Global Automotive Wiping Systems Market Size, Share, and COVID-19 Impact Analysis, By Vehicle Type (Passenger Cars and Commercial Vehicles), By Component (Wiper Blades, Wiper Motor, Pumps, and Others), By Application (Windshield Washer, Headlight Washer, and Rear Glass), By Sales Channel (OEM and Replacement/Aftermarket), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Automotive & TransportationGlobal Automotive Wiping Systems Market Insights Forecasts to 2035

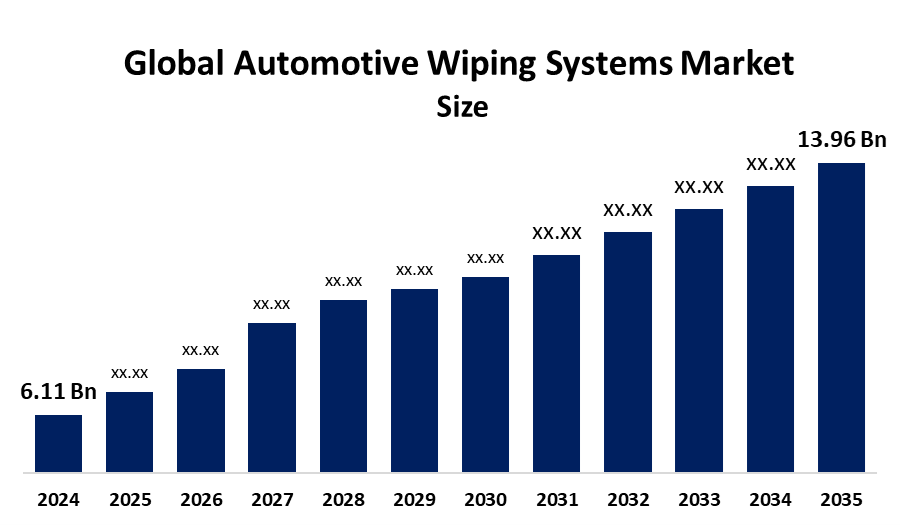

- The Global Automotive Wiping Systems Market Size Was Estimated at USD 6.11 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 7.8% from 2025 to 2035

- The Worldwide Automotive Wiping Systems Market Size is Expected to Reach USD 13.96 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global automotive wiping systems market size was worth around USD 6.11 billion in 2024 and is predicted to grow to around USD 13.96 billion by 2035 with a compound annual growth rate (CAGR) of 7.8% from 2025 to 2035. The automotive wiping systems market is growing due to rising vehicle production, stricter safety regulations demanding clear visibility, and increased demand for advanced, smart rain-sensing wipers. Additionally, the shift toward EVs, SUVs, and high-performance beam blades, coupled with robust aftermarket replacement rates, drives this expansion.

designed to clear rain, snow, ice, dirt, and debris from windshields, rear windows, and headlights for optimal driver visibility and safety. Key uses cover passenger cars, SUVs, commercial vehicles, and specialized applications such as rain-sensing automatic systems, headlamp washers, and camera cleaning modules for ADAS, equipped vehicles.

Primary market drivers are rising global vehicle production, stringent road safety regulations mandating enhanced visibility features, growing consumer demand for convenience technologies like rain-sensing and adaptive-speed wipers, increasing adoption in electric and autonomous vehicles, and frequent replacement needs due to weather wear. Opportunities include integration with advanced driver-assistance systems (ADAS), development of durable silicone and eco-friendly blades, smart connected wiping solutions, and strong aftermarket growth in emerging economies. In May 2024, the U.S. National Highway Traffic Safety Administration (NHTSA) upheld FMVSS No. 104, requiring power-driven windshield wipers with at least two speeds and defined wiped areas for cars, trucks, and buses. No amendments were introduced for 2024, ensuring continued compliance with established safety standards.

Report Coverage

This research report categorizes the automotive wiping systems market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the automotive wiping systems market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the automotive wiping systems market.

