Global Bulk Drug Intermediates Market Size, and Share, By Type (Active Pharmaceutical Ingredients (APIs) Intermediates, Key Starting Materials (KSMs), and Others), By Application (Cardiovascular Drugs, Antibiotics, Analgesics & Anti-inflammatory Drugs, Oncology Drugs, and Other Therapeutics), By End-User (Pharmaceutical Companies, Contract Manufacturing Organizations (CMOs), and Research & Development Organizations), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Chemicals & MaterialsGlobal Bulk Drug Intermediates Market Insights Forecasts to 2035

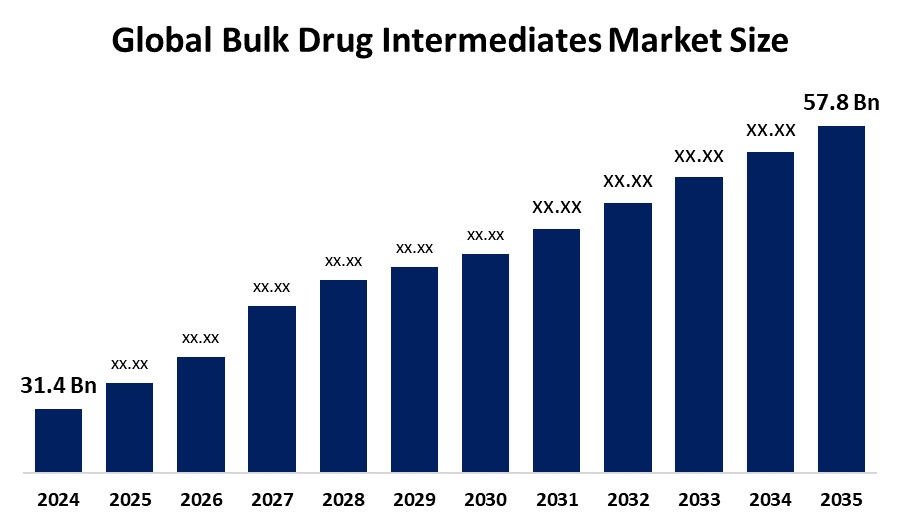

- The Global Bulk Drug Intermediates Market Size Was Estimated at USD 31.4 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 5.7% from 2025 to 2035

- The Worldwide Bulk Drug Intermediates Market Size is Expected to Reach USD 57.8 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global bulk drug intermediates market size was worth around USD 31.4 billion in 2024 and is predicted to grow to around USD 57.8 billion by 2035 with a compound annual growth rate (CAGR) of 5.7% from 2025 to 2035. The bulk drug intermediates market is expanding due to growing demand for APIs, higher chronic disease prevalence, and increased outsourcing to CDMOs, alongside accelerated generic drug manufacturing and significant investments in pharmaceutical R&D supporting market growth.

Report Coverage

This research report categorizes the bulk drug intermediates market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the bulk drug intermediates market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the bulk drug intermediates market.

Global Bulk Drug Intermediates Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 31.4 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 5.7% |

| 2035 Value Projection: | USD 57.8 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 240 |

| Tables, Charts & Figures: | 108 |

| Segments covered: | By Type, By Application, By End-User |

| Pitfalls & Challenges: | COVID-19 Impact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global bulk drug intermediates sector is mainly propelled by increasing demand for generic and specialty pharmaceuticals, growth in pharmaceutical research and development, and greater reliance on contract manufacturing organizations (CMOs). The rising incidence of chronic illnesses, including cardiovascular diseases, diabetes, and cancer, drives higher API production, thereby enhancing consumption of intermediates. Innovations in chemical synthesis, continuous-flow technologies, and sustainable green chemistry boost production efficiency, yields, and cost-effectiveness. Moreover, emerging Asia-Pacific markets, supported by expanding healthcare systems and favorable regulatory policies, present substantial growth potential. Increased funding in personalized medicine and novel therapeutics further fuels global demand for high-quality bulk drug intermediates.

Restraining Factors

The bulk drug intermediates market is constrained by strict regulations, lengthy approval procedures, and high compliance costs, especially in North America and Europe. Fluctuating raw material prices and supply chain disruptions hinder production efficiency. Environmental challenges associated with chemical synthesis further restrict expansion, collectively slowing market growth and limiting the sectors full potential.

