Global Cardiac Output Monitoring Device Market Size, and Share, By Product Type (Standalone Devices, Integrated Systems, and Wearable Devices), By Technology (Invasive Monitoring, Minimally Invasive Monitoring, and Non-Invasive Monitoring), By Application (Cardiac Surgery, Critical Care, Emergency Medicine, Anesthesia, and Postoperative Care), By End Use (Hospitals, Ambulatory Surgical Centers, Home Care Settings, and Specialty Clinics), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: HealthcareGlobal Cardiac Output Monitoring Device Market Insights Forecasts to 2035

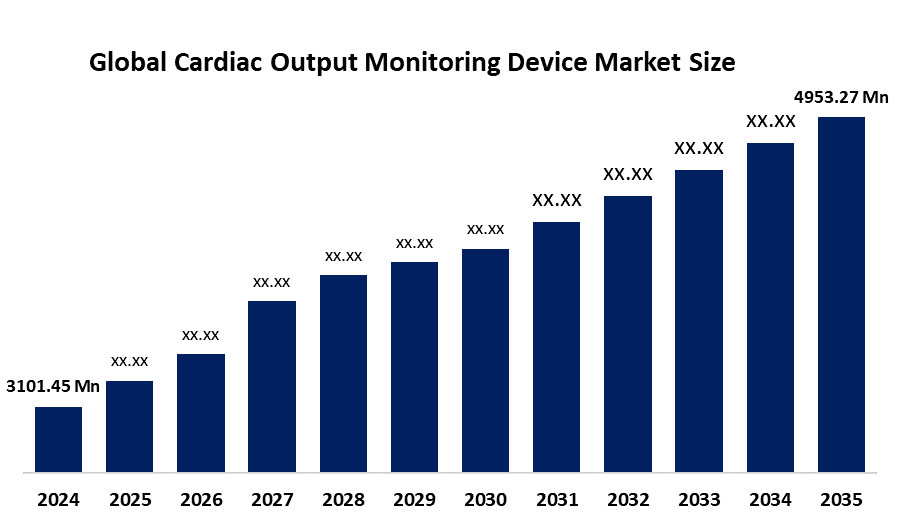

- The Global Cardiac Output Monitoring Device Market Size Was Estimated at USD 3101.45 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 4.35% from 2025 to 2035

- The Worldwide Cardiac Output Monitoring Device Market Size is Expected to Reach USD 4953.27 Million by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, The Global Cardiac Output Monitoring Device Market Size was worth around USD 3101.45 Million in 2024 and is predicted to grow to around USD 4953.27 Million by 2035 with a compound annual growth rate (CAGR) of 4.35% from 2025 to 2035. The cardiac output monitoring device market is expanding due to increasing cardiovascular disease prevalence, a growing elderly population, and demand for minimally invasive, real-time monitoring. Advancements in non-invasive sensors and rising healthcare investments in emerging markets further boost adoption.

Market Overview

The global cardiac output monitoring device market refers to medical technologies used to measure the volume of blood the heart pumps per minute, a critical parameter in assessing cardiovascular performance and guiding treatment decisions. The devices find application in critical care environments, which include intensive care units, operating rooms and emergency departments, to treat patients who suffer from cardiovascular diseases, sepsis and heart failure. In December 2025, the U.S. Medicare updated payment policies to expand home cardiac monitoring, simplifying billing and improving reimbursement for remote care. This move is expected to transform the remote patient monitoring market, driving broader adoption of home-based cardiac monitoring solutions nationwide.

The market is growing steadily because cardiovascular diseases, which result in approximately 17.9 million annual deaths worldwide according to the World Health Organization, create increasing demand for medical services. Increasing demand for minimally invasive and non-invasive monitoring technologies is a key driver, improving patient safety and reducing complications. The development of wearable devices and continuous monitoring systems results in better clinical results for patients. The business will find new opportunities through its AI system and remote patient monitoring system, and through its development of healthcare services in developing nations. In November 2024, SeeMedX submitted a 510(k) to the FDA for its non-invasive cardiac monitoring device, providing real-time insights into cardiac output and fluid status. Designed to optimize heart failure care, it enables earlier detection, faster clinical decisions, improved patient comfort, and streamlined hospital workflows.