Global Automotive Wiping Systems Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 6.11 billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 215 |

| Tables, Charts & Figures: | 117 |

| Segments covered: | By Vehicle Type |

| Companies covered:: | Robert Bosch GmbH, Mitsuba Corp., DENSO Corporation, Valeo SA, HELLA GmbH & Co. KGaA, Trico Products Corp., Continental AG, DOGA S.A., Lucas TVS Limited, WEXCO Industries, Nippon Wiper Blade, Cardone Industries, Federal-Mogul, Zhejiang Shenghuabo Electric Corp., Others, and |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global automotive wiping systems market is propelled by rising vehicle production, with China producing 31.28 million units in 2024, a 3.7% increase, driving OEM demand. Strict safety regulations requiring clear driver visibility further support growth. Expanding electric vehicle adoption, including 12.9 million NEVs in China, fuels demand for energy-efficient, aerodynamic wipers. Integration with ADAS technologies, such as rain-sensing wipers that maintain camera and sensor clarity, creates new opportunities. Additionally, urbanization, higher traffic density, and frequent adverse weather events increase the need for reliable visibility solutions. Advanced wipers, heated, aerodynamic, and smart designs, enhance safety and convenience globally. In April 2024, the UNECE amended UN Regulation No. 167, enhancing direct frontal visibility for heavy goods vehicles to protect pedestrians and cyclists. Transitional deadlines extend to 2031 for approvals and 2036 for registrations, with the EU estimating 550 annual lives saved once fully implemented.

Restraining Factors

The global automotive wiping systems market faces restraints from high costs of advanced wiper technologies, such as rain-sensing and heated systems, and stringent automotive manufacturing regulations. Additionally, increasing adoption of advanced driver-assistance systems (ADAS) with automated cleaning features may reduce demand for traditional wiper systems, limiting overall market growth.

Market Segmentation

The automotive wiping systems market share is classified into vehicle type, component, application, and sales channel.

- The passenger cars segment dominated the market in 2024, approximately 68% and is projected to grow at a substantial CAGR during the forecast period.

Based on the vehicle type, the automotive wiping systems market is divided into passenger cars and commercial vehicles. Among these, the passenger cars segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment dominance is attributed to their high global production volumes, rising safety awareness, and stringent regulatory standards mandating reliable visibility. Increasing adoption of advanced wiper technologies, including rain-sensing, heated, and aerodynamic designs, in both new and retrofitted vehicles further drives demand, making passenger cars the largest market contributor.

- The wiper blades segment accounted for the largest share in 2024, approximately 52% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the component, the automotive wiping systems market is divided into wiper blades, wiper motor, pumps, and others. Among these, the wiper blades segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The wiper blades segment is growing in the automotive wiping systems market due to their essential role in ensuring driver visibility and safety. High replacement frequency, widespread adoption across passenger and commercial vehicles, and growing demand for advanced designs like aerodynamic, heated, and rain-sensing blades drive significant market growth globally.

