Global Catalyst Aging Testing Market Size, Share, and COVID-19 Impact Analysis, By Material Type (Thermal Aging Testing, Chemical, Mechanical, and Combined), By Application (Catalyst Aging, Catalyst Ageing Cycle Development, After-treatment Efficiency Measurement, Catalyst Light-off Evaluation, and Dynamic Cycle Evaluation), By End-Use (Automotive, Petrochemicals, Chemicals, Pharmaceuticals, Environmental, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Catalyst Aging Testing Market Insights Forecasts to 2035

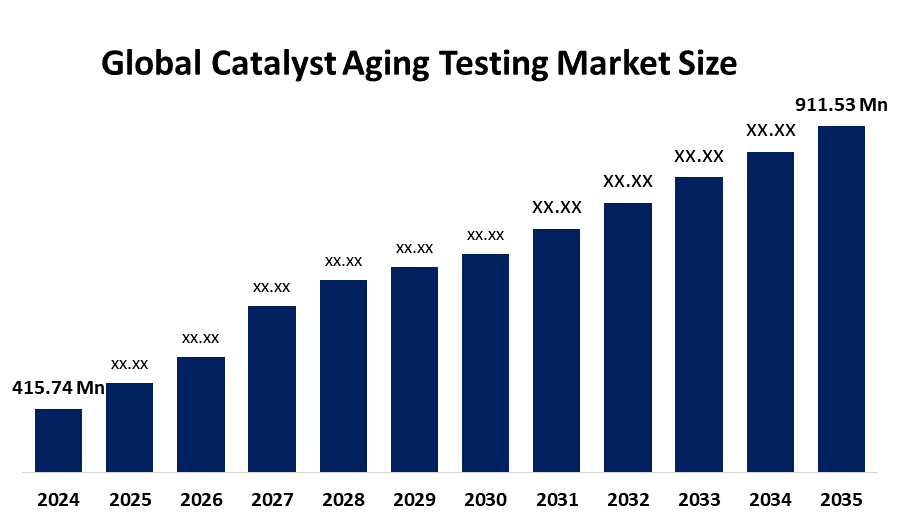

- The Global Catalyst Aging Testing Market Size Was Estimated at USD 415.74 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 7.4% from 2025 to 2035

- The Worldwide Catalyst Aging Testing Market Size is Expected to Reach USD 911.53 Million by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, The Global Catalyst Aging Testing Market Size was worth around USD 415.74 Million in 2024 and is predicted to Grow to around USD 911.53 Million by 2035 with a Compound Annual Growth Rate (CAGR) of 7.4% from 2025 to 2035. The catalyst aging testing market is growing rapidly due to tightening environmental regulations requiring strict emission control (Euro 7/China VI), rising demand for long-life catalysts in automotive/petrochemical sectors, and the need for accelerated, AI-driven testing to reduce R&D costs.

Market Overview

The global catalyst aging testing market encompasses the sector dedicated to assessing the long-term performance, durability, and deactivation behavior of catalysts used in automotive exhaust systems, petrochemical operations, and industrial chemical production. Aging tests evaluate catalyst performance under prolonged thermal, chemical, and mechanical stresses, ensuring compliance with emissions and efficiency standards. These tests are especially critical in automotive applications, where catalysts must meet stringent regulations such as EURO 7 and other global norms, driving demand for accurate aging assessments.

In March 2026, the European Commission issued COM (2026) 108 final, updating heavy-duty vehicle assessment methods under Euro 7 (EU 2024/1257). The guidance mandates rigorous catalyst aging validation up to 200,000 km, supporting on-board monitoring, real-driving emissions testing, and precise bench simulations ahead of its implementation on November 29, 2026.

Rising vehicle production, projected to surpass 1.5 billion units by 2030, along with tightening emission control requirements, is significantly expanding market potential. In the petrochemical and refining sectors, aging testing plays a crucial role in optimizing catalyst lifecycles and improving operational efficiency. Growing R&D in advanced catalyst formulations and testing technologies, combined with increasing environmental compliance costs, is driving demand for high-precision testing solutions.

Additionally, expansion in renewable energy and chemical processing industries is creating long-term growth opportunities for catalyst aging testing services and equipment. In August 2025, the California Air Resources Board updated its Heavy-Duty Omnibus regulations, aligning durability requirements, in-use testing, and warranties for 2027 and later engines with federal standards. At the same time, the EPA released revised SCR inducement guidance to ensure reliable long-term catalyst performance and prevent premature derating, further strengthening emissions compliance and testing requirements.

