Global Coalescing Agents Market Size, and Share, By Product (Hydrophilic Coalescing Agent and Hydrophobic Coalescing Agent), By Application (Paints & Coatings, Adhesive & Sealants, Inks, Personal Care Ingredients, and Others), By End-Use (Construction, Marine, Automotive, Personal Care & Pharmaceuticals, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2026 - 2035.

Industry: Chemicals & MaterialsGlobal Coalescing Agents Market Insights Forecasts to 2035

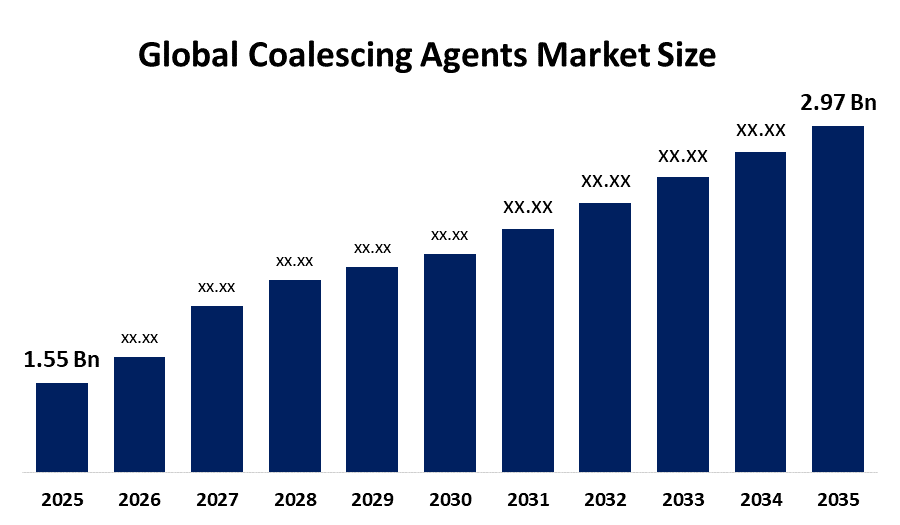

- The Global Coalescing Agents Market Size Was Estimated at USD 1.55 Billion in 2025

- The Market Size is Expected to Grow at a CAGR of around 6.72% from 2026 to 2035

- The Worldwide Coalescing Agents Market Size is Expected to Reach USD 2.97 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global coalescing agents market size was worth around USD 1.55 billion in 2025 and is predicted to grow to around USD 2.97 billion by 2035 with a compound annual growth rate (CAGR) of 6.72% from 2026 to 2035. The coalescing agents market provides opportunities through increasing demand for bio-based low-VOC products, greater usage of waterborne coatings, and fast infrastructure development in emerging markets, along with new high-performance multifunctional additive technologies used in coatings and adhesives and personal care products.

Coalescing Agents Market Key Takeaways

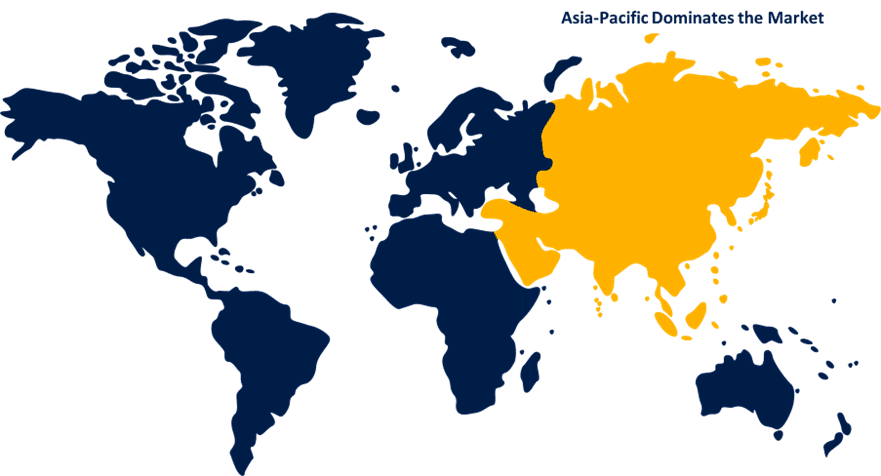

- Asia Pacific dominated the market with the largest share of 47% in 2025.

- North America is expected to grow at the fastest CAGR during the forecast period.

- By product, the hydrophilic coalescing agent segment held a dominant share of the market in 2025, with an approximate 60% share.

- By product, the hydrophobic coalescing agent segment is expected to grow at the fastest CAGR in the market between 2026 and 2035.

