Global Automotive GenAI Copilot Market Size, Share, and COVID-19 Impact Analysis, By Vehicle Type (Passenger Vehicles and Commercial Vehicles), By Level of Autonomy (L0-L1 (Basic), L2/L2+ (Partial Automation), L3 (Conditional Automation), and L4/L5 (High/Full Automation)), By Application (In-Cabin Conversational AI, Predictive Maintenance, Advanced Driver Assistance Systems (ADAS) Integration, Navigation and Routing, and Personalized Entertainment), By Sales Channel (OEM/Factory Fitted and Aftermarket), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Automotive & TransportationGlobal Automotive GenAI Copilot Market Insights Forecasts to 2035

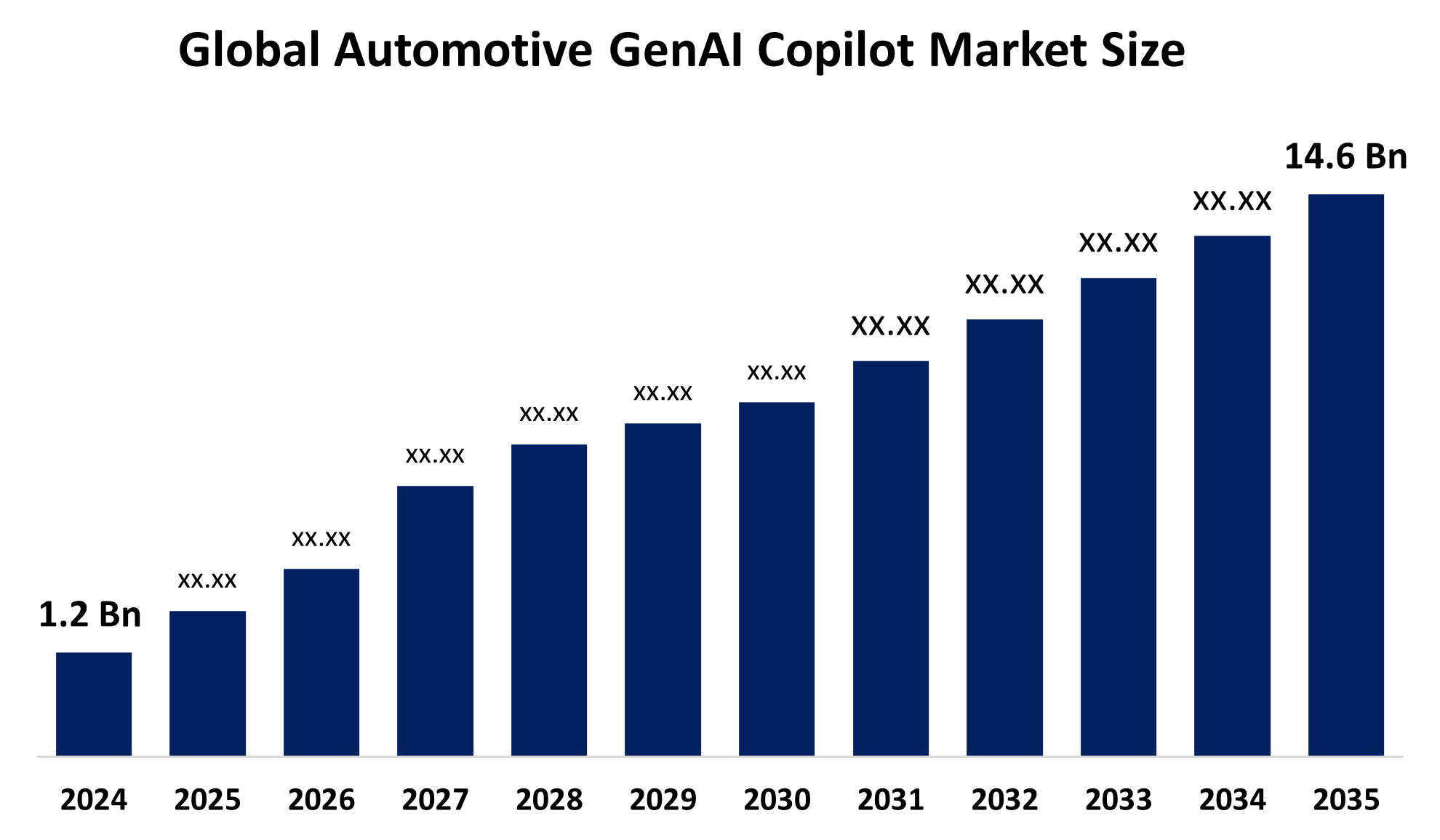

- The Global Automotive GenAI Copilot Market Size Was Estimated at USD 1.2 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 25.5% from 2025 to 2035

- The Worldwide Automotive GenAI Copilot Market Size is Expected to Reach USD 14.6 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, The Global Automotive GenAI Copilot Market Size was worth around USD 1.2 Billion in 2024 and is Predicted to Grow to around USD 14.6 Billion by 2035 with a compound annual growth rate (CAGR) of 25.5% from 2025 to 2035. The automotive GenAI copilot market is growing due to rising consumer demand for personalized digital cabins, the rapid shift toward software-defined vehicles, enhanced safety via advanced driver assistance systems (ADAS), and automakers using AI to differentiate in a competitive EV market.

