Global Battlefield Management Systems Market Size, Share, By Component (Hardware and Software, By System (Navigation & Mapping, Communication, Command & Control, Computing, and Others), By End Use (Army, Navy, Air Force, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Aerospace & DefenseGlobal Battlefield Management Systems Market Insights Forecasts to 2035

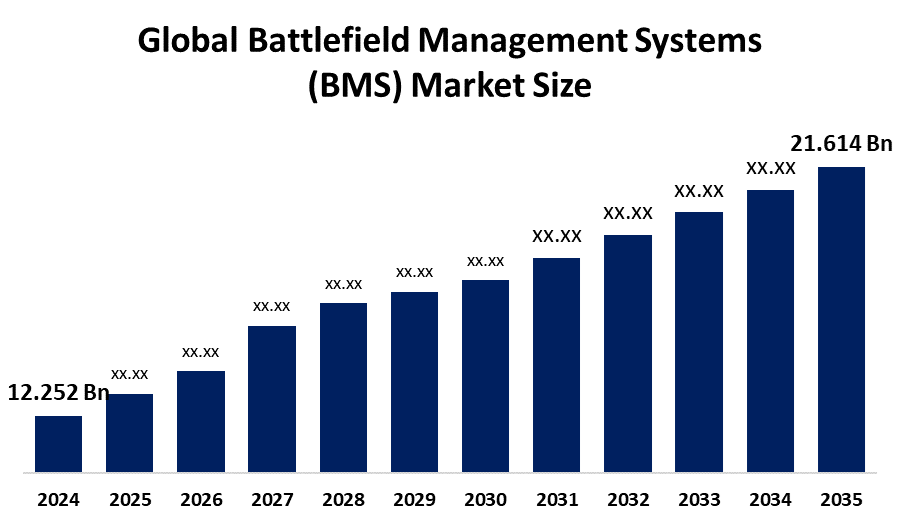

- The Global Battlefield Management Systems Size Was Estimated at USD 12.252 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 5.3% from 2025 to 2035

- The Worldwide Battlefield Management Systems Market Size is Expected to Reach USD 21.614 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global battlefield management systems market size was worth around USD 12.252 billion in 2024 and is predicted to grow to around USD 21.614 billion by 2035 with a compound annual growth rate (CAGR) of 5.3% from 2025 to 2035. Global advancements in AI, cloud computing, secure 5G communications, expansion of sensor integration, real-time situational awareness and network-centric warfare, increased defense digitization, and adoption of drone technology integration are all driving opportunities in the battlefield management systems market.

Market Overview

The battlefield management systems market refers to the global industry that develops integrated digital command and control solutions which provide military forces with real-time situational awareness, communication, and decision-making support. The systems include hardware and software together with communication networks which link soldiers, vehicles, drones, and command centers to create a complete operational view. The market serves land forces as its main application base while extending to joint operations which require air and naval coordination including technologies such as AI-driven analytics and cybersecurity frameworks and satellite communications. The market presents key opportunities through defense modernization programs which increase the budget for network centric warfare and demand for interoperability between allied forces and emerging technologies such as autonomous systems and edge computing.

Governments play a central and dominant role in this market as the main buyers who create regulations and supply funding for research and development activities. They drive demand through defense budgets while establishing standards and procurement policies which protect national security and technological sovereignty. For instance, in December 2022, Japan’s Ministry of Defense approved the Defense Buildup Program which will spend 43 trillion yen from FY2023 to FY2027 to increase defense spending until it reaches 2% of GDP, enabling battlefield management systems development which will serve as a primary market driver.

In June 2020, the U.S. Department of the Air Force allocated funding between USD 750 million and USD 950 million for the Advanced Battle Management System program which serves as a critical element of its next-generation battlefield management and command-and-control modernization effort under JADC2 system.

Report Coverage

This research report categorizes the battlefield management systems market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the battlefield management systems market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the battlefield management systems market.

Driving Factors

Rapid technological innovation is one of the main drivers of the battlefield management systems market's growth. Increasing need for real-time situational awareness and faster decision-making in modern warfare environments, which is the main factor driving the market for battlefield management systems. In this field, innovation and investment are driven by the global shift toward network-centric warfare, rising defense budgets in many countries, and increased modernization and digitization programs. Advancements in technologies such as artificial intelligence, data analytics, cloud and edge computing, and secure communication networks are also key drivers, enabling more efficient data processing and battlefield visibility, Additionally, government initiatives promote indigenous defense manufacturing and strategic partnerships with private sector players further propel the market growth.