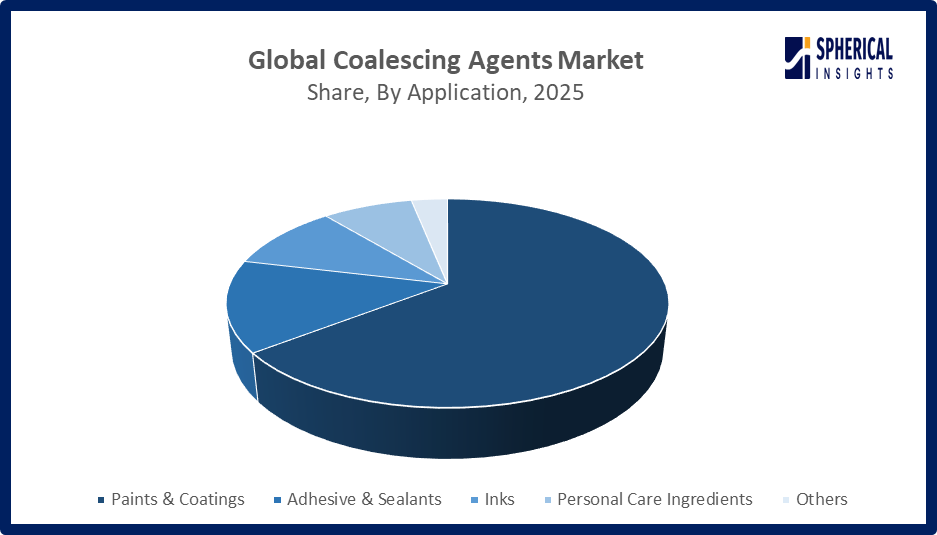

- By application, the paints & coatings segment accounted for a 65% share in the market in 2025.

- By application, the personal care ingredients segment is expected to grow at the highest CAGR in the market during the studied years.

- By end-use, the construction segment registered its dominance in the market in 2025, with approximate 38% market share.

- By end-use, the personal care & pharmaceuticals segment is expected to witness the fastest growth in the market over the forecast period.

Market Overview

The global coalescing agents market comprises specialty additives used mainly in water-based coatings to facilitate film formation by softening polymer particles, which create a smooth, continuous layer at lower temperatures. These agents find extensive use in paints and coatings, adhesives and inks, and personal care products because they enhance product properties such as gloss and durability, adhesion and stability. Market growth is driven by increasing demand for eco-friendly low-VOC coatings, which the construction and automotive sectors require because regulatory pressure forces companies to switch from solvent-based systems to water-based systems. Rapid urbanization and infrastructure development in emerging economies further support demand.

Innovation acts as a key industry development because manufacturers devote resources to creating bio-based coalescing agents, which produce low odors while delivering high-performance results. Research and development investments combined with formulation technology advancements enable manufacturers to create multifunctional additives that help drive market growth throughout the world. In January 2026, the U.S. Environmental Protection Agency finalized stricter VOC emission standards for the Synthetic Organic Chemical Manufacturing Industry under 40 CFR Part 60, Subpart IIIa, mandating advanced recovery systems and monitoring, significantly impacting chemical manufacturers supplying coatings and related industries.

Coalescing Agents Market Trends

- Shift toward low-VOC and eco-friendly solutions: Increasing environmental regulations are driving demand for low-VOC and zero-VOC coalescing agents. Manufacturers are developing sustainable formulations to comply with strict emission standards and reduce environmental impact.

- Rising adoption of water-based coatings: Waterborne coatings are gaining popularity due to their lower toxicity and environmental benefits. This trend is boosting the use of coalescing agents, which are essential for improving film formation and coating performance.

- Growth of bio-based and high-performance additives: There is a growing focus on bio-based coalescing agents derived from renewable sources, along with advanced multifunctional additives that enhance durability, adhesion, and efficiency across industries.

Report Coverage

This research report categorizes the coalescing agents market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the coalescing agents market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the coalescing agents market.

Global Coalescing Agents Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2025 |

| Market Size in 2025: | USD 1.55 Billion |

| Forecast Period: | 2026 – 2035 |

| Forecast Period CAGR 2026 – 2035 : | CAGR of 6.72% |

| 026 – 2035 Value Projection: | USD 2.97 Billion |

| Historical Data for: | 2020-2024 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 95 |

| Segments covered: | By Product By Application |

| Companies covered:: | Eastman Chemical Company, Arkema Group, BASF SE, Dow, Elementis Plc, Celanese Corporation, ADDAPT Chemicals B.V., Synthomer Plc, Chemoxy International Ltd, Evonik Industries AG, Stepan Company, Hallstar, Cargill, Incorporated, Runtai New Material Co., Ltd., Others, and Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global coalescing agents market is driven by rising demand for water-based coatings, which account for over 55% of the total coatings market due to strict VOC regulations. The construction sector, which represents almost 40% of coatings usage, creates strong demand throughout fast urban development. The automotive industry, which manufactures more than 90 million vehicles each year, drives growth through its increasing adoption of environmentally friendly paints. The EU VOC Directive and U.S. EPA standards lead companies to develop products that produce lower emissions through environmental regulations. The Asia-Pacific region maintains a market share above 45% because of industrial growth and infrastructure development, which create ongoing international demand for coalescing agents.