Automotive GenAI Copilot Market Key Takeaways

- North America dominated the global automotive GenAI copilot market with the largest share of 40% in 2024.

- Asia-Pacific is expected to grow at the fastest CAGR in the market during the forecast period.

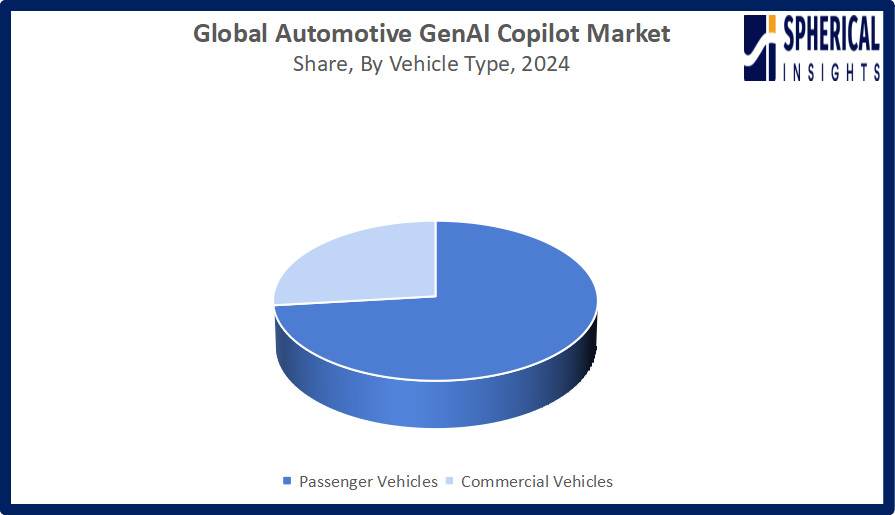

- By vehicle type, the passenger vehicles segment accounted for a considerable revenue share of 73% in the market in 2024.

- By vehicle type, the commercial vehicles segment is expected to grow at the fastest CAGR in the market between 2024 and 2035.

- By level of autonomy, the L2/L2+ (partial automation) segment dominated the global market in 2024, with an approximate 56% share market.

- By level of autonomy, the L3 (conditional automation) segment is expected to show the fastest growth over the forecast period.

- By application, the in-cabin conversational AI segment accounted for the 45% share in the market in 2024.

- By application, the predictive maintenance segment is expected to grow with the highest CAGR in the market during the studied years.

- By sales channel, the OEM/factory fitted segment dominated the global market in 2024, with an approximate 85% share of the market.

