Global Bio Polylactic Acid Market Size, Share, By Product Type (PLA Resins, PLA Films, PLA Foams, PLA Blends, and PLA Fibers), By Application (Packaging, Medical Healthcare, Automotive, Agriculture, and Electronics Consumer Products), By End User (Food Beverage, Healthcare, Automotive Transportation, Consumer Goods, Agriculture, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Bio Polylactic Acid Market Insights Forecasts to 2035

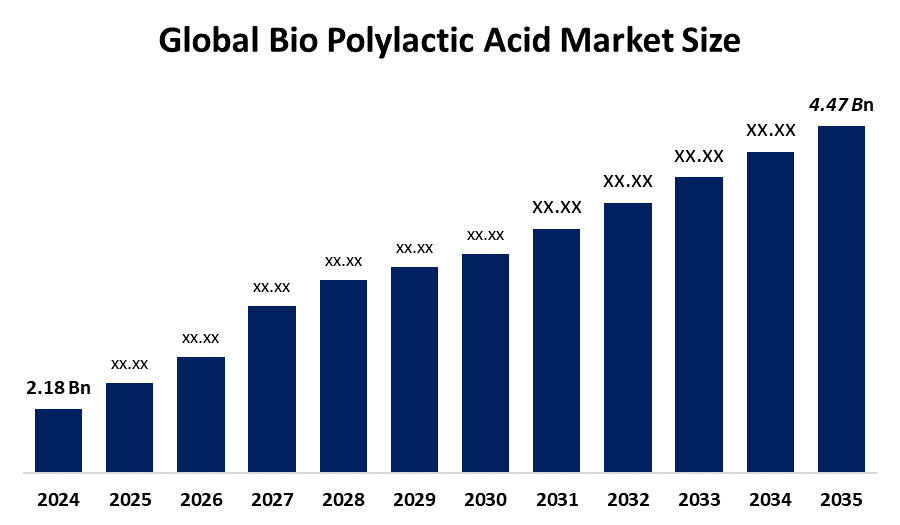

- The Global Bio Polylactic Acid Market Size Was Estimated at USD 2.18 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 7.17% from 2025 to 2035

- The Worldwide Bio Polylactic Acid Market Size is Expected to Reach USD 4.67 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global bio polylactic acid market size was worth around USD 2.18 billion in 2024 and is predicted to grow to around USD 4.67 billion by 2035 with a compound annual growth rate (CAGR) of 7.17% from 2025 to 2035. Global advancements in fermentation techniques, advanced bioprocessing and continuous manufacturing, innovations in polymer formulation enhance heat resistance, integration with recycling and composting technologies are all driving opportunities in the bio polylactic acid market.

Market Overview

The bio polylactic acid market refers to the global industry involved in the production, distribution, and application of PLA, which is a biodegradable bio based polymer that derives from renewable resources such as corn starch and sugarcane. The market encompasses all activities that include PLA production, compounding, processing, and delivery to various sectors, including packaging, textiles, automotive, electronics, and medical devices. The market key opportunities arise from growing consumer demand for sustainable materials, increasing public knowledge about plastic pollution and the development of advanced bioplastics which can match the performance of traditional plastics. The industry experiences greater material adoption because technological advancements decrease production expenses while delivering superior material attributes.

The government establishes essential economic incentives through its implementation of policies that support bio-based production and its provision of subsidies while enforcing tougher regulations to control single-use plastic products, which leads to higher industry investment in PLA technology. For instance, in December 2022, the U.S. Department of Agriculture (USDA) announced an investment of USD 9.5 million to scale up biobased product manufacturing, including biodegradable plastics like PLA. The funding enables research and development activities, together with the commercial launch of products made from agricultural feedstocks, which help decrease petroleum-based plastic dependency.

In December 2022, the Indian PIB data shows that enforcement actions resulted in the confiscation of 775577 kilograms of plastic materials and penalties amounting to INR 5.81 crore, which demonstrates strong enforcement activities. The enforcement activities create a greater need for PLA because it serves as a compliant solution.

Report Coverage

This research report categorizes the bio polylactic acid market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the bio polylactic acid market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the bio polylactic acid market.