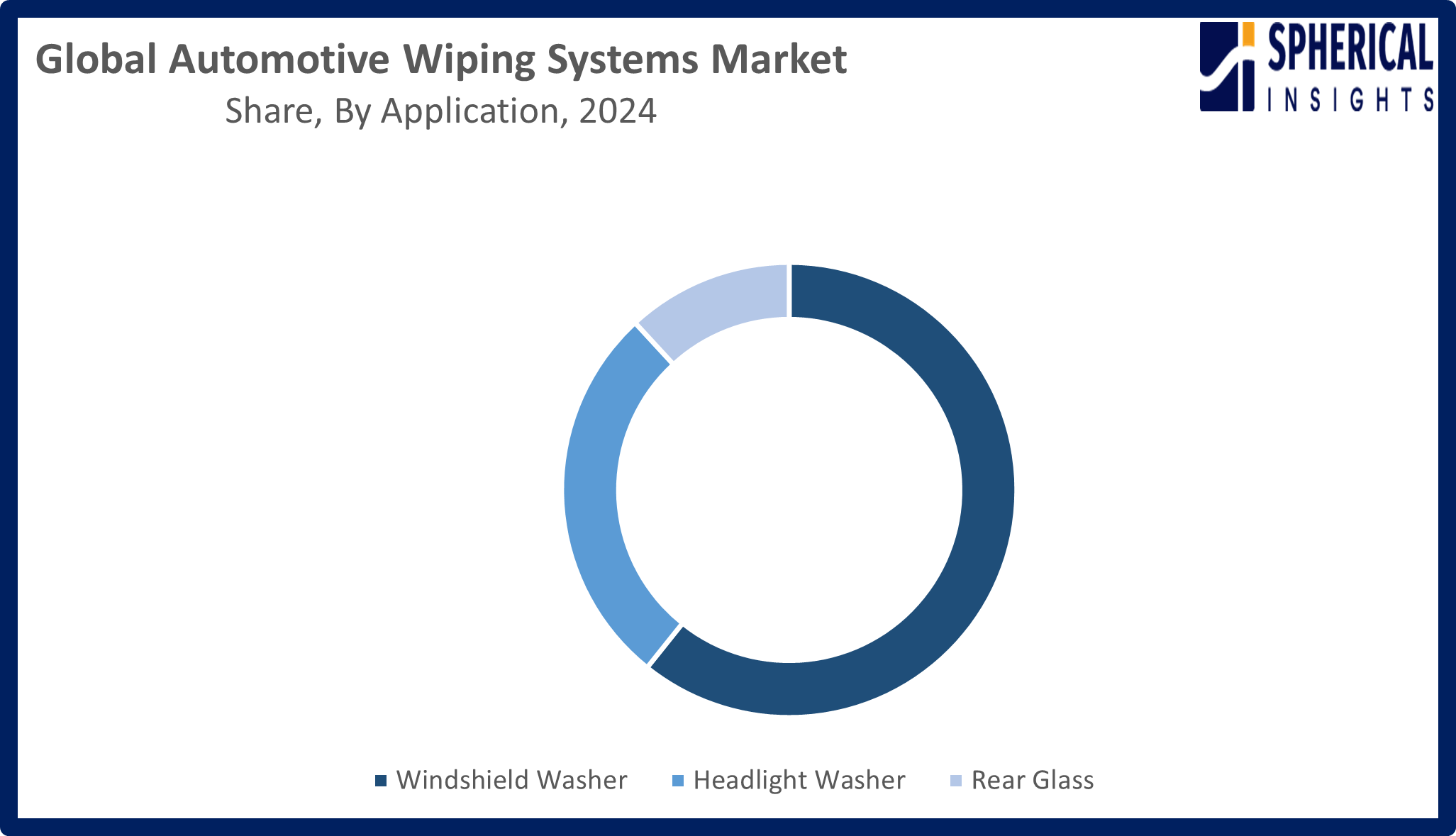

- The windshield washer segment dominated the market in 2024, approximately 61% and is projected to grow at a substantial CAGR during the forecast period.

Based on the application, the automotive wiping systems market is divided into windshield washer, headlight washer, and rear glass. Among these, the windshield washer segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment growth driven by its critical role in maintaining clear visibility during adverse weather conditions. Rising vehicle production, stringent safety regulations, and increasing adoption of advanced washer technologies, including automated and sensor-integrated systems, enhance safety and convenience, driving strong demand across passenger, commercial, and electric vehicles globally.

Get more details on this report -

- The OEM segment accounted for the highest market revenue in 2024, approximately 65% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the sales channel, the automotive wiping systems market is divided into OEM and replacement/aftermarket. Among these, the OEM segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The OEM segment growth in the market is owing to its integration of advanced, reliable wiper and washer systems during vehicle manufacturing. Rising vehicle production, strict safety regulations, and the growing adoption of electric and premium vehicles with sophisticated wiping technologies drive consistent demand within the OEM channel globally.

Regional Segment Analysis of the Automotive Wiping Systems Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the automotive wiping systems market over the predicted timeframe.