- By sales channel, the aftermarket segment is expected to show the fastest growth over the forecast period.

Market Overview

The global automotive GenAI copilot market encompasses generative AI systems, ranging from cloud-connected large language models to edge-based smaller models, that integrate with vehicle architectures via CAN bus systems to enable context-aware control of cabin features, navigation, predictive maintenance, and real-time decision-making. These solutions are widely used for in-cabin conversational interfaces, natural-language vehicle control, personalized infotainment (accounting for over 45% share), predictive diagnostics through telemetry analysis, ADAS explainability, route optimization, and immersive multimedia experiences across passenger and commercial vehicles. In August 2024, Acsia Technologies inaugurated its global headquarters and R&D center in Thiruvananthapuram, where Minister P. Rajeeve launched Lila, a generative AI copilot designed to automate coding and accelerate automotive software innovation, reinforcing regional ambitions to become a global automotive technology hub.

Market growth is accelerating alongside rising connected vehicle adoption, which exceeded 60% globally in 2024. Demand for intelligent mobility, advancements in AI chipsets, and increasing integration by leading automakers are key growth drivers. Studies suggest more than 70% of consumers favor AI-powered in-car assistants, further boosting adoption. Emerging opportunities include digital twin integration, autonomous driving systems, and cloud-based engineering platforms, supported by growing investments in AI ecosystems. In March 2026, during Two Sessions, automotive leaders, including Zhu Huarong and Li Shufu, urged faster autonomous-driving laws, citing European Union regulations as a benchmark. Proposals call for legal recognition of AI driving systems and clearer accident liability frameworks to support GenAI copilots and advanced automation adoption.

Impact of AI in the Automotive GenAI Copilot Market

AI is transforming the automotive GenAI copilot market by enabling real-time decision-making, personalized in-cabin experiences, and predictive maintenance. It enhances ADAS transparency, optimizes navigation, and automates software development. Growing integration of AI models improves vehicle intelligence, boosts user satisfaction, and accelerates innovation, driving widespread adoption across connected and autonomous mobility ecosystems.

Automotive GenAI Copilot Market Trends

1. Shift toward edge + cloud AI integration:

Automakers are combining cloud-based large language models with edge AI for faster, low-latency responses. This hybrid approach improves real-time decision-making, enhances privacy, and ensures continuous functionality even with limited connectivity.

2. Rise of in-cabin personalization:

GenAI copilots are increasingly enabling hyper-personalized user experiences, including voice-controlled features, adaptive infotainment, and behavior-based recommendations, significantly improving driver comfort, engagement, and brand differentiation.

3. Integration with ADAS and autonomous systems:

AI copilots are being integrated with ADAS to explain automated decisions, improve safety transparency, and support higher levels of autonomy, making vehicles more intelligent, trustworthy, and aligned with evolving regulatory expectations.

Report Coverage

This research report categorizes the automotive GenAI copilot market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the automotive GenAI copilot market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the automotive GenAI copilot market.

Global Automotive GenAI Copilot Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 1.2 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 25.5% |

| 2035 Value Projection: | USD 14.6 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 195 |

| Tables, Charts & Figures: | 102 |

| Segments covered: | By Vehicle Type, By Level of Autonomy |

| Companies covered:: | Cerence Inc., NVIDIA Corporation, SoundHound AI, Inc., Google LLC, Aptiv PLC, Baidu, Inc., Microsoft Corporation, Robert Bosch GmbH, Valeo SA, Qualcomm Technologies, Inc., Harman International Industries, Inc., Apple Inc., Continental AG, TomTom International BV, and Other Key Players |

| Pitfalls & Challenges: | and COVID-19 Impact Analysis |

Get more details on this report -

Driving Factors

The global automotive GenAI copilot market is driven by the rapid adoption of software-defined and connected vehicles, which enable over-the-air updates and continuous feature enhancement. Increasing consumer demand for hyper-personalized, intuitive in-car experiences that mimic at-home smart assistants is a key catalyst. The expansion of electric and autonomous vehicle segments necessitates intelligent copilots for range optimization, charging management, and hands-free operation. Major automakers deploy GenAI to differentiate brands as electric powertrains commoditize, while seeking to own customer relationships and reduce reliance on tech giants. In July 2025, the European Union issued its General AI Code of Practice, effective August 2, 2025. The regulation mandates strict oversight for automotive AI, requiring disclosure of sensor algorithms and training data. Non-compliance may incur penalties up to 7% of global turnover, raising vehicle R&D costs significantly.