In January 2025, Government of India launched SANJAY Battlefield Surveillance System to improve Indian army capacity to monitor situations in real-time. The system developed in partnership with Bharat Electronics Limited enables users to track multiple battlefield sensors which together create a comprehensive battlefield view that supports operational decision-making.

Restraining Factors

High development and deployment costs, military infrastructure and interoperability issues, concerns around cybersecurity vulnerabilities, risk of data breaches complexity of training personnel, and limited communication infrastructure in remote or hostile environments are the main factors restricting the battlefield management systems market.

Market Segmentation

The battlefield management systems market share is classified into component, system, and end user.

- The hardware segment dominated the market in 2024, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the component, the battlefield management systems market is divided into hardware and software. Among these, the hardware segment dominated the market in 2024, approximately 60%, and is projected to grow at a substantial CAGR during the forecast period. The growing need procurement of robust and ruggedized components, crucial for real-time data processing in hash combat environments, rising demand for sensor integration, drones, and communication devices is driving the hardware industry.

- The command & control segment accounted for the largest share in 2024, approximately 36%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the system, the battlefield management systems market is divided into navigation & mapping, communication, command & control, computing, and others. Among these, the command & control segment accounted for the largest share in 2024, approximately 36%, and is anticipated to grow at a significant CAGR during the forecast period. Primary framework for strategic planning and operational monitoring, integration of data from various sources, rising geopolitical tensions, enhancement of situational awareness and interoperability, and rising complexity is driving the command & control industry.

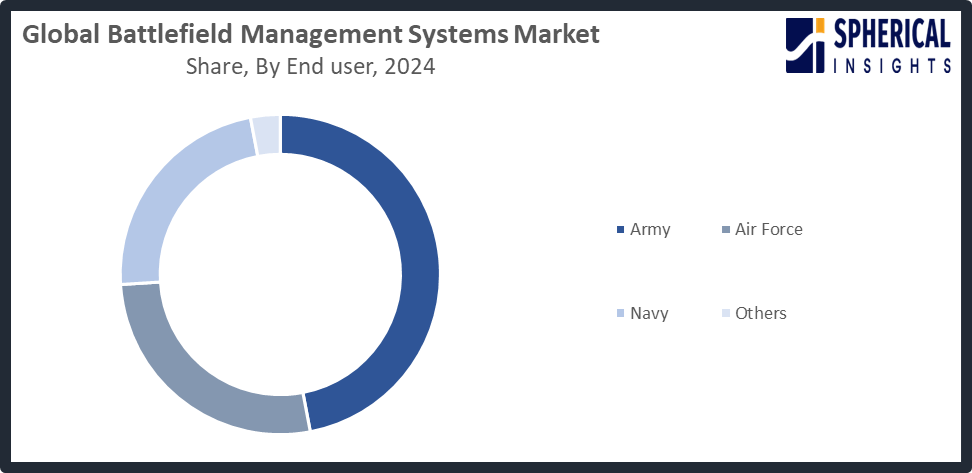

- The army segment accounted for the highest market revenue in 2024, approximately 47%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the battlefield management systems market is divided into army, navy, air force, and others. Among these, the army segment accounted for the highest market revenue in 2024, approximately 47%, and is anticipated to grow at a significant CAGR during the forecast period. Increased demand for deployment in ground operations, widespread implementation of surveillance systems, increased investment in modernization and digitization programs, and increased need for real-time intelligence is bolstering army market.

Get more details on this report -

Regional Segment Analysis of the Battlefield Management Systems Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the battlefield management systems market over the predicted timeframe.

North America is anticipated to hold the largest share of the battlefield management systems market over the predicted timeframe. Strong government backing for extensive defense budgets, advanced technological infrastructure, and early adoption of network-centric warfare systems are what propel North America. The U.S. and Canada are investing heavily in next-generation command-and-control platforms, AI-enabled battlefield analytics, and integrated sensor networks which receive financial backing from the government and military contracts with defense contractors. North America controls the largest portion of the market because it combines financial resources with advanced technology and military strategies designed for contemporary warfare.