Report Coverage

This research report categorizes the catalyst aging testing market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the catalyst aging testing market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the catalyst aging testing market.

Driving Factors

Major factors driving the global catalyst aging testing market include growing demand for long-lasting, high-performance catalysts in the chemical, petrochemical, and automotive sectors. Strict environmental regulations compel manufacturers to maintain catalyst efficiency and durability. The increasing use of advanced analytical methods, such as spectroscopy and thermal analysis, allows accurate tracking of catalyst degradation. Furthermore, the expansion of chemical processing industries, rising investments in renewable energy, and emphasis on cost efficiency in industrial operations are fueling market growth. Enhanced R&D efforts for next-generation catalysts are also accelerating global adoption of catalyst aging testing, ensuring both reliability and regulatory compliance. In June 2024, the U.S. EPA regulatory framework (Appendix VIII to Part 86) continues to guide catalyst aging testing, mandating standardized procedures and compliance protocols. These regulations ensure vehicle emissions systems remain effective, driving demand for certified testing services and reinforcing long-term market growth in catalyst durability assessment.

Restraining Factors

Key restraining factors include high equipment and operational costs for advanced aging testing systems, limiting adoption among small enterprises. Technical complexities in simulating diverse real-world conditions accurately pose challenges. Additionally, a shortage of skilled personnel to operate sophisticated testing equipment and interpret complex degradation data hinders market growth.

Market Segmentation

The catalyst aging testing market share is classified into material type, application, and end-use.

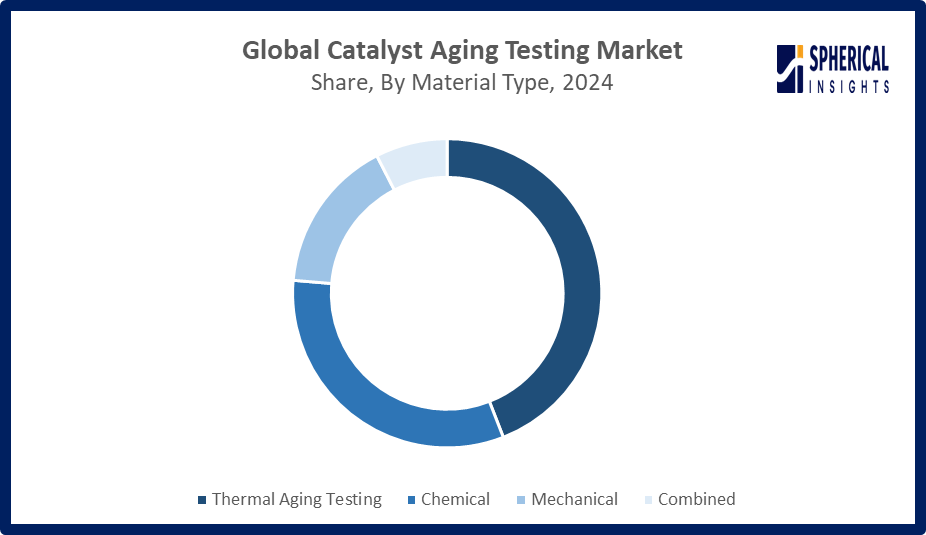

- The thermal aging testing segment dominated the market in 2024, approximately 44% and is projected to grow at a substantial CAGR during the forecast period.

Based on the material type, the catalyst aging testing market is divided into thermal aging testing, chemical, mechanical, and combined. Among these, the thermal aging testing segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. This growth dominance is attributed to the universal susceptibility of catalysts to high-temperature degradation across automotive and industrial applications. Stringent emissions regulations requiring validation of catalyst durability under extreme thermal conditions further drive adoption. Additionally, the global shift toward electrification and hydrogen technologies necessitates thermal stability testing for next-generation catalyst materials used in fuel cells and emission control systems.

Get more details on this report -

- The catalyst aging segment accounted for the largest share in 2024, approximately 37% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the catalyst aging testing market is divided into catalyst aging, catalyst ageing cycle development, after-treatment efficiency measurement, catalyst light-off evaluation, and dynamic cycle evaluation. Among these, the catalyst aging segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The segment growth is due to the universal industry requirement to validate long-term catalyst durability and performance stability under simulated operational conditions. This testing enables manufacturers to predict degradation patterns, optimize formulations, and extend catalyst lifespan, directly reducing replacement costs and operational downtime. Stringent environmental regulations mandating sustained emissions compliance across automotive and industrial sectors further drive adoption, as companies must verify that catalysts maintain efficiency throughout their operational lifecycle to meet regulatory standards and avoid penalties.