Global Bio Polylactic Acid Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 2.18 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 7.17% |

| 2035 Value Projection: | USD 4.67 Billion |

| Historical Data for: | 2021-2023 |

| No. of Pages: | 220 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Product Type, By Application |

| Companies covered:: | NatureWorks LLC, TotalEnergies Corbion PLA, Futerro SA, BASF SE, Zhejiang Hisun Biomaterials Co., Ltd., COFCO Biotechnology Col, Ltd., Mitsubishi Chemical Group Corporation, Toray Industries, Inc., Danimer Scientific, Evonik Industries AG, Unitika Ltd., Synbra Technology B.V., Anhui BBCA Biochemical Co., Ltd., Shanghai Tong-Jie-Liang Biomaterials Co., Ltd., Jilin COFCO Biomaterials Co., Ltd., Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

Rapid technological innovation is one of the main drivers of the bio polylactic acid market's growth. Growing environmental concerns and the urgent need to reduce reliance on conventional plastics which is the main factors driving the market for bio polylactic acid. The demand for sustainable biodegradable products has increased because consumers now prefer these items across packaging, textiles, and medical sectors. The technological progress that encompasses fermentation methods, polymer processing techniques, and material enhancement methods results in better PLA performance and lower production expenses. The combination of supportive government policies and financial incentives with single-use plastic bans creates an environment that promotes business adoption of these solutions. The market growth process receives additional momentum through the expanding use of products in automotive and electronics, and 3D printing, together with the rising corporate sustainability efforts.

In September 2022, the U.S. government launched the National Biotechnology and Biomanufacturing Initiative through an Executive Order to increase domestic production of bio-based products which include bioplastics such as PLA. The initiative targets establishing operational solutions to scale innovations and creating efficient pathways for sustainable manufacturing growth.

Restraining Factors

High production and processing costs, limited availability of raw materials, lower thermal and mechanical properties, Inadequate recycling and industrial composting infrastructure market, strong competition from cheaper petroleum-based plastics, technological limitations in large-scale production, are the main factors restricting the bio polylactic acid market.

Market Segmentation

The bio polylactic acid market share is classified into product type, application, and end user.

- The PLA resins segment dominated the market in 2024, approximately 45%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the product type, the bio polylactic acid market is divided into PLA resins, PLA films, PLA foams, PLA blends, and PLA fibers. Among these, the PLA resins segment dominated the market in 2024, approximately 45%, and is projected to grow at a substantial CAGR during the forecast period. Serve as the primary raw material for producing films, foams, fibers, and blends, making them highly versatile, widespread use in packaging, medical devices, and consumer goods, technological advancements improving processability and cost-efficiency are driving the PLA resins industry.

- The packaging segment accounted for the largest share in 2024, approximately 58%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the bio polylactic acid market is divided into packaging, medical healthcare, automotive, agriculture, and electronics consumer products. Among these, the packaging segment accounted for the largest share in 2024, approximately 58%, and is anticipated to grow at a significant CAGR during the forecast period. Growing demand for sustainable, biodegradable alternatives is driving the packaging industry. Providing transparency, strength, and compostability, increasing environmental regulations, consumer awareness, and corporate sustainability initiatives are driving the packaging industry.

- The food beverage segment accounted for the highest market revenue in 2024, approximately 45%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the bio polylactic acid market is divided into food beverage, healthcare, automotive transportation, consumer goods, agriculture, and others. Among these, the food and beverage segment accounted for the highest market revenue in 2024, approximately 45%, and is anticipated to grow at a significant CAGR during the forecast period. Rising demand for eco-friendly packaging, provides biodegradability, safety for direct food contact, and versatility, increasing consumer preference for sustainable options, and stricter regulations on single-use plastics are bolstering the food and beverage market.

Regional Segment Analysis of the Bio Polylactic Acid Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

