China Smart Building Market Size, Share, By Solution (Safety & Security Management, Energy Management, Building Infrastructure Management, Integrated Workplace Management System), By Component (Hardware, Software, Services), By Connectivity Type (Wired Technology, Wireless Technology), By End Use (Residential, Commercial, Healthcare, Retail, Academic, Industrial), China Smart Building Market Insights, Industry Trend, Forecasts to 2035.

Industry: Information & TechnologyChina Smart Building Market Insights Forecasts to 2035

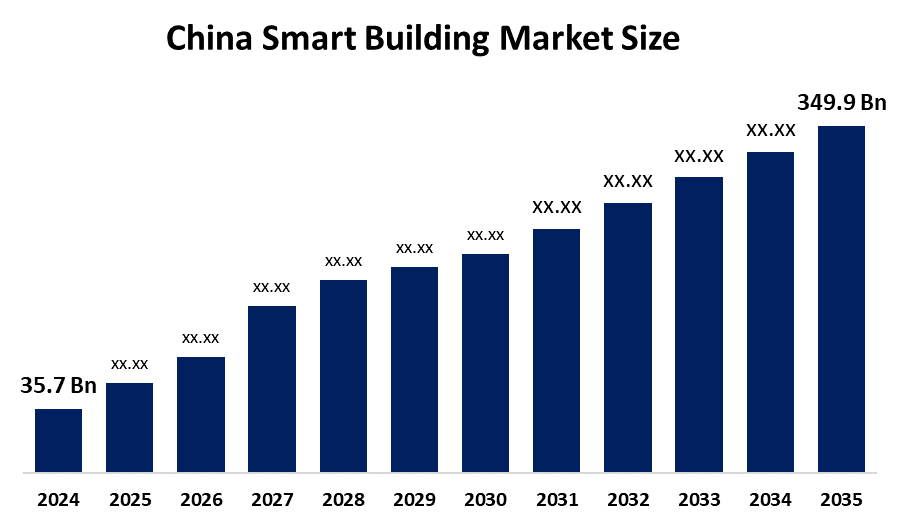

- China Smart Building Market Size 2024: USD 35.7 Billion

- China Smart Building Market Size 2035: USD 349.9 Billion

- China Smart Building Market CAGR 2024: 23.06%

- China Smart Building Market Segments: Solution, Component, Connectivity Type, and End Use.

Get more details on this report -

The China smart building market combines digital automation solutions, IoT devices, AI-driven analytics, and centralized control solutions to enhance energy efficiency, productivity, and safety. The adoption of smart infrastructure solutions is increasing in residential buildings, office skyscrapers, healthcare facilities, retail spaces, educational institutions, and industrial parks. The rising need for smart city development and carbon neutrality is fueling the adoption of smart building solutions. The latest technologies like AI-powered predictive maintenance, 5G connectivity solutions, and cloud-based monitoring solutions are revolutionizing the management of modern infrastructure in China.

The China smart building market is driven by the strong government focus on green building, energy efficiency, and digital infrastructure development. The smart city development projects and increasing electricity costs are encouraging the adoption of building energy management solutions, safety solutions, and intelligent automation solutions. The rising demand for cybersecurity, workplace management, and sustainable facilities operations is further fueling the demand for smart building solutions.

Market Dynamics of the China Smart Building Market:

The China smart building market is driven by rapid urbanization, increased development of commercial real estate, and pursuit of carbon neutrality within China. Investment in smart cities and digital infrastructure has been a catalyst for implementing intelligent energy management systems, advanced camera/surveillance systems and advanced heating, air conditioning and ventilation systems. Companies and real estate developers are focusing on their environmental, social and governance (ESG) goals; improving operational efficiency; and providing better tenant experiences with integrated smart buildings through the application of artificial intelligence (AI), Internet of Things (IoT) [also referred to as "smart devices"] and near real-time data analytics platforms.

The primary barriers to the future growth of the China smart building market are high initial project costs, integration with legacy systems, and vulnerability to cyber-attack. Many end-users have experienced project delays, mainly due to the lack of uniformed interoperability between the different vendors involved in such projects. Small developers are often unable to implement large-scale automation solutions due to financial constraints; however, privacy concerns regarding the use of data and dependence on advanced semiconductor products could hinder the ability to maintain long-term scalable automation and operational resilience.

The future business growth of the China smart building market remains positive due to the need to improve energy efficiency, new forms of AI-based security systems and integrated space management systems. The creation of smart hospitals, digital campuses and automated industrial parks will provide additional growth opportunities. The continuous development of wireless communication, cloud-based services and predictive analytics solutions will strongly influence the modernization of sustainable infrastructure throughout China.

China Smart Building Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | 349.9 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 23.06% |

| 2035 Value Projection: | USD 349.9 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 220 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Solution, By Connectivity Type |

| Companies covered:: | Honeywell International Inc., Siemens AG, Schneider Electric SE, Johnson Controls International, Huawei Technologies Co., Ltd., ABB Ltd., Hikvision Digital Technology Co., Ltd., Zhejiang Dahua Technology Co., Ltd., Delta Electronics, Inc., Legrand SA |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Market Segmentation

The China smart building market share is classified into solution, component, connectivity type, and end use.

By Solution:

The China smart building market is divided by solution into safety & security management, energy management, building infrastructure management, and Integrated workplace management system (IWMS). Among these, safety & security management dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Subsystems, including access control systems, video surveillance systems, and fire and life safety systems, are widely deployed across commercial and residential complexes. Rising security concerns, urban density, and regulatory mandates are accelerating investments in intelligent monitoring, threat detection, and centralised emergency response systems nationwide.