Restraining Factors

The bulk drug intermediates market is constrained by strict regulations, lengthy approval procedures, and high compliance costs, particularly in North America and Europe. Fluctuating raw material prices and supply chain disruptions further hinder production efficiency. Additionally, environmental concerns associated with chemical synthesis restrict market expansion. Collectively, these factors slow overall market growth and limit the sector’s full potential.

Market Segmentation

The active pharmaceutical ingredient (API) intermediates segment dominated the market in 2024, accounting for approximately 48%, and is projected to grow at a substantial CAGR during the forecast period. Based on type, the market is categorized into API intermediates, key starting materials (KSMs), and others. Among these, API intermediates held the largest share due to rising demand for generic and specialty drugs, increasing prevalence of chronic diseases, and expanding pharmaceutical R&D activities. Large-scale API production, along with technological advancements in chemical synthesis and continuous-flow processes, has improved efficiency, yield, and cost-effectiveness, thereby driving global market growth.

The antibiotics segment accounted for the largest share in 2024, approximately 37%, and is anticipated to grow at a significant CAGR during the forecast period. Based on application, the market is segmented into cardiovascular drugs, antibiotics, analgesics & anti-inflammatory drugs, oncology drugs, and other therapeutics. The dominance of the antibiotics segment is attributed to the increasing prevalence of infectious diseases, growing demand for generic antibiotics, and improved healthcare access worldwide. Furthermore, the expansion of large-scale antibiotic production and advancements in intermediates synthesis have enhanced efficiency and output, supporting strong market growth.

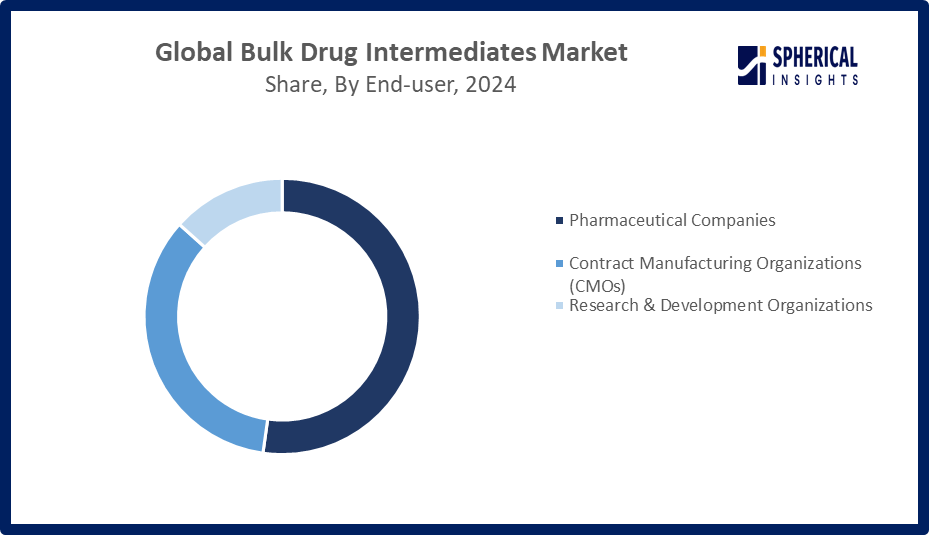

The pharmaceutical companies segment accounted for the highest market revenue in 2024, approximately 52%, and is expected to grow at a significant CAGR during the forecast period. Based on end-user, the market is divided into pharmaceutical companies, contract manufacturing organizations (CMOs), and research & development organizations. The growth of this segment is driven by increasing in-house production of APIs and intermediates for generics and specialty drugs. Additionally, rising chronic disease prevalence, increased R&D investments, and a focus on cost-efficient large-scale manufacturing have strengthened demand, positioning pharmaceutical companies as the leading consumers of bulk drug intermediates globally.