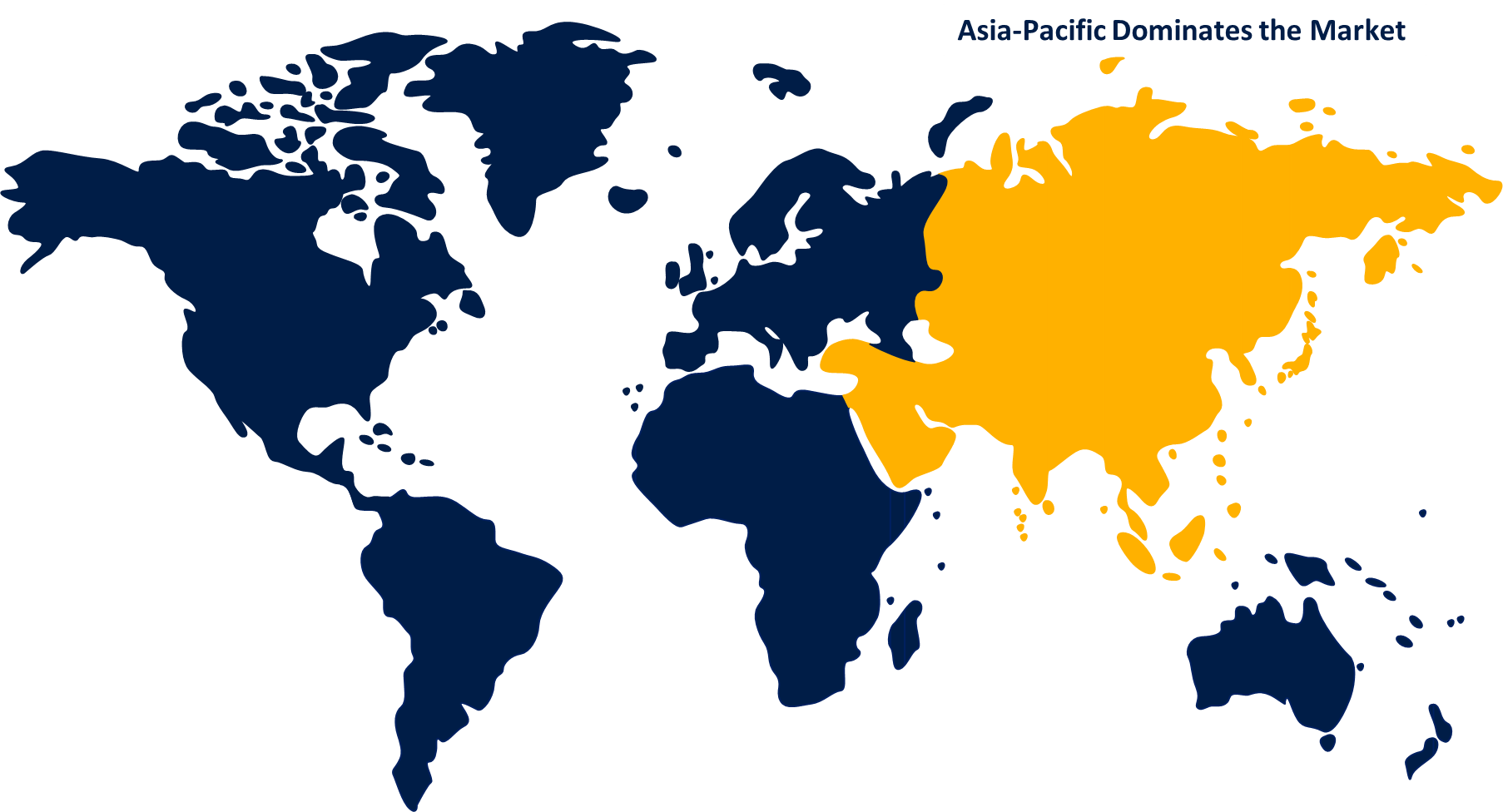

Asia Pacific is anticipated to hold the largest share of the bio polylactic acid market over the predicted timeframe.

Get more details on this report -

Asia Pacific is anticipated to hold the largest share of the bio polylactic acid market over the predicted timeframe. Strong government backing for strong manufacturing capabilities, abundant raw material availability, and growing demand for sustainable products are what propel the Asia Pacific. Countries such as China, India, and Japan benefit from easy access to renewable feedstocks like corn, sugarcane, and cassava, which lowers production costs. The region has experienced rapid growth in PLA usage because of increased industrial activities, urban development and consumer goods packaging sector expansion. The combination of government policies that support biodegradable plastic products and growing consumer environmental awareness has led to faster product adoption in the Asia Pacific.

Government initiatives include China’s BASP Initiative, Nov 2022, which promotes bio-based alternatives to plastics across industries, India’s Plastic Waste Management Amendment Rules, Aug 2021, banned single-use plastics and introduced EPR, pushing industries toward PLA adoption, and Japan’s USD 2 billion Supply Chain Diversification Program 2020, provide investment incentives for bio-based manufacturing.

North America is expected to grow at a rapid CAGR in the bio polylactic acid market during the forecast period. The market expansion receives support from major PLA manufacturers who operate in countries like the United States and Canada together with advanced production capabilities, established industrial composting, and recycling systems. The rising government rules about single-use plastics together with corporate sustainability commitments by businesses create a positive environment that drives companies to use PLA materials. The combination of rising environmental awareness among consumers, increased funding for bio-based material development, and new technologies drives economic expansion which makes North America an important player in the worldwide PLA market.