By Component:

The China smart building market is divided by component into hardware, software, and services. Among these, hardware dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Hardware components such as smart sensors, controllers, cameras, HVAC control units, and lighting management devices form the backbone of intelligent infrastructure. Increasing installation of IoT-enabled equipment across new construction projects and retrofitting initiatives drives hardware demand. However, software platforms and services including consulting, implementation, and support are steadily expanding as system complexity increases.

By Connectivity Type:

The market is divided by connectivity type into wired technology and wireless technology. Among these, wireless technology dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Wireless connectivity enables flexible installation, scalability, and integration with IoT devices, reducing cabling costs and deployment time. Adoption of 5G, Wi-Fi 6, and low-power wide-area networks supports real-time data transmission and remote monitoring. Growing demand for adaptive and cloud-integrated building systems is strengthening the shift toward wireless infrastructure solutions.

By End Use:

The China smart building market is divided by end use into residential, commercial, healthcare, retail, academic, and industrial. Among these, commercial dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. Commercial buildings such as office towers, malls, and mixed-use complexes are prioritizing smart technologies to enhance energy efficiency, tenant safety, and operational optimization. Increasing demand for intelligent HVAC systems, lighting management, surveillance platforms, and integrated workplace management tools is driving widespread adoption in China’s expanding urban business districts.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the China smart building market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in China Smart Building Market:

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- Johnson Controls International

- Huawei Technologies Co., Ltd.

- ABB Ltd.

- Hikvision Digital Technology Co., Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- Delta Electronics, Inc.

- Legrand SA

Recent Developments in China Smart Building Market:

In April 2025, Huawei Technologies Co., Ltd. launched an upgraded AI-powered Smart Building Solution integrating IoT sensors, edge computing, and cloud-based building management systems to enhance predictive maintenance, energy optimization, and real-time security monitoring across commercial and mixed-use developments in China.

In February 2025, Schneider Electric SE expanded its EcoStruxure Building platform in China with advanced carbon tracking, AI-driven HVAC optimization, and cloud-enabled energy analytics to support commercial developers in meeting sustainability and ESG targets.

In June 2024, Hikvision Digital Technology Co., Ltd. introduced next-generation AI-based video surveillance systems designed for smart offices and residential complexes, enhancing facial recognition, behavioral analytics, and centralized security management capabilities.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the China, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the China smart building market based on the below-mentioned segments

China Smart Building Market, By Solution

- Safety & Security Management

- Energy Management

- Building Infrastructure Management

- Integrated Workplace Management System

China Smart Building Market, By Component

- Hardware

- Software

- Services

China Smart Building Market, By Connectivity Type

- Wired Technology

- Wireless Technology

China Smart Building Market, By End Use

- Residential

- Commercial

- Healthcare

- Retail

- Academic

- Industrial

Frequently Asked Questions (FAQ)

-

1. What is the projected growth of the China smart building market by 2035?The China smart building market is projected to grow from USD 35.7 billion in 2024 to USD 349.9 billion by 2035, registering a CAGR of 23.06% during 2025–2035. This strong growth reflects rapid digital infrastructure development, smart city initiatives, and rising demand for energy-efficient buildings. The market expansion is driven by AI integration, IoT adoption, and increasing commercial real estate modernization across China.

-

2. What are the key drivers of the China smart building market?The market is primarily driven by rapid urbanization, smart city investments, and China’s carbon neutrality goals. Growing electricity costs and ESG compliance requirements are accelerating the adoption of building energy management and intelligent automation systems. Additionally, AI-powered analytics, IoT-enabled devices, and 5G connectivity are strengthening real-time building monitoring and operational efficiency.

-

3. Which solution segment dominates the China smart building market?Safety & Security Management dominates the China Smart Building Market due to rising urban density and increasing security concerns. Solutions such as access control systems, video surveillance, and fire & life safety systems are widely deployed in commercial and residential buildings. Regulatory mandates and demand for centralized monitoring systems further support the growth of this segment.

-

4. Why is wireless technology gaining traction in smart buildings in China?Wireless technology is gaining popularity due to its flexibility, scalability, and lower installation complexity compared to wired systems. Technologies such as 5G, Wi-Fi 6, and low-power networks enable real-time data transmission and remote building monitoring. The shift toward cloud-integrated smart systems is further accelerating wireless connectivity adoption across commercial and industrial facilities.

-

5. Which end-use sector leads the China smart building market?The commercial sector leads the market, driven by increasing investments in office buildings, malls, and mixed-use complexes. Commercial developers prioritize smart HVAC systems, lighting automation, surveillance platforms, and workplace management tools to improve efficiency and tenant experience. Rising demand for operational cost optimization and sustainability compliance further strengthens adoption in this segment.

-

6. What challenges affect the growth of the China smart building market?High initial investment costs and integration challenges with legacy infrastructure remain major barriers to adoption. Cybersecurity risks and lack of interoperability between multiple vendors can delay project implementation. Additionally, smaller developers may face financial limitations, restricting large-scale deployment of intelligent automation solutions.

-

7. Who are the key players in the China smart building market?Major companies operating in the China smart building market include Honeywell International Inc., Siemens AG, Schneider Electric SE, Johnson Controls International, Huawei Technologies Co., Ltd., ABB Ltd., Hikvision Digital Technology Co., Ltd., Zhejiang Dahua Technology Co., Ltd., Delta Electronics, Inc., and Legrand SA. These players focus on product innovation, AI-based automation, and strategic collaborations to strengthen their market presence.

-

8. What are the future opportunities in the China smart building market?Future growth opportunities lie in smart hospitals, digital campuses, automated industrial parks, and AI-based predictive maintenance systems. Increasing adoption of integrated workplace management platforms and sustainable infrastructure solutions will further drive market expansion. Continuous advancements in cloud computing, wireless connectivity, and energy optimization technologies will shape the long-term evolution of China’s smart building ecosystem.

Need help to buy this report?