Global In Vitro Diagnostics Market Size, Share, and COVID-19 Impact Analysis, By Test Type (Clinical Chemistry, Molecular Diagnostics, Immunodiagnostics, Hematology, and Others), By Product (Reagents & Kits and Instruments), By End User (Hospital Laboratories, Clinical Laboratories, Point Of Care Testing Centers, Academic Institutes, Patients, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: HealthcareGlobal In Vitro Diagnostics Market Insights Forecasts to 2035

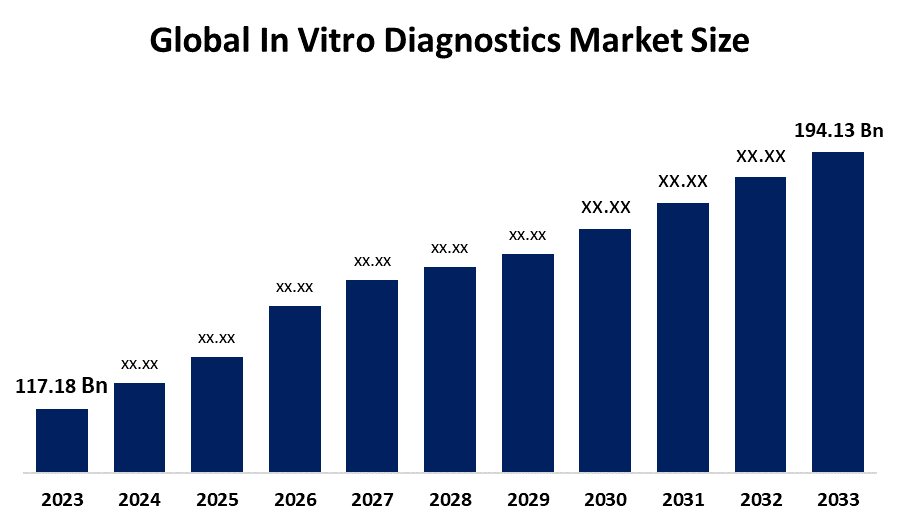

- The Global In Vitro Diagnostics Market Size Was Estimated at USD 117.18 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 4.7% from 2025 to 2035

- The Worldwide In Vitro Diagnostics Market Size is Expected to Reach USD 194.13 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, The Global In-Vitro Diagnostics Market Size Was Worth Around USD 117.18 Billion In 2024 And Is Predicted To Grow To Around USD 194.13 Billion By 2035, With A Compound Annual Growth Rate (CAGR) Of 4.7% From 2025 To 2035. Global advancements in molecular diagnostics, next-generation sequencing, and point-of-care testing, along with AI integration for data analysis, advanced immunoassays, and digital health integration, are driving opportunities in the in-vitro diagnostics market.

Market Overview

The in-vitro diagnostics market is the portion of the global industry that involves companies that develop and manufacture products used to test biological samples outside of the body to help diagnose medical conditions, monitor patient health, or assist in making treatment decisions. These products include high-volume clinical chemistry tests, molecular diagnostic tests, immunoassays, hematology tests, microbiology kits, and point-of-care testing devices. The growth of the IVD market is supported by several factors, including the rising incidence of chronic diseases, the growing need for early disease detection, technological advancements in diagnostic testing products, and the development of emerging markets.

IVD products are regulated by government agencies to ensure they are safe and effective. Many government agencies and organizations reimburse U.S. clinical laboratories for their laboratory-developed tests as a means of supporting laboratories and enhancing public health. In addition, federal and state governments fund laboratory research and invest in new technologies to increase access to diagnostic testing. For example, in February 2025, India’s ABDM initiative to build a national digital health ecosystem with interoperable health records reported more than 73.98 crore ABHA created and over 49.06 crore health records linked, helping integrate lab test data and other diagnostic information digitally, thereby supporting the expansion and accessibility of the in-vitro diagnostics market.

In December 2024, the U.S. NIH allocated approximately 6.581 billion for allergy and infectious disease research funding, supporting the development and deployment of diagnostic test kits and point-of-care tests, which are key components of the in-vitro diagnostics market. The rapid pace of technological advancement remains one of the main drivers of the market’s expansion.

Report Coverage

This research report categorizes the in-vitro diagnostics market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyzes the key growth drivers, opportunities, and challenges influencing the in-vitro diagnostics market. Recent market developments and competitive strategies, such as expansion, product launches, development, partnerships, mergers, and acquisitions, have been included to outline the competitive landscape of the market. The report strategically identifies and profiles the key market players and analyzes their core competencies in each sub-segment of the in-vitro diagnostics market.

