China Electronic Design Automation (EDA) Tools Market Size, Share, By Tool Type (IC Physical Design & Verification, Semiconductor IP, PCB & MCM, Services), By Deployment (On-Premise, Cloud-Based), By Application (Consumer Electronics, Automotive, Telecommunications, Industrial, Aerospace & Defense), By End Use (Foundries, Fabless Companies, Integrated Device Manufacturers (IDMs), Research Institutes), China Electronic Design Automation (EDA) Tools Market Insights, Industry Trend, Forecasts to 2035

Industry: Information & TechnologyChina Electronic Design Automation (EDA) Tools Market Insights Forecasts to 2035

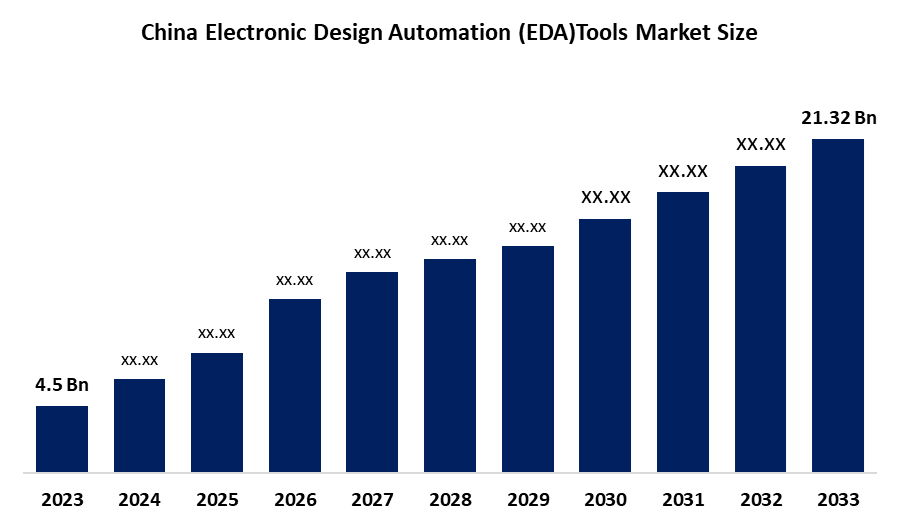

- China Electronic Design Automation (EDA) Tools Market Size 2024: USD 4.5 Billion

- China Electronic Design Automation (EDA) Tools Market Size 2035: USD 21.32 Billion

- China Electronic Design Automation (EDA) Tools Market CAGR 2024: 15.19%

- China Electronic Design Automation (EDA) Tools Market Segments: Tool Type, Deployment, Application, and End Use.

Get more details on this report -

The China electronic design automation (EDA) tools market operates through its software platforms and services, which support the design and verification, simulation and manufacturing optimisation processes of semiconductor chip development. The tools function as essential resources that enable designers to create integrated circuits that operate at advanced process nodes, including 7nm and 5nm and all smaller nodes. The market provides support to fabless semiconductor companies and integrated device manufacturers, foundries and research institutions that work on AI chips, automotive electronics, 5G infrastructure, IoT devices and high-performance computing.

China's semiconductor self-sufficiency initiative, together with rising investments in domestic chip design companies and the rapid expansion of AI, automotive electronics and advanced communication technologies, drives market growth. The combination of government programs that support local semiconductor development and increasing research and development investment, along with the need for advanced system-on-chip designs, has resulted in greater use of EDA tools. The rising availability of cloud-based simulation platforms, together with AI-powered chip design optimisation tools is transforming how companies compete in the market.

Market Dynamics of the China Electronic Design Automation (EDA) Tools Market:

The driving forces behind this market include the rapid growth of China's semiconductor industry, the national integrated circuit development programs that receive government funding, and the increasing need for advanced chips used in AI systems, automotive electronics, 5G technology, and consumer devices. Designers require advanced EDA solutions because chip design becomes more complex through smaller process nodes, and the industry demands high-performance chips that consume less power. Domestic EDA vendors establish strategic partnerships with foundries, which enable them to develop stronger capabilities.