Get more details on this report -

Government initiatives include the U.S. Navy Program CEC, August 2025, enhances real-time sensor sharing and integrated weapon coordination across naval forces, supporting network-centric battlefield management and situational awareness and the U.S. Army’s Project Convergence launch, October 2022, to tests and links sensors, shooters, and command networks to improve battlefield awareness and inform next-generation command-and-control systems under JADC2.

Asia Pacific is expected to grow at a rapid CAGR in the battlefield management systems market during the forecast period. China, India, Japan, and South Korea are among the nations making significant investments in expanding defense budgets, military modernization programs, and increased geopolitical tensions. The region's advanced command and control systems together with its real time situational awareness abilities and integrated battlefield solutions create a strong requirement for battlefield management systems. The demand for BMS solutions throughout Asia Pacific has increased because of the push for domestic defense manufacturing combined with the use of AI and unmanned systems and secure communication technologies.

Government launches include Australia’s LAND 200 Phase 3 Battlefield Command Systems project, approved on 13 July 2023, which aims to deliver next-generation battlefield management and tactical communications for the Australian Army, and Singapore’s DIS, launched in October 2022, a government-led SAF branch that integrates C4I and cyber capabilities to enhance real-time command, control, and battlefield awareness, supporting modern battlefield management.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the battlefield management systems market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- BAE Systems plc.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- RTX Corporation

- Thales Group

- General Dynamics Corporation

- Elbit Systems Ltd

- Leonardo S.p.A.

- Saab AB

- Kongsberg Gruppen ASA

- Rheinmetall AG

- L3Harris Technologies, Inc.

- Israel Aerospace Industries Ltd.

- ASELSAN A.A.

- Indra Sistemas, S.A.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

In March 2026, the U.S. Department of Defense announced plans to designate Palantir’s Maven Smart System, an AI-driven digital battle management and situational awareness platform, as an official program of record, signaling long-term integration across U.S. military operations. This move reflects Palantir’s expanded role in battlefield data analytics, decision support, and operational awareness.

In December 2025, OpenPR Industry highlighted that battlefield management systems are advancing with AI integration and real-time command innovations, reflecting ongoing product and technology evolution in the market.

In September 2024, Indra and Thales announced upgrades to the Spanish Army’s Battlefield Management System to improve processing capacity, mobility, and interoperability, representing a key battlefield management advancement.

In April 2024, BAE Systems received an additional USD 25 million modification to its Marine Corps amphibious combat vehicles contract, which supports expanded command and control capabilities tied to BMS functions within the ACV family.

In January 2024, BAE Systems delivered the first Amphibious Combat Vehicle Command and Control (ACV C) variant under full-rate production to the U.S. Marine Corps, providing mobile command, control, and situational awareness capabilities that support future battlefield management integration.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the battlefield management systems market based on the below-mentioned segments:

Global Battlefield Management Systems Market, By Component

- Hardware

- Software

Global Battlefield Management Systems Market, By System

- Navigation & Mapping

- Communication

- Command & Control

- Computing

- Others

Global Battlefield Management Systems Market, By End User

- Army

- Navy

- Air Force

- Others

Global Battlefield Management Systems Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What technologies do battlefield management systems support?BMS solutions support technologies such as real-time situational awareness platforms, integrated C4ISR, AI-driven decision support, IoT-enabled sensor networks, and secure data-sharing across joint forces.

-

2. What communication bands are commonly used in BMS?BMS solutions often operate across VHF, UHF, and satellite communication (SATCOM) bands, as well as secure military data networks to ensure reliable connectivity across diverse terrains and operational theaters.

-

3. What is the role of over-the-air (OTA) testing in BMS?OTA testing evaluates the performance of communication and sensor systems in real-world battlefield conditions without wired connections. It is crucial for validating wireless links, interoperability, and system reliability under mobility and interference.

-

4. What is network emulation in BMS testing?Network emulators simulate battlefield network conditions such as latency, jamming, node failures, and mobility patterns, allowing developers to assess system performance and resilience before deployment.

-

5. What industries will benefit from BMS advancements?Defense forces, homeland security, disaster response, peacekeeping operations, and defense contractors benefit from advanced BMS capabilities, enabling faster decision-making, improved situational awareness, and coordinated operations.

-

6. What is the expected commercialization and deployment timeline for BMS?Many BMS programs are already operational, with ongoing modernization and upgrades planned throughout the 2020s. Advanced AI-enabled and integrated systems are expected to see broader deployment by 2025–2030.

Need help to buy this report?