Global In Vitro Diagnostics (IVD) Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 117.18 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR Of 4.7% |

| 2035 Value Projection: | USD 194.13 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 90 |

| Segments covered: | By Product Type, By Application |

| Companies covered:: | Roche Diagnostics Abbott Laboratories Danaher Corporation Siemens Healthineers Thermo Fisher Scientific Becton, Dickinson and Company bioMerieux Sysmex QuidelOrtho Bio-Rad Laboratories Illumina Hologic Qiagen DiaSorin Agilent Technologies Others Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

Rapid technological innovation is one of the main drivers of the in-vitro diagnostics market's growth. A rise in both chronic and infectious disease rates creates an immediate demand for reliable and prompt diagnosis, which continues to drive the in-vitro diagnostics market. In addition, innovation and investment in this area are primarily driven by increasing patient awareness of health management, a growing emphasis on disease prevention through early detection, rising healthcare spending, and advancements in technologies such as molecular diagnostics, immunoassays, next-generation sequencing, and POC devices, which are helping broaden and improve testing. Government support also continues to encourage digital health integration, laboratory innovation, and new diagnostic product development.

In June 2023, Japan’s Ministry of Health, Labour and Welfare (MHLW) granted manufacturing and marketing approval for Toray Industries' Toray APOA2-iTQ, an in-vitro diagnostic test for pancreatic cancer using novel biomarkers, reflecting governmental support for advanced IVD products in routine clinical practice.

Restraining Factors

High development and deployment costs, stringent regulatory approvals, complex reimbursement processes, lack of skilled personnel, data privacy concerns, and competition from traditional diagnostic methods are the main factors restricting the in-vitro diagnostics market.

Market Segmentation

The in-vitro diagnostics market share is classified into test type, product, and end user.

- The molecular diagnostics segment dominated the market in 2024, approximately 35%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the test type, the in-vitro diagnostics market is divided into clinical chemistry, molecular diagnostics, immunodiagnostics, haematology, and others. Among these, the molecular diagnostics segment dominated the market in 2024, approximately 35%, and is projected to grow at a substantial CAGR during the forecast period. Superior sensitivity, accuracy, and speed in detecting infectious diseases, rapid adoption of PCR technology, expansion of personalized medicine, and increasing demand for POC testing are driving the molecular diagnostics industry.

- The reagents & kits segment accounted for the largest share in 2024, approximately 50%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the product, the in-vitro diagnostics market is divided into reagents & kits and instruments. Among these, the reagents & kits segment accounted for the largest share in 2024, approximately 50%, and is anticipated to grow at a significant CAGR during the forecast period. High, consistent, and recurring demand; essential consumables used in every diagnostic test; rising disease prevalence and chronic illnesses; and growing adoption of POC diagnostics are driving the reagents & kits indust

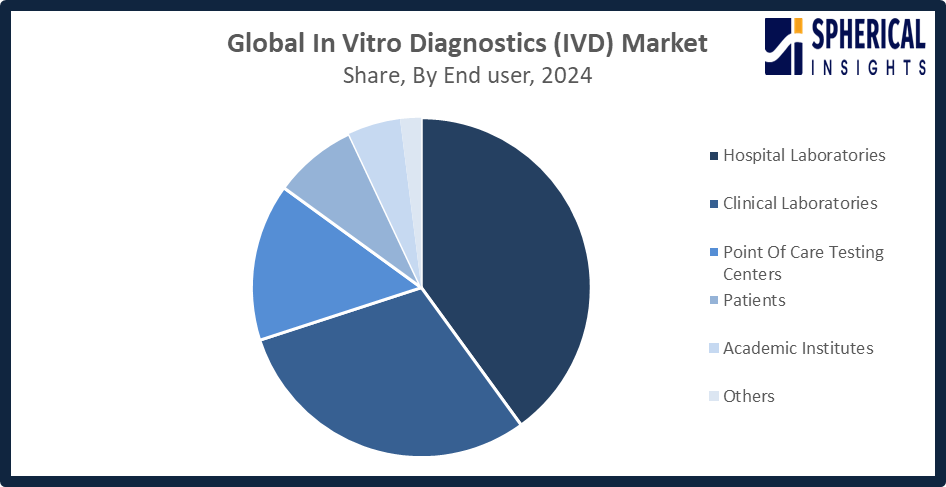

- The hospital laboratories segment accounted for the highest market revenue in 2024, approximately 40%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the in-vitro diagnostics market is divided into hospital laboratories, clinical laboratories, point-of-care testing centers, academic institutes, patients, and others. Among these, the hospital laboratories segment accounted for the highest market revenue in 2024, approximately 40%, and is anticipated to grow at a significant CAGR during the forecast period. Increased patient volume requiring testing for inpatients and emergency cases, advanced infrastructure and funding for specialized laboratory tests, and integration of diagnostic services are bolstering the hospital laboratories market.

Get more details on this report -

Regional Segment Analysis of the In Vitro Diagnostics Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the in-vitro diagnostics market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the largest share of the in-vitro diagnostics market over the predicted timeframe. North America is propelled by strong government support for digital health platforms and electronic health records, molecular diagnostics, next-generation sequencing, AI-enabled diagnostics, and sophisticated point-of-care test systems. The region's position is further reinforced by government initiatives to create new biomarker-based tests and personalized medicine strategies. There is a strong level of laboratory integration of automation and robotics, which improves efficiency, accuracy, and turnaround times for high-volume testing in North America.