Restraining Factors

The global coalescing agents market encounters restrictions because raw material prices, especially for petrochemical derivatives, create price fluctuations that control more than 60% of production expenses. The strict environmental regulations, which require VOC content to stay below 50 g/L, create difficulties for standard formulations. The high expenses of bio-based alternatives, which emerge as 20-30% more expensive than conventional products, limit their acceptance in price-sensitive markets.

Market Segmentation

Product Insights

Why does the hydrophilic coalescing agent hold the largest share in the coalescing agents industry?

The hydrophilic coalescing agent segment led the market, holding a major 60% share in 2025. The segment growth is due to their superior compatibility with water-based coatings, which dominate the industry amid rising low-VOC regulations. They enable efficient film formation, improved stability, and reduced odor. Additionally, their cost-effectiveness and strong performance in architectural paints, accounting for a major consumption segment, further drive widespread adoption globally.

The hydrophobic coalescing agent segment is expected to show the fastest growth over the forecast period. The segment growth in the market is owing to its enhanced water resistance, durability, and superior film performance. Increasing demand for high-performance coatings in industrial and automotive applications, along with innovation in low-VOC formulations, is accelerating their adoption globally.

Application Insights

Why did the paints & coatings segment dominate the market?

The paints & coatings segment dominated the coalescing agents market with the 65% share in 2025. The segment dominance is attributed to its high consumption in construction, automotive, and industrial applications. Coalescing agents are essential for film formation, durability, and finish quality in water-based coatings. Growing demand for low-VOC, eco-friendly paints and rapid infrastructure development further drive the segment’s leading market share globally.

The personal care ingredients segment is expected to witness the fastest growth in the market over the forecast period. The growth is due to rising demand for eco-friendly and multifunctional formulations. Increasing use of coalescing agents in cosmetics, skincare, and haircare products for improved texture, stability, and sensory performance is driving rapid market expansion globally.

Get more details on this report -

End-Use Insights

Which end-use segment dominated the coalescing agents market?

The construction segment contributed 38% of the market share in 2025. Growth is driven by rising demand for durable, high-performance coatings, sealants, and adhesives in modern construction. Coalescing agents improve film formation, adhesion, and moisture resistance. Increasing adoption of low-VOC, eco-friendly materials, along with rapid urbanization and infrastructure development, further boosts demand, while ongoing investments in sustainable and smart building projects support long-term segment growth.

The personal care & pharmaceuticals segment is expected to expand rapidly in the market in the coming years, as rising demand for high-quality formulations, increasing consumer awareness, and growing healthcare needs. Coalescing agents enhance product stability, texture, and performance, supporting their wider adoption across cosmetics, skincare, and pharmaceutical applications globally.

Regional Segment Analysis of the Coalescing Agents Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Get more details on this report -

What factors have led to Asia Pacific dominance in the coalescing agents market?

Asia Pacific dominated the coalescing agents market by holding the largest share of 47% in 2025. The coalescing agents market results in Asia Pacific domination because China and India experience rapid urban growth while developing their infrastructure and expanding construction projects. The region’s large population and growing middle class drive demand for paints, coatings, and personal care products. The rising demand for high-performance coatings results from increasing industrialization and automotive production activities. The region holds a dominant market position because government initiatives create cost-effective production methods and manufacturers adopt environmentally friendly water-based products.

China Coalescing Agents Market Trends

China’s coalescing agents market is growing due to rapid urbanization, strong construction activity, and expanding automotive production. Water-based low-VOC coatings are becoming more popular because environmental regulations require their use, according to growing demand from consumers. The market experiences consistent growth because infrastructure and industrial projects receive increased funding, and eco-friendly product development progresses.

Why is North America the fastest-growing region in the coalescing agents market?

North America is expected to experience the fastest growth over the forecast period, with an approximate 26% market share. The coalescing agents market experiences its fastest growth in North America because environmental regulations require the use of low-VOC water-based coatings. The construction sector, together with the automotive and industrial sectors, shows strong demand, which drives market growth. The market experiences innovation because companies invest in research and development while developing sustainable, high-performance products. The market growth in the region receives acceleration from major chemical manufacturers and increasing renovation projects.