The challenges faced by the market include reliance on foreign EDA software vendors, export control restrictions, high development costs for advanced EDA platforms, and a lack of expertise in cutting-edge process node technology. The design process becomes harder to manage because design teams need to learn advanced design tools while maintaining their current workflow. Established global vendors create competitive pressure, which makes it difficult for new domestic businesses to enter the market.

The future maintains strong prospects because companies increase their localization efforts, demand for automotive semiconductors continues to grow, AI chip startups expand their operations, and advanced manufacturing nodes receive higher investment. The transition toward cloud-enabled EDA tools, AI-assisted design automation, and domestic IP core development will improve competitive position. The demand for secure EDA platforms which provide strong performance and scalable functionality will increase as China builds up its semiconductor supply chain system.

China Electronic Design Automation (EDA) Tools Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 4.5 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 15.19% |

| 2035 Value Projection: | USD 21.32 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 210 |

| Tables, Charts & Figures: | 95 |

| Segments covered: | By Deployment |

| Companies covered:: | Synopsys, Inc., Cadence Design Systems, Inc., Siemens EDA, Silvaco Group, Inc., Altium Limited, Empyrean Technology Co., Ltd., Xpeedic Technology Inc., Primarius Technologies Co., Ltd., Beijing Huada Jiutian Software Co., Ltd., Semitronix Corporation, Zuken Ltd., Platform Design Automation, and Inc and other kay palyers |

| Pitfalls & Challenges: | and COVID-19 Impact Analysis |

Get more details on this report -

Market Segmentation

The China electronic design automation (EDA) tools market share is classified into tool type, deployment, application, and end use.

By Tool Type:

The China electronic design automation tools market is divided by tool type into IC physical design & verification, semiconductor IP, PCB & MCM, and services. Among these, IC physical design & verification dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. This dominance is primarily due to increasing chip complexity, advanced process node migration, demand for system-on-chip architectures, and the need for accurate simulation, timing analysis, and layout verification tools to ensure manufacturing precision and performance reliability.

By Deployment:

The China electronic design automation tools market is divided by deployment into on-premise and cloud-based. Among these, on-premise deployment dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. On-premise solutions remain preferred due to data security concerns, protection of sensitive intellectual property, and strict compliance requirements within semiconductor design workflows. Large chipmakers and foundries in China prioritize secure internal infrastructure to safeguard proprietary designs, particularly in strategic industries such as defense, telecommunications, and AI processors.

By Application:

The China electronic design automation tools market is divided by application into consumer electronics, automotive, telecommunications, industrial, and aerospace & defence. Among these, consumer electronics dominated in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. This dominance is driven by China’s strong smartphone, wearable, computing, and smart device manufacturing ecosystem. Continuous innovation in processors, power management ICs, display drivers, and connectivity chips significantly increases demand for advanced EDA tools to enable rapid product development cycles.

By End Use:

The China electronic design automation tools market is divided by end use into foundries, fabless companies, integrated device manufacturers (IDMs), and research institutes. Among these, fabless companies dominated the share in 2024 and is anticipated to grow at a remarkable CAGR during the forecast period. The rapid emergence of AI chip startups, 5G chipset developers, and automotive semiconductor designers in China has significantly expanded demand for high-performance design and verification tools. Fabless firms rely heavily on EDA platforms to accelerate time-to-market and compete globally.

Competitive Analysis:

The report offers the appropriate analysis of the key organisations/companies involved within the China electronic design automation (EDA) tools market, along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

Top Key Companies in China Electronic Design Automation (EDA) Tools Market:

- Synopsys, Inc.

- Cadence Design Systems, Inc.

- Siemens EDA

- Silvaco Group, Inc.

- Altium Limited

- Empyrean Technology Co., Ltd.

- Xpeedic Technology Inc.

- Primarius Technologies Co., Ltd.

- Beijing Huada Jiutian Software Co., Ltd.

- Semitronix Corporation

- Zuken Ltd.

- Platform Design Automation, Inc.