Get more details on this report -

Regional Segment Analysis of the Bulk Drug Intermediates Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

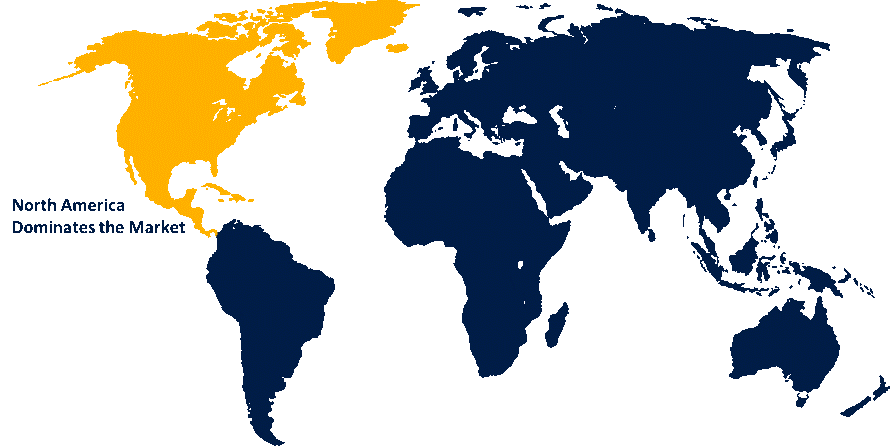

North America is anticipated to hold the largest share of the bulk drug intermediates market over the predicted timeframe.

Get more details on this report -

North America is anticipated to hold the 42% share of the bulk drug intermediates market over the predicted timeframe. The bulk drug intermediates market in North America is its largest market segment because of the United States dominance. The region benefits from a well-established pharmaceutical industry, high R&D investments, and stringent regulatory standards that emphasize quality and safety. The market experiences strong growth because of high demand for generic and specialty drugs, which exists together with advanced manufacturing facilities and ongoing improvements in chemical synthesis and API production. The North American market maintains its leading position because of companies that choose to outsource and work together with contract manufacturing organizations who provide their services. In the U.S., the FDA issued interim guidance in January 2025 for outsourcing facilities using bulk drug substances ahead of the official 503B bulks list. Meanwhile, the FTC and HHS launched a February 2024 inquiry into how drug supply middlemens contracting practices affect generic drug shortages.

Asia Pacific is expected to grow at a rapid CAGR in the bulk drug intermediates market during the forecast period. The bulk drug intermediates market in Asia-Pacific is rapidly growing in India and China, which leads the region. The pharmaceutical sector in the region expands its production capabilities while government programs support local production through budget-friendly manufacturing solutions. The region experiences rapid growth because of increasing global demand for generic drugs and the rising tendency to outsource API and intermediate production to local manufacturers. The Asia-Pacific region is becoming a fast-developing market center through its investments in research and development, together with its investments to build large-scale production facilities. In February 2026, the Indian government reported progress under its PLI Scheme for Bulk Drugs, with rs4,814 crore invested to boost domestic KSM, DI, and API production. The initiative created capacities for 26 critical drugs, generated rs2,720 crore in sales, including rs528 crore exports, and helped avoid imports worth rs2,192 crore.

The bulk drug intermediates market in Europe experiences steady growth. Market expansion in the region derives from three factors, which include a strong generics sector, advanced pharmaceutical manufacturing facilities, and high-quality regulatory requirements. The European market for intermediates production maintains its status as a major international force because research investments, together with high specialty drug demand and contract manufacturing partnerships, drive market expansion.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the bulk drug intermediates market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- BASF SE

- Evonik Industries AG

- Lonza Group AG

- Aurobindo Pharma Ltd.

- Divis Laboratories Limited

- Cambrex Corporation

- WuXi AppTec

- Aarti Industries Ltd.

- Dishman Group

- Merck KGaA

- Green Vision Life Sciences

- Chiracon GmbH

- Aceto Corporation

- Vertellus Holdings LLC

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026, Cambrex completed initial engineering studies for its new USD 120 million API manufacturing plant in Charles City, Iowa, adding 140,000 litre capacity and boosting production by 20%. In Europe, a USD 30 million expansion at Milan enhances R&D and production capabilities, supporting growing demand for CDMO services.