U.S. Coalescing Agents Market Trends

The United States coalescing agents market is experiencing consistent expansion because of strict VOC regulations and increasing usage of water-based coatings. The market grows due to rising demand from construction and automotive industries and the development of new bio-based and low-odor products. The market experiences accelerated growth due to businesses investing in research and development while sustainability trends shape their operations.

How is the opportunistic rise of Europe in the coalescing agents market?

Europe experiences growth in the coalescing agents market due to environmental regulations which require businesses to develop water-based coatings that have low VOC emissions. The automotive and construction industries drive demand which leads to businesses implementing sustainability objectives through their circular economy programs. The regional market experiences consistent growth because of innovations in bio-based additives and advanced formulation technologies and strong research and development capabilities.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the coalescing agents market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Eastman Chemical Company

- Arkema Group

- BASF SE

- Dow

- Elementis Plc

- Celanese Corporation

- ADDAPT Chemicals B.V.

- Synthomer Plc

- Chemoxy International Ltd

- Evonik Industries AG

- Stepan Company

- Hallstar

- Cargill, Incorporated

- Runtai New Material Co., Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In June 2025, Eastman Chemical Company launched Esmeri CC1N10, a biodegradable cellulose ester micropowder for color cosmetics. Designed to meet strict EU microplastics regulations, it offers enhanced performance, sustainability, and compatibility, supporting the European Commission's goal of reducing environmental microplastic pollution.

- In April 2025, Synthomer and Henkel Corporation partnered to reduce carbon emissions in Henkel’s TECHNOMELT adhesives across Europe, India, the Middle East, and Africa. Using CLIMA-branded products and renewable energy, the collaboration ensures measurable, at least 20% cradle-to-gate carbon footprint reductions.

- In November 2024, Henkel Corporation partnered with Celanese Corporation to advance circularity by producing water-based adhesives from captured CO2. Leveraging CCU technology, the collaboration supports sustainable packaging solutions and reduces environmental impact across consumer goods and industrial applications.

- In July 2024, the U.S. Environmental Protection Agency proposed a rule under the Toxic Substances Control Act to regulate N-methylpyrrolidone (NMP), aiming to protect workers and consumers through usage bans, concentration limits, and stricter safety, labeling, and recordkeeping requirements across industrial and consumer applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the coalescing agents market based on the below-mentioned segments:

Global Coalescing Agents Market, By Product

- Hydrophilic Coalescing Agent

- Hydrophobic Coalescing Agent

Global Coalescing Agents Market, By Application

- Paints & Coatings

- Adhesive & Sealants

- Inks

- Personal Care Ingredients

- Others

Global Coalescing Agents Market, By End-Use

- Construction

- Marine

- Automotive

- Personal Care & Pharmaceuticals

- Others

Global Coalescing Agents Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.How are environmental regulations impacting the demand for coalescing agents globally?Stringent environmental regulations limiting VOC emissions are driving coalescing agent demand, as over 62% of manufacturers shift to waterborne coatings, while solvent-based coatings contain up to 84% VOCs, accelerating the adoption of eco-friendly formulations.

-

2.What economic factors are influencing pricing trends in the coalescing agents market?Economic factors such as fluctuating crude oil prices, energy costs, and inflation influence coalescing agent pricing, with feedstock-driven costs causing 6-8% price variations and premium products exceeding USD 3,500 per ton, impacting affordability and demand.

-

3.How is R&D investment transforming product innovation in the coalescing agents market?R&D investment is transforming coalescing agent innovation, with over 70% of R&D focused on low-VOC and advanced formulations, enabling improved film performance, polymer compatibility, and efficiency, driving 6-7% market growth annually.

-

4.What technological advancements are improving coalescing agent performance?Technological advancements such as bio-based coalescing agents, low-VOC formulations, and high-efficiency additives are improving performance, with innovations reducing emissions by over 60% and enabling up to 25% energy savings in coating processes.

-

5.What are the major supply chain challenges faced by coalescing agent manufacturers?Major supply chain challenges for coalescing agent manufacturers include raw material price volatility linked to petrochemicals (impacting over 60% of costs), supply disruptions, and complex global logistics, increasing production costs and causing frequent delays.

-

6.How are regulatory policies shaping future opportunities in the coalescing agents market?Regulatory policies enforcing VOC limits (often below 50 g/L) are creating opportunities by driving a 7% rise in low-VOC coalescing agent demand, encouraging innovation in bio-based and sustainable formulations globally.

-

7.What impact do raw material price fluctuations have on market stability?Raw material price fluctuations destabilize the coalescing agents market, as feedstocks account for 40-70% of production costs and experience 30-50% price swings, reducing margins by up to 10% and disrupting pricing stability.

Need help to buy this report?