Restraining Factors

Key restraining factors include high implementation costs and uncertain ROI, leading Gartner to predict that by 2029, 95% of automakers will reduce AI investment growth due to disappointing returns. Consumer resistance is significant, with only 23% of European drivers willing to pay extra for AI features. Technical complexity, legacy integration challenges, data privacy concerns, and a shortage of skilled talent further hinder adoption.

Market Segmentation

Vehicle Type Insights

The passenger vehicles segment held a dominant position in the market in 2024, driven by demand for advanced, localized generative AI models. OEMs must shift toward software-defined architectures, treating vehicles as continuously evolving computing platforms. This transition relies on strong AI chipset performance and delays risk, leaving traditional brands vulnerable to agile, software-centric EV competitors.

The commercial vehicles segment is expected to show the fastest growth over the forecast period, as rising fleet digitization, demand for predictive maintenance, and AI-driven route optimization. Increasing adoption of connected logistics, cost-efficiency needs, and real-time decision support are accelerating GenAI copilot integration across transportation and delivery operations.

Get more details on this report -

Level of Autonomy Insights

The L2/L2+ (partial automation) segment registered its dominance over the global market in 2024, attributed to widespread adoption of ADAS features such as adaptive cruise control and lane-keeping assist. Strong regulatory acceptance, affordability compared to higher autonomy levels, and integration by major automakers have accelerated deployment, while consumer demand for enhanced safety and driving convenience continues to drive sustained growth globally.

The L3 (conditional automation) segment is expected to gain the fastest market share in 2024. Growth is due to increasing regulatory approvals, advancements in sensor fusion and AI processing, and rising demand for hands-off driving. Premium automakers are accelerating deployment, enhancing convenience and safety in controlled driving environments.

Application Phase Insights

The in-cabin conversational AI segment led the market in 2024, with growth due to rising consumer demand for voice-enabled control, personalized infotainment, and seamless human-machine interaction. Advancements in natural language processing, integration with vehicle systems, and increasing adoption of connected cars have enabled intuitive user experiences, making AI assistants a key differentiator for automakers globally.

The predictive maintenance segment is expected to expand rapidly in the market in the coming years, as increasing demand for real-time vehicle diagnostics, reduced downtime, and cost optimization. AI-driven telemetry analysis enables early fault detection, improving fleet efficiency, enhancing vehicle lifespan, and driving adoption across both passenger and commercial vehicle segments.

Sales Channel Insights

The OEM/factory fitted segment registered its dominance over the global market in 2024, attributed to automakers’ increasing integration of GenAI copilots during vehicle production, ensuring seamless performance, safety compliance, and brand differentiation. Early adoption of AI-enabled features, coupled with rising consumer preference for pre-installed intelligent systems, continues to drive strong growth in factory-fitted solutions worldwide.

The aftermarket segment is expected to grow at the fastest CAGR during the forecast period. The growth, rising demand for retrofitting older vehicles with AI-enabled copilots, increasing fleet upgrades, and expanding consumer interest in personalized in-cabin experiences are driving the adoption of plug-and-play AI solutions across emerging and mature markets.