- The automotive segment accounted for the highest market revenue in 2024, approximately 48% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end-use, the catalyst aging testing market is divided into automotive, petrochemicals, chemicals, pharmaceuticals, environmental, and others. Among these, the automotive segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The automotive segment market growth is owing to increasingly stringent global emissions regulations, such as Euro 7 and China VI, which mandate rigorous catalyst durability testing for vehicle certification. The rapid expansion of electric vehicle production, particularly fuel cell electric vehicles requiring specialized catalyst validation, further drives demand. Additionally, automotive manufacturers must verify emissions control systems remain effective throughout extended warranty periods, compelling investment in comprehensive catalyst aging tests.

Regional Segment Analysis of the Catalyst Aging Testing Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Get more details on this report -

Asia Pacific is anticipated to hold the largest share of the catalyst aging testing market over the predicted timeframe.

Asia Pacific is anticipated to hold the 45% share of the catalyst aging testing market over the predicted timeframe. The region growth in the catalyst aging testing market, driven by rapid industrialization, expanding automotive production, and stringent emission regulations in countries such as China, India, and Japan. Increasing investments in petrochemical and chemical processing sectors, rising demand for durable and high-performance catalysts, and government initiatives promoting environmental compliance are boosting the adoption of catalyst aging tests. Additionally, the region’s growing R&D activities in advanced catalyst formulations and testing technologies further accelerate market growth, ensuring long-term operational efficiency and regulatory adherence. In July 2025, SGS INSPIRE attended China’s 2025 Annual Conference on carbon neutrality and emission control in Xiamen. Key stakeholders, including government, industry, and academia, discussed vehicle emission regulations, testing technologies, and emission-reducing components, while CRAES unveiled the tentative timeline for China VII emission standards.

North America is expected to grow at a rapid CAGR in the catalyst aging testing market during the forecast period. The region is rapidly growing in the catalyst aging testing market, with an approximate market share in 25%, led by the United States and Canada. Strict emission regulations, such as EPA standards and California’s CARB programs, drive demand for reliable catalyst durability testing. High adoption of advanced automotive technologies, growing petrochemical and industrial sectors, and increasing R&D investments in next-generation catalysts further support market expansion, ensuring compliance, operational efficiency, and long-term sustainability across industries. In February 2026, the U.S. EPA rescinded the 2009 Greenhouse Gas Endangerment Finding, removing future GHG standards. However, catalyst durability and in-use aging requirements remain under multi-pollutant and heavy-duty programs, with CARB maintaining 2026-2027 model-year alignments for warranties, testing, and catalyst performance verification.

Europe is experiencing strong growth in the catalyst aging testing market, led by Germany, France, and the UK. Stringent emission standards such as Euro 7, along with an increasing focus on sustainable automotive and industrial processes, are driving demand for reliable catalyst testing solutions. Additionally, expanding R&D in advanced catalyst formulations, the growth of chemical and petrochemical industries, and supportive government initiatives for environmental compliance are further accelerating market adoption and long-term growth across the region.

In September 2025, Europe enacted Implementing Regulations (EU) 2025/1706 and 2025/1707, introducing Euro 7-TEMP standards. These regulations impose stricter exhaust emission limits, enhanced onboard monitoring systems, anti-tampering requirements, and extended catalyst durability standards of up to 200,000 km. As a result, OEMs are required to conduct rigorous accelerated aging tests to meet type approval and ensure ongoing regulatory compliance.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the catalyst aging testing market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Intertek Group plc

- Johnson Matthey PLC

- Umicore

- BASF SE

- SGS

- Fisher Barton

- Cormetech

- TUV SUD

- Clariant AG

- JGC C&C

- Heraeus Precious Metals

- Evonik Industries AG

- FEV Group

- Honeywell International Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In February 2026, Honeywell announced an amended agreement to acquire Johnson Matthey’s Catalyst Technologies business for £1.325 billion, extending the long-stop date to July 21. The acquisition enhances Honeywell UOP’s refining, petrochemical, and renewable fuel capabilities, expands its installed base, and creates synergies across process technologies and automation.