- In December 2025, India intensified efforts for pharmaceutical self-reliance by reopening the sixth application round under its PLI scheme for bulk drugs on November 26. The initiative targets critical APIs like Meropenem and Ritonavir, aiming to expand domestic manufacturing capacity, strengthen the pharmaceutical ecosystem, and reduce dependence on imported raw materials.

- In October 2025, Cambrex announced a USD 120 million investment to expand its U.S. operations, boosting large-scale manufacturing at its Charles City, Iowa, facility by 40% to nearly one million liters. The site produces diverse APIs, including highly potent molecules and controlled substances, strengthening Cambrexs role in peptide therapeutics.

- In August 2025, India’s pharmaceutical PLI schemes exceeded expectations, attracting RS 4,709 crore for bulk drugs and R 38,543 crore for broader pharma initiatives. The schemes boosted production of KSMs, APIs, and intermediates, generated R 1,962 crore in sales, and reduced import dependence, though reliance on China for raw materials persists.

- In August 2024, Indias Ministry of Chemicals and Fertilizers announced the completion of 32 projects under the PLI Scheme for Key Starting Materials, Drug Intermediates, and APIs, totaling 56,679 MT year. With a Rs 6,940 crore outlay, the scheme aims to boost domestic production, reduce imports, and enhance supply chain resilience.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the bulk drug intermediates market based on the below-mentioned segments:

Global Bulk Drug Intermediates Market, By Types

- Active Pharmaceutical Ingredients (APIs) Intermediates

- Key Starting Materials (KSMs)

- Others

Global Bulk Drug Intermediates Market, By Application

- Cardiovascular Drugs

- Antibiotics

- Analgesics & Anti-inflammatory Drugs

- Oncology Drugs

- Other Therapeutics

Global Bulk Drug Intermediates Market, By End-User

- Pharmaceutical Companies

- Contract Manufacturing Organizations (CMOs)

- Research & Development Organizations

Global Bulk Drug Intermediates Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What role do technological innovations in chemical synthesis play in enhancing bulk drug intermediate production efficiency?Technological innovations in chemical synthesis, such as continuous-flow processes and green chemistry, enhance bulk drug intermediate efficiency by 20-30%, reduce waste, and accelerate production, with 45% of manufacturers adopting these methods globally.

-

2. What economic factors are affecting investment in bulk drug intermediates manufacturing?Economic factors affecting investment in bulk drug intermediates include high capital expenditure, raw material price volatility, and regulatory costs, with 52% of manufacturers citing cost constraints, while global pharmaceutical investment reached USD 152 billion in 2025.

-

3. Which regulatory changes are impacting the production and approval of bulk drug intermediates?Regulatory changes impacting bulk drug intermediates include stricter CGMP compliance and environmental standards, with 60% of manufacturers reporting increased audit requirements and 25% facing longer approval timelines, raising compliance costs and affecting production schedules.

-

4. What is the impact of government incentive schemes, such as PLI, on the domestic production of intermediates?Government incentive schemes like PLI significantly boost domestic intermediate production by increasing local output by 25-35%, reducing import dependence, and attracting investment. In markets like India, 50+ companies expanded API/intermediate capacity under PLI, enhancing competitiveness and supply‑chain resilience.

-

5. What innovations in oral and biologic drug delivery are affecting intermediate demand?Innovations in oral and biologic drug delivery, including enhanced oral formulations and permeability technologies, are expanding demand for complex intermediates, as the oral biologics market is projected to grow sharply through 2030, increasing production needs for advanced APIs and intermediates used in these patient‑friendly therapies.

-

6. How are environmental sustainability initiatives influencing manufacturing practices in the bulk drug intermediates sector?Environmental sustainability initiatives are pushing manufacturers to adopt greener processes, reducing solvent and waste by up to 40%, with 55% of firms investing in eco‑friendly technologies to meet stricter emission and effluent standards.

-

7. What role does investment in personalized medicine play in boosting bulk drug intermediate demand?Investment in personalized medicine drives demand for specialized bulk drug intermediates, as tailored therapies require unique APIs and precursors; global spending on personalized drugs reached USD 120 billion in 2025, boosting intermediate consumption by 15% annually.

Need help to buy this report?