Regional Segment Analysis of the Automotive GenAI Copilot Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America Automotive GenAI Copilot Market Trends

North America held a major market share in 2024, due to high adoption of connected vehicles, advanced ADAS systems, and AI-enabled in-cabin assistants. Strong OEM investments, widespread R&D in automotive AI, and consumer demand for personalized, voice-controlled experiences further drive growth. The region benefits from robust technological infrastructure, early adoption of generative AI for software development, and integration of predictive maintenance solutions, enhancing vehicle safety, efficiency, and user experience, making North America a key leader in automotive AI innovation. In December 2024, the National Highway Traffic Safety Administration proposed the AV STEP program to evaluate autonomous vehicles. The initiative aims to enhance safety and transparency for ADS-equipped vehicles, which remain road-legal under Federal Motor Vehicle Safety Standards despite lacking ADS-specific performance standards.

U.S. Automotive GenAI Copilot Market Trends

The U.S. dominates the market in North America, and is growing due to rising adoption of AI-enabled in-cabin assistants, advanced ADAS integration, and predictive maintenance solutions. High connected vehicle penetration, strong OEM investments, and consumer demand for personalized, voice-controlled experiences are accelerating deployment, making the U.S. a key leader in automotive AI innovation. In February 2026, the U.S. National Highway Traffic Safety Administration highlighted a regulatory velocity gap, as enterprise AI innovation outpaces government frameworks, creating challenges in deploying advanced automotive AI technologies.

Asia Pacific Automotive GenAI Copilot Market Trends

Asia-Pacific is expected to experience the fastest growth during the predicted timeframe, owing to rising EV adoption, growing connected vehicle penetration, and supportive government initiatives promoting smart mobility. Increasing investments by OEMs and tech startups in AI-enabled in-cabin assistants, predictive maintenance, and infotainment solutions drive adoption. AI integration improves vehicle intelligence, reduces maintenance costs, and enhances passenger experiences, accelerating market growth across both passenger and commercial vehicle segments in the region. In January 2026, China's Ministry of Industry and Information Technology launched a digital transformation plan mandating AI integration in R&D, production, and management, targeting industry-specific AI models and a 20% reduction in product development cycles by 2027.

India Automotive GenAI Copilot Market Trends

The Indian automotive GenAI copilot market is expanding rapidly, driven by rising EV adoption, government initiatives supporting smart mobility, and increasing connected vehicle penetration. Growing consumer demand for AI-enabled in-cabin assistants, predictive maintenance, and personalized infotainment, combined with investments from OEMs and tech startups, is accelerating market growth nationwide.

Europe Automotive GenAI Copilot Market Trends

The European automotive GenAI copilot market is growing due to strong adoption of AI for in-cabin assistants, ADAS integration, and predictive maintenance. Government support for Industry 4.0, stringent regulatory compliance, and investments in connected vehicles and generative AI tools enhance efficiency, reduce development cycles, and improve vehicle safety and user experience, driving regional market expansion. In December 2025, the EU AI Act classified many automotive AI systems as high-risk, imposing stricter compliance, safety, and lifecycle obligations, driving regulatory readiness and responsible AI deployment across manufacturing and aftermarket operations.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the automotive GenAI copilot market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Cerence Inc.

- NVIDIA Corporation

- SoundHound AI, Inc.

- Google LLC

- Aptiv PLC

- Baidu, Inc.

- Microsoft Corporation

- Robert Bosch GmbH

- Valeo SA

- Qualcomm Technologies, Inc.

- Harman International Industries, Inc.

- Apple Inc.

- Continental AG

- TomTom International BV

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026, Microsoft integrated Anthropic models into its Copilot workplace tools, diversifying AI options for enterprise customers. Microsoft also launched the $99-per-user E7 bundle, a 65% increase, to accelerate the adoption of AI-powered productivity features like document generation, coding assistance, and automation.

- In January 2026, Visteon Corporation announced a collaboration with TomTom to launch the world’s first in-car local AI conversational navigation assistant. Visteon’s cognitoAI platform integrates TomTom’s Automotive Navigation Application, offering a privacy-first, intelligent navigation experience for drivers.