- In February 2026, Johnson Matthey plc unveiled its advanced Cracking Evaluation (ACE) units at the Savannah lab, acquired from Kayser Technology Inc. The multi-million-dollar investment boosts JM’s fluid catalytic cracking additive innovation, enabling higher-resolution testing, accelerating catalyst development, and strengthening commercialization of next-generation FCC solutions.

- In May 2025, Umicore announced a new advanced facility at its Catoosa, US site. The multi-million-dollar investment, backed by strategic specialty chemicals partnerships, will start Grubbs Catalyst production by early 2027, strengthening Umicore’s global leadership in homogeneous catalysts and advancing industrial-scale sustainable chemistry.

- In December 2024, BASF inaugurated its Catalyst Development and Solids Processing Center in Ludwigshafen, Germany. The facility enables pilot-scale catalyst synthesis and new solids processing technologies, accelerating global customer access to innovations. It strengthens BASF’s R&D capabilities, supporting the rapid development of sustainable processes for the green transformation.

- In November 2024, Clariant launched its Plus series syngas catalysts, including ReforMax LDP Plus, ShiftMax 217 Plus, and AmoMax 10 Plus. Designed as drop-in solutions, the catalysts enhance plant economics and reduce carbon emissions, with commercial use confirming their effectiveness and sustainability benefits across syngas applications.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the catalyst aging testing market based on the below-mentioned segments:

Global Catalyst Aging Testing Market, By Material Type

- Thermal Aging Testing

- Chemical

- Mechanical

- Combined

Global Catalyst Aging Testing Market, By Application

- Catalyst Aging

- Catalyst Ageing Cycle Development

- After-treatment Efficiency Measurement

- Catalyst Light-off Evaluation

- Dynamic Cycle Evaluation

Global Catalyst Aging Testing Market, By End-Use

- Automotive

- Petrochemicals

- Chemicals

- Pharmaceuticals

- Environmental

- Others

Global Catalyst Aging Testing Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.How do stringent emission regulations impact the demand for catalyst aging testing services globally?Stringent emission regulations, such as Euro 7, compel industries to validate catalyst durability through rigorous aging tests, ensuring long-term compliance. This regulatory pressure is the primary driver of sustained global demand for catalyst aging testing services.

-

2.What are the latest innovations in catalyst aging testing methodologies and equipment?Recent innovations include AI-driven predictive analytics for forecasting catalyst lifespan with over 30% greater accuracy, operando channel flow cells with ICP-MS for real-time dissolution monitoring, parallel 10-fold reactors enabling simultaneous high-throughput aging tests, and high-pressure reactors simulating years of thermal degradation in weeks.

-

3.How are advanced analytical techniques, like spectroscopy and thermal analysis, shaping market trends?Advanced analytical techniques like spectroscopy and thermal analysis are shaping market trends by enabling precise, real-time catalyst degradation monitoring. This drives demand for sophisticated testing services, projected to reach $22.94 billion by 2033, by providing deeper insights into catalyst structure-performance relationships

-

4.What role do government policies and environmental regulations play in market adoption and growth?Government policies and environmental regulations are the primary catalysts for market adoption, mandating stringent emissions compliance. This regulatory enforcement compels industries to conduct rigorous catalyst aging tests, ensuring sustained performance and driving market growth.

-

5.How are emerging economies contributing to the expansion of the catalyst aging testing market?Emerging economies, particularly in Asia-Pacific and Latin America, are driving market expansion through rapid industrialization and expanding manufacturing bases. Countries like China, India, Brazil, and Malaysia are witnessing increased demand for catalyst aging testing due to growing petrochemical, automotive, and biofuels sectors adopting advanced testing technologies to meet international standards.

-

6.What economic factors, such as R&D investments and production costs, influence market growth?Increasing R&D investments enable advanced testing technologies and predictive models, expanding market capabilities. Simultaneously, high production costs for sophisticated equipment can restrain adoption, particularly among smaller enterprises with limited capital budgets.

-

7.How are digital and automated testing solutions transforming efficiency and accuracy in catalyst aging testing?Digital and automated solutions transform catalyst aging testing by enabling AI-driven predictive modelling and high-throughput parallel reactors. This automation accelerates testing cycles, improves accuracy by over 30%, reduces human error, and ensures consistent, reproducible results across complex degradation protocols.

Need help to buy this report?