Report Coverage

This research report categorizes the cardiac output monitoring device market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the cardiac output monitoring device market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the cardiac output monitoring device market.

Global Cardiac Output Monitoring Device Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 3101.45 Million |

| Forecast Period: | 2024-2035 |

| Forecast Period CAGR 2024-2035 : | CAGR of 4.35% |

| 2035 Value Projection: | USD 4953.27 Million |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 95 |

| Segments covered: | By Product Type, By Technology |

| Companies covered:: | Edwards Lifesciences Corporation, Koninklijke Philips N.V., GE HealthCare Technologies Inc., Medtronic, Abbott Laboratories, ICU Medical, Inc., Uscom Ltd, Osypka Medical GmbH, Deltex Medical Group plc, LiDCO Group plc, Getinge AB, BioTelemetry, Inc., CNSystems Medizintechnik GmbH, Baxter International, Inc., Others, and |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The demand for global cardiac output monitoring devices grows because of two factors, which include the increasing spread of cardiovascular diseases that cause 32% of worldwide deaths and the need for precise hemodynamic measurement during critical surgical procedures. Patient safety and clinical efficiency improve when healthcare systems implement both minimally invasive and non-invasive monitoring solutions. The demand for healthcare services increases because emerging regions build more intensive care unit facilities, and the worldwide geriatric population will reach 1.5 billion people by 2050. Continuous monitoring together with wearable cardiac output devices creates new possibilities for obtaining precise data in real time. The market continues to grow because of increased healthcare spending, government expenditures, and public understanding of the importance of early diagnosis.

Restraining Factors

The market development faces obstacles because of expensive equipment requirements, insufficient reimbursement options, and the necessity for specialized medical training. The market expansion faces challenges because developing regions show lower adoption rates, which result from both affordable monitoring solutions and users' worries about device invasiveness and maintenance requirements.

Market Segmentation

The cardiac output monitoring device market share is classified into product type, technology application, and end use.

- The standalone devices segment dominated the market in 2024, approximately 48% and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the cardiac output monitoring device market is divided into standalone devices, integrated systems, and wearable devices. Among these, the standalone devices segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment dominance is attributed to its widespread adoption in hospitals, ICUs, and surgical settings. Offering precise, real-time hemodynamic measurements, these devices are preferred for critical patient management. Their ease of integration, reliability, and compatibility with existing hospital systems further reinforced their leading market position and sustained growth.

- The minimally invasive monitoring segment accounted for the largest share in 2024, approximately 42% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the technology, the cardiac output monitoring device market is divided into invasive monitoring, minimally invasive monitoring, and non-invasive monitoring. Among these, the minimally invasive monitoring segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The minimally invasive monitoring segment growth is driven by rising demand for safer, accurate hemodynamic assessments. These devices reduce patient risk compared to fully invasive methods, enhance clinical efficiency, and enable real-time monitoring. Increasing adoption in ICUs, cardiac surgeries, and critical care settings further accelerated market expansion.

- The critical care segment dominated the market in 2024, approximately 36% and is projected to grow at a substantial CAGR during the forecast period.

Based on the application, the cardiac output monitoring device market is divided into cardiac surgery, critical care, emergency medicine, anesthesia, and postoperative care. Among these, the critical care segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The critical care segment led the market due to high demand for precise, real-time hemodynamic monitoring in ICUs. Growing prevalence of cardiovascular diseases, increasing critical care admissions, and the need for accurate patient management during complex conditions reinforced its leading position, driving significant market growth and adoption.