Recent Developments in China Electronic Design Automation (EDA) Tools Market:

In March 2025, Empyrean Technology Co., Ltd. announced the expansion of its advanced-node digital implementation and verification platform to support sub-7nm process technologies. The product enhancement aims to strengthen China’s domestic IC design ecosystem and reduce reliance on foreign EDA vendors for AI and high-performance computing chip development.

In February 2025, Synopsys, Inc. strengthened its collaboration with leading Chinese semiconductor manufacturers to optimize advanced process node enablement and AI-driven design automation workflows, supporting complex automotive and data center chip architectures.

In January 2025, Primarius Technologies Co., Ltd. launched a cloud-based parasitic extraction and sign-off verification platform targeting Chinese fabless semiconductor companies, improving scalability, accessibility, and time-to-market for advanced SoC designs.

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at the China, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the China electronic design automation (EDA) tools market based on the below-mentioned segments:

China Electronic Design Automation (EDA) Tools Market, By Tool Type

- IC Physical Design & Verification

- Semiconductor IP

- PCB & MCM

- Services

China Electronic Design Automation (EDA) Tools Market, By Deployment

- On-Premise

- Cloud-Based

China Electronic Design Automation (EDA) Tools Market, By Application

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial

- Aerospace & Defence

China Electronic Design Automation (EDA) Tools Market, By End Use

- Foundries

- Fabless Companies

- Integrated Device Manufacturers (IDMs)

- Research Institutes

Frequently Asked Questions (FAQ)

-

What is driving the growth of the China electronic design automation (EDA) tools market?The market is primarily driven by China’s semiconductor self-sufficiency strategy, increasing investments in domestic chip design companies, and rising demand for AI, automotive, and 5G semiconductors. Growing chip complexity at advanced nodes such as 7nm and 5nm requires sophisticated EDA solutions. Government-backed integrated circuit development programs further accelerate market expansion.

-

What is the projected market size of the China EDA tools market by 2035?The China Electronic Design Automation (EDA) Tools Market is projected to grow from USD 4.5 billion in 2024 to USD 21.32 billion by 2035. The market is expected to register a CAGR of 15.19% during the forecast period 2025–2035. Strong growth reflects rising semiconductor R&D investments and increasing localization efforts.

-

Which segment dominates the China EDA tools market by tool type?IC Physical Design & Verification dominates the market due to increasing chip complexity and migration to advanced semiconductor nodes. The demand for accurate simulation, layout verification, and timing analysis tools continues to rise. This segment remains critical for ensuring performance reliability and manufacturing precision.

-

Why does on-premise deployment lead the China EDA market?On-premise deployment leads due to strict data security requirements and protection of sensitive intellectual property. Semiconductor firms prefer secure internal infrastructures to safeguard proprietary chip designs. Strategic industries such as defense, AI processors, and telecommunications prioritize controlled environments.

-

Which application segment holds the largest share in China’s EDA tools market?Consumer electronics holds the largest share due to China’s strong smartphone, computing, and smart device manufacturing ecosystem. Continuous innovation in processors, connectivity chips, and power management ICs drives tool demand. Rapid product development cycles further increase reliance on advanced EDA platforms.

-

Who are the key end users in the China EDA tools market?Fabless semiconductor companies represent the dominant end-user segment in China. The expansion of AI chip startups, automotive semiconductor developers, and 5G chipset firms fuels demand for advanced design tools. These firms depend heavily on EDA platforms to accelerate time-to-market and compete globally.

-

What challenges does the China EDA tools market face?The market faces challenges such as dependence on foreign EDA vendors and export control restrictions. High development costs for advanced EDA platforms and limited expertise at cutting-edge nodes also restrict growth. Competitive pressure from established global vendors creates additional barriers for domestic players.

-

What are the future opportunities in the China EDA tools market?Future opportunities lie in localization of EDA software, cloud-enabled design platforms, and AI-assisted automation tools. Growing investment in automotive semiconductors, advanced manufacturing nodes, and domestic IP core development will strengthen the ecosystem. Secure, scalable, and high-performance EDA solutions will see increasing demand.

Need help to buy this report?