Government initiatives include the USDA’s BioPreferred Program, which certifies and promotes biobased products, including PLA bioplastics. The U.S. EPA’s National Strategy to Prevent Plastic Pollution, launched in November 2023, establishes a framework that encourages the broader adoption of bioplastics and compostable materials such as PLA. Additionally, in April 2021, Natural Resources Canada announced a USD 1 million investment under the Bioplastics Challenge to support the development of compostable bioplastics derived from biomass.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the bio polylactic acid market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- NatureWorks LLC

- TotalEnergies Corbion PLA

- Futerro SA

- BASF SE

- Zhejiang Hisun Biomaterials Co., Ltd.

- COFCO Biotechnology Col, Ltd.

- Mitsubishi Chemical Group Corporation

- Toray Industries, Inc.

- Danimer Scientific

- Evonik Industries AG

- Unitika Ltd.

- Synbra Technology B.V.

- Anhui BBCA Biochemical Co., Ltd.

- Shanghai Tong-Jie-Liang Biomaterials Co., Ltd.

- Jilin COFCO Biomaterials Co., Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In February 2026, Balrampur Chini Mills Limited’s PLA division Balrampur Bioyug signed its first institutional order with the Lucknow Cantonment Board for a range of compostable PLA products, marking a commercial rollout of PLA products derived from renewable resources.

- In September 2025, Sulzer Management Ltd in collaboration with TripleW announced the launch of the world’s first PLA bioplastics made entirely from food waste, transitioning the technology from pilot to scalable production.

- In May 2025, Balrampur Chini Mills launched Balrampur Bioyug, India’s first industrial scale PLA brand, tied to an integrated facility in Uttar Pradesh with substantial production capacity.

- In April 2025, TotalEnergies Corbion partnered with Useon launch an expanded PLA foam technology, an industrially compostable alternative to polystyrene using Luminy PLA.

- In October 2024, Praj Industries inaugurated India’s first demonstration facility for biopolymers, including PLA technology developed indigenously, capable of producing pilot quantities of PLA and showcasing industrial fermentation to polymer scale up.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the bio polylactic acid market based on the below-mentioned segments:

Global Bio Polylactic Acid Market, By Product Type

- PLA Resins

- PLA Films

- PLA Foams

- PLA Blends

- PLA Fibers

Global Bio Polylactic Acid Market, By Application

- Packaging

- Medical Healthcare

- Automotive

- Agriculture

- Electronics Consumer Products

Global Bio Polylactic Acid Market, By End User

- Food Beverage

- Healthcare

- Automotive Transportation

- Consumer Goods

- Agriculture

- Others

Global Bio Polylactic Acid Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What technologies are driving the bio-PLA market?The bio-PLA market is driven by technologies such as renewable feedstock fermentation, polymer blending, PLA compounding, 3D printing with PLA, and advanced biodegradable packaging solutions. Innovations in composite PLA materials and improved thermal/mechanical performance also support broader industrial adoption.

-

2. What types of PLA products are available?The market includes PLA resins, PLA films, PLA foams, PLA fibers, and PLA blends. PLA resins are the primary raw material for downstream applications, while films and foams are widely used in packaging, disposable products, and insulation. What is the role of PLA in sustainable packaging? PLA provides biodegradable, compostable, and eco-friendly alternatives to conventional plastics. It helps companies meet environmental regulations and corporate sustainability targets, particularly in food & beverage packaging, disposable tableware, and medical disposables.

-

3. How does government policy influence the PLA market?Government policies like single-use plastic bans, Extended Producer Responsibility regulations, and bio-based product incentives drive demand for PLA. In India, the Plastic Waste Management Amendment Rules and in the U.S., the USDA BioPreferred Program are examples of regulatory support.

-

4. Which industries benefit from PLA?Industries benefiting from PLA include food & beverage, healthcare, agriculture, automotive, consumer goods, and electronics. PLA is used for packaging, medical devices, biodegradable textiles, mulch films, and lightweight automotive components. What is the commercialization timeline for PLA? PLA is already commercially available globally, with large-scale production ongoing in Asia-Pacific, North America, and Europe. Market growth is expected to accelerate through the 2020’s, driven by rising environmental regulations, industrial adoption, and technological improvements in PLA production.

Need help to buy this report?