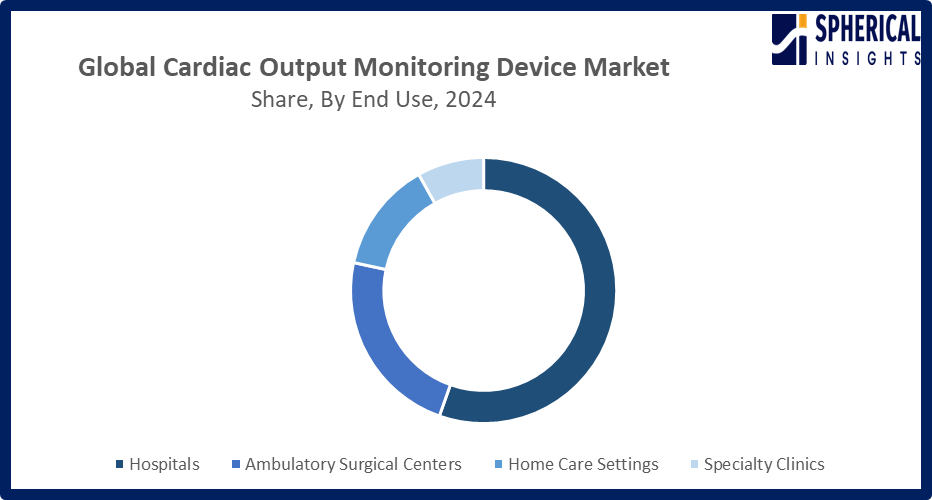

- The hospitals segment accounted for the highest market revenue in 2024, approximately 55% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end use, the cardiac output monitoring device market is divided into hospitals, ambulatory surgical centers, home care settings, and specialty clinics. Among these, the hospitals segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The hospitals segment growth in the market is driven by the need for continuous, accurate patient monitoring across ICUs, cardiac surgery, and critical care units. Rising cardiovascular disease prevalence, expanding hospital infrastructure, and increasing adoption of advanced monitoring technologies further fueled demand, positioning hospitals as the primary end-users.

Get more details on this report -

Regional Segment Analysis of the Cardiac Output Monitoring Device Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the cardiac output monitoring device market over the predicted timeframe.

North America is anticipated to hold the 45% share of the cardiac output monitoring device market over the predicted timeframe. The region's growth is driven primarily by the United States. Factors include advanced healthcare infrastructure, high adoption of minimally invasive and wearable monitoring technologies, and significant healthcare spending exceeding $4 trillion annually. The region also benefits from well-established reimbursement policies, extensive ICU and cardiac care facilities, and a strong presence of leading device manufacturers. Growing cardiovascular disease prevalence and increasing geriatric population further reinforce North America’s dominant market position and sustained growth. In October 2024, Senator Duckworth secured $192,000 in federal funding for Pinckneyville Community Hospital. The grant will upgrade cardiac monitoring and vital signs systems across the Emergency, Oncology, Surgical, and medical units, replacing outdated devices and enhancing patient care with advanced, innovative technology.

Asia Pacific is expected to grow at a rapid CAGR in the cardiac output monitoring device market during the forecast period. The region is rapidly growing in the cardiac output monitoring device market, led by China and India. Growth is driven by expanding healthcare infrastructure, rising cardiovascular disease prevalence, increasing government healthcare investments, and growing awareness of advanced monitoring technologies. Additionally, the region’s large patient population and rising adoption of noninvasive and wearable cardiac monitoring devices support market expansion, making Asia Pacific a fast-growing and attractive market for manufacturers.

Europe, led by Germany and the UK, is witnessing steady growth in the cardiac output monitoring device market due to advanced healthcare infrastructure, high adoption of innovative medical technologies, and supportive reimbursement policies. Increasing prevalence of cardiovascular diseases, rising geriatric population, and growing focus on critical care and postoperative monitoring further drive demand for accurate, minimally invasive, and continuous cardiac output monitoring solutions across hospitals and healthcare facilities.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the cardiac output monitoring device market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Edwards Lifesciences Corporation

- Koninklijke Philips N.V.

- GE HealthCare Technologies Inc.

- Medtronic

- Abbott Laboratories

- ICU Medical, Inc.

- Uscom Ltd

- Osypka Medical GmbH

- Deltex Medical Group plc

- LiDCO Group plc

- Getinge AB

- BioTelemetry, Inc.

- CNSystems Medizintechnik GmbH

- Baxter International, Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026, the FDA granted Noah Labs a breakthrough device designation for Vox, an AI-powered RPM tool analyzing voice recordings to detect worsening heart failure. Validated in multiple clinical trials, Vox offers noninvasive early detection, expediting interventions and marking a shift from traditional blood pressure–based monitoring systems.

