iran phenol market based on the below-mentioned segments:

Iran Phenol Market, By Derivative Type

- Bisphenol A

- Phenolic Resins

- Caprolactum

- Alkyl Phenols

- Others

Iran Phenol Market, By End Use

- Chemicals

- Construction

- Automotive

- Electronic Communication

- Pharmaceuticals

- Others

Frequently Asked Questions (FAQ)

-

Q: What is the Iran phenol market size?A: Iran phenol market is expected to grow from 7.92 thousand tonnes in 2024 to 14.13 thousand tonnes by 2035, growing at a CAGR of 5.4% during the forecast period 2025-2035.

-

Q: What are the key growth drivers of the market?A: Market growth is driven by the expanding demand for phenol derivatives, growing end user sectors, rise in phenol consumption, domestic industrial capacity building, globalization of Chinese chemical producers further support market growth, state-led policies to secure supply chains, encourage large-scale refining complexes underpin expansion, and Iran’s expanding export orientation in chemical intermediates has contributed to sustained phenol industry activity and investment.

-

Q: What factors restrain the Iran phenol market?A: Constraints include the oversupply and weak downstream demand, price depressions and cyclical downturns challenges, weakening effective demand, creating supply-chain feedback that depressed phenol prices, environmental regulation, and raw material price volatility also add cost pressures.

-

Q: How is the market segmented by derivative type?A: The market is segmented into bisphenol A, phenolic resins, caprolactum, alkyl phenols, and others.

-

Q: Who are the key players in the Iran phenol market?A: Key companies include Arak Petrochemical Company, National Petrochemical Company, Isfahan Petrochemical Company, Bandar Imam Petrochemical Co., Khuzestan Petrochemical Co., and Others.

-

Q: Who are the target audiences for this market report?A: The report targets market players, investors, end-users, government authorities, consulting and research firms, venture capitalists, and value-added resellers (VARs).

Need help to buy this report?