Government initiatives include Canada’s November 2025 updated guidance for Class II–IV medical device applications, including IVDs, strengthening regulatory submission requirements and digital processes; the U.S. FDA’s May 2024 final rule regulating LDTs as IVD devices, strengthening oversight and quality standards in the diagnostics market; and Mexico’s Ministry of Health June 2023 update to the NOM 241 SSA1 standard for medical devices and IVDs.

Asia Pacific is expected to grow at a rapid CAGR in the in-vitro diagnostics market during the forecast period. China, Japan, and India are among the nations making significant investments into establishing cutting-edge healthcare systems while implementing new diagnostic methods into their healthcare protocols. Growing population and the prevalence of chronic and infectious diseases have made many countries in the region increasingly interested in using innovative technologies for diagnostics. Increased awareness of the benefits of early disease detection, the availability of private laboratories for diagnostics, and decreased costs associated with manufacturing and performing diagnostic tests make the Asia-Pacific region a key growth engine for the IVD market.

Government initiatives include India’s Free Diagnostics Service Initiative (September 2023), which expands access to essential diagnostic tests including IVDs, and the January 2018 implementation of the Medical Device Rules, 2017, introducing a risk-based regulatory framework for IVDs to improve safety, quality, and market regulation, along with China’s increased investments in healthcare infrastructure and diagnostic technologies supporting IVD solutions in recent years.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the in-vitro diagnostics market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Roche Diagnostics

- Abbott Laboratories

- Danaher Corporation

- Siemens Healthineers

- Thermo Fisher Scientific

- Becton, Dickinson and Company

- bioMerieux

- Sysmex

- QuidelOrtho

- Bio-Rad Laboratories

- Illumina

- Hologic

- Qiagen

- DiaSorin

- Agilent Technologies

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026,Prolight Diagnostics reported analytic progress on its point-of-care platform Psyros in collaboration with BRAINBox Solutions, indicating enhanced biomarker detection capabilities relevant to IVD applications.

- In February 2026, Insight Molecular Diagnostics, Inc. completed key milestones advancing its GraftAssureDx kidney transplant test toward an FDA De Novo IVD submission, including reproducibility studies and clinical sample collection, moving it closer to regulatory clearance.

- In January 2026, iMDx announced preparations for the U.S. commercial launch of GraftAssureDx as clinical trials near completion, highlighting broader adoption of innovative transplant diagnostic solutions

- In December 2025, Roche announced the U.S. launch of next-generation cobas systems and software, expanding laboratory efficiency and IVD assay capabilities with increased throughput and flexibility for molecular testing labs.

- In August 2025,Labcorp announced the launch of the Lumipulse pTau-217/Beta Amyloid 42 Ratio, the first FDA-cleared blood-based IVD test to aid in early Alzheimer’s disease detection, enhancing the IVD test portfolio for neurodegenerative diagnostics.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the in-vitro diagnostics market based on the below-mentioned segments:

Global In Vitro Diagnostics Market, By Test Type

- Clinical Chemistry

- Molecular Diagnostics

- Immunodiagnostics

- Hematology

- Others

Global In Vitro Diagnostics Market, By Product

- Reagents & Kits

- Instruments

Global In Vitro Diagnostics Market, By End User

- Hospitals Laboratories

- Clinical Laboratories

- Point Of Care Testing Centers

- Academic Institutes

- Patients

- Others

Global In Vitro Diagnostics Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

How do technological advancements impact the IVD market?Advancements like molecular diagnostics, AI, and POC testing improve accuracy, speed, and usability. Automation reduces errors and increases efficiency. Digital platforms enable real-time results and data sharing

-

What is the role of molecular diagnostics in the IVD market?Molecular diagnostics detect genetic, infectious, and oncological conditions with high sensitivity. Techniques like PCR and NGS enable early detection and personalized treatments. Continuous innovation drives market growth.

-

How do infectious disease outbreaks influence the IVD market?Outbreaks increase demand for rapid tests like PCR and antigen kits. Governments and labs ramp up procurement. They also drive regulatory flexibility and public-private collaborations

-

How does AI integration benefit the IVD market?AI improves data analysis, predictive insights, and workflow efficiency. It enhances accuracy in molecular and imaging diagnostics. Predictive analytics support early detection and personalized care

-

How do digital health platforms enhance the IVD market?They integrate diagnostic data with electronic records and telemedicine. Remote monitoring and analytics improve decision-making. Digital solutions increase efficiency and adoption

-

What future trends are expected in the IVD market?Trends include AI integration, POC and home-based testing, and molecular diagnostics. Expansion in emerging markets will continue. Innovation, government support, and digital health adoption will shape growth.

Need help to buy this report?