- In October 2025, GE HealthCare received the CE mark for its Carevance patient monitor in Europe. The system offers scalable, cost-effective cardiac monitoring with advanced Cardiac Output Insights, enabling real-time hemodynamic visualization, improved workflow efficiency, and noninvasive monitoring to support clinicians amid staffing and patient care challenges.

- In September 2025, Philips launched its Telemetry Monitor 5500, a cardiac monitoring platform addressing staff shortages and alarm management. The wearable, touchscreen-enabled system supports patient mobility, scalable high-acuity monitoring, filtered alarms, and data-driven insights, enhancing hospital workflow efficiency, care coordination, and overall patient surveillance across healthcare networks.

- In July 2025, the FDA granted 510(k) clearance for Cardiosense’s wearable CardioTag, capturing ECG, SCG, and PPG signals for noninvasive cardiac monitoring. AI-integrated trials aim to measure cardiac timing and pulmonary capillary wedge pressure, potentially improving advanced heart failure management with accuracy comparable to implantable sensors.

- In April 2025, Medtronic partnered with Retia Medical to distribute the Argos cardiac output monitor in the U.S. The device delivers accurate hemodynamic data, enabling clinicians to detect circulatory shock early, support timely interventions, and improve outcomes for high-risk surgical and critically ill patients.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the cardiac output monitoring device market based on the below-mentioned segments:

Global Cardiac Output Monitoring Device Market, By Product Type

- Standalone Devices

- Integrated Systems

- Wearable Devices

Global Cardiac Output Monitoring Device Market, By Technology

- Invasive Monitoring

- Minimally Invasive Monitoring

- Non-Invasive Monitoring

Global Cardiac Output Monitoring Device Market, By Application

- Cardiac Surgery

- Critical Care

- Emergency Medicine

- Anesthesia

- Postoperative Care

Global Cardiac Output Monitoring Device Market, By End Use

- Hospitals

- Ambulatory Surgical Centers

- Home Care Settings

- Specialty Clinics

Global Cardiac Output Monitoring Device Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.What role do technological innovations, such as wearable and minimally invasive devices, play in market growth?Technological innovations like wearable and minimally invasive cardiac output monitoring devices enhance patient safety, enable continuous real-time data, improve clinical efficiency, and expand adoption across critical care and surgical settings, driving significant market growth.

-

2.What trends in remote patient monitoring are influencing cardiac output device adoption?Remote monitoring trends include real-time data transmission, AI-driven analytics, and patient engagement tools. These reduce hospital visits by 40% and improve early intervention for heart failure patients.

-

3.How does aging population growth affect the market for cardiac output monitoring devices?An aging global population increases demand for cardiac output monitoring devices, as cardiovascular risk rises with age; adults over 65 are projected to reach 1.5 billion by 2050, driving expanded device adoption in clinical care.

-

4.What economic factors, including healthcare spending and reimbursement policies, are shaping the market?Rising global healthcare spending (10% of GDP in the US, 2023) and value-based reimbursement policies (linking 60% of payments to outcomes) drive the adoption of cost-effective, non-invasive cardiac monitors.

-

5.How are AI and data analytics enhancing cardiac output monitoring accuracy and usability?AI and data analytics enhance cardiac output monitoring by improving signal interpretation, predictive insights, and decision support, with AI‑enabled devices projected to boost diagnostic accuracy by 20-30% and streamline clinical workflows globally.

-

6.What future innovations could redefine the cardiac output monitoring device market over the next decade?By 2030, AI-integrated bioimpedance wearables could achieve 92% accuracy versus pulmonary artery catheters, reducing ICU costs by $2,000 per patient and enabling continuous home monitoring for 40% of heart failure cases.

-

7.How do government regulations and CE/FDA approvals impact market growth?Government regulations and CE/FDA approvals ensure device safety and efficacy, boosting market confidence and adoption; approximately 70% of new cardiac output monitoring devices in 2024 achieved regulatory clearance, accelerating global market growth.

Need help to buy this report?