Asia Pacific is anticipated to hold the 40% share of the automotive wiping systems market over the predicted timeframe. Asia Pacific is leading the automotive wiping systems market due to rapid vehicle production, rising safety awareness, and expanding automotive infrastructure. China drives the region, producing 31.28 million vehicles in 2024, including 12.9 million new energy vehicles, boosting demand for advanced, energy-efficient wiper systems. Japan, India, and South Korea contribute through growing passenger car and commercial vehicle markets. Increasing adoption of smart technologies, such as rain-sensing, heated, and aerodynamic wipers in electric and premium vehicles, further strengthens market growth across the region.

North America is expected to grow at a rapid CAGR in the automotive wiping systems market during the forecast period. The region is rapidly growing in the automotive wiping systems market due to strict safety regulations, high vehicle production, and growing adoption of advanced wiper technologies. The United States, as the largest contributor, enforces standards like FMVSS Nos. 103 and 104, driving demand for reliable wiper and washer systems. Rising electric and premium vehicle sales, coupled with the integration of ADAS features such as rain-sensing wipers for sensor and camera visibility, further accelerate market growth across passenger and commercial vehicles in the region. In September 2025, the U.S. NHTSA began modernizing FMVSS Nos. 103 and 104 for Automated Driving System (ADS) vehicles. The proposal removes manual defrosting and wiper requirements for purpose-built autonomous vehicles, reflecting reliance on sensor-based visibility. The rule is slated for publication in January 2026.

Europe’s automotive wiping systems market growth is driven by stringent vehicle safety regulations, increasing adoption of advanced wiper technologies, and rising production of passenger and commercial vehicles. Germany, as the region’s largest contributor, leads with robust automotive manufacturing and innovation in rain-sensing and aerodynamic wipers. Growing electric vehicle adoption and integration with ADAS features further boost demand, ensuring enhanced visibility, safety, and market expansion across the European automotive sector.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the automotive wiping systems market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Robert Bosch GmbH

- Mitsuba Corp.

- DENSO Corporation

- Valeo SA

- HELLA GmbH & Co. KGaA

- Trico Products Corp.

- Continental AG

- DOGA S.A.

- Lucas TVS Limited

- WEXCO Industries

- Nippon Wiper Blade

- Cardone Industries

- Federal-Mogul

- Zhejiang Shenghuabo Electric Corp.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the automotive wiping systems market based on the below-mentioned segments:

Global Automotive Wiping Systems Market, By Vehicle Type

- Passenger Cars

- Commercial Vehicles

Global Automotive Wiping Systems Market, By Component

- Wiper Blades

- Wiper Motor

- Pumps

- Others

Global Automotive Wiping Systems Market, By Application

- Windshield Washer

- Headlight Washer

- Rear Glass

Global Automotive Wiping Systems Market, By Sales Channel

- OEM

- Replacement/Aftermarket

Global Automotive Wiping Systems Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.What economic factors are driving investment in advanced wiper technologies?Rising vehicle production and safety spending boost investment in advanced wiper technologies. With global light‑vehicle output exceeding 80 million units in 2024, automakers allocate more to sensor‑enabled wipers, driven by growing demand for enhanced safety and premium features.

-

2.How are government regulations and vehicle safety standards shaping market growth?Government safety standards, including expanded AFCI/AFDD and visibility requirements, are driving automotive wiping systems demand. Regions like North America and Europe report 5-7% annual safety‑tech growth, boosting advanced wiper adoption and regulatory compliance.

-

3.What technological advancements are emerging in wiper blade materials and efficiency?Emerging advancements include graphene‑enhanced and silicone‑coated wiper blades, improving durability by 30-50%, and aerodynamic, motor‑optimized designs that reduce drag and noise, boosting overall wiping efficiency and lifespan in diverse weather conditions.

-

4.How does integration with ADAS and autonomous driving systems affect market adoption?Integration with ADAS and autonomous driving systems boosts market adoption as advanced visibility solutions become essential; vehicles with such systems are expected to exceed 50% global penetration by 2030, increasing demand for smart wiping technologies.

-

5.What are the primary economic factors influencing the pricing and adoption of wiping systems?Primary economic factors include raw material costs (steel, rubber), inflation‑linked production expenses, and consumer purchasing power. With global automotive production exceeding 80 million units in 2024, cost‑efficient wiping systems are crucial for competitive pricing and wider adoption.

Need help to buy this report?