- In January 2026, HARMAN, a Samsung Electronics Co., Ltd. subsidiary, unveiled production-ready in-car personalization technologies. These AI-driven solutions enable adaptive sound design, individualized and shared listening experiences, and branded audio atmospheres, allowing OEMs to create intelligent, expressive cabins that respond to occupants and the driving environment.

- In October 2025, Aptiv unveiled its Gen 8 radar technology for AI-driven ADAS, enabling hands-free urban driving. The radars, also powering the Aptiv PULSE Sensor, combine radar and camera data to enhance perception, reduce system complexity, and replace multiple ultrasonic sensors, lowering costs for automakers.

- In September 2025, Qualcomm Technologies, Inc. and Google Cloud expanded their partnership to deliver agentic AI for automakers. Combining Google’s Automotive AI Agent with Qualcomm’s Snapdragon Digital Chassis enables multimodal, hybrid edge-to-cloud AI, creating personalized, conversational, and enhanced in-car experiences for drivers and passengers.

- In February 2024, Apple is preparing to launch a generative AI-powered coding tool within its Xcode software development package. Similar to Microsoft’s GitHub Copilot, the tool automates code generation, simplifying programming tasks, and has now entered expanded testing ahead of its official release.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Global Automotive GenAI Copilot Market based on the below-mentioned segments:

Global Automotive GenAI Copilot Market, By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

Global Automotive GenAI Copilot Market, By Level of Autonomy

- L0-L1 (Basic)

- L2/L2+ (Partial Automation)

- L3 (Conditional Automation)

- L4/L5 (High/Full Automation)

Global Automotive GenAI Copilot Market, By Application

- In-Cabin Conversational AI

- Predictive Maintenance

- Advanced Driver Assistance Systems (ADAS) Integration

- Navigation and Routing

- Personalized Entertainment

Global Automotive GenAI Copilot Market, By Sales Channel

- OEM/Factory Fitted

- Aftermarket

Global Automotive GenAI Copilot Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1.What are the key technological innovations driving the GenAI Copilot market?Key innovations driving the GenAI Copilot market include advanced natural language processing, AI‑based predictive analytics, and edge computing, improving system accuracy by over 30%, enhancing voice interaction, personalization, and real‑time decision support.

-

2.How are generative AI models transforming in-cabin passenger experiences?Generative AI models are transforming in‑cabin experiences by enabling natural voice interaction, personalized recommendations, and predictive assistance, with user satisfaction improving by over 25% and engagement rates increasing significantly in connected vehicles.

-

3.What economic impact do AI copilots have on OEMs and aftermarket services?AI copilots boost OEM revenue by enabling premium feature differentiation, reducing warranty costs by up to 20%, and expanding aftermarket services through subscriptions and updates, driving significant long‑term economic growth.

-

4.How is government regulation influencing market adoption and compliance costs?Government regulation is accelerating AI copilot adoption by enforcing safety standards, increasing compliance costs by around 15-20%, while boosting consumer trust and accelerating integration in markets with strict rules like the European Union.

-

5.How is consumer preference for personalized, voice-controlled features affecting market demand?Consumer preference for personalized, voice‑controlled features is driving market demand, with over 70% of drivers favoring AI assistants, significantly boosting adoption and in‑vehicle engagement in GenAI copilot systems.

-

6.What investment trends are emerging among automakers and technology providers?Investment trends show automakers and tech providers increasing AI copilot R&D spending by over 30%, forming strategic partnerships, and prioritizing software development to capture rising demand for intelligent, connected vehicle experiences.

-

7.How will AI integration in commercial versus passenger vehicles influence market dynamics?AI integration in commercial vehicles enhances fleet efficiency and safety, while in passenger vehicles, it boosts personalization and convenience, collectively expanding market size, with commercial adoption growing over 25% faster than passenger segments.

-

8.How is software-defined vehicle adoption accelerating market trends?Software-defined vehicle adoption is accelerating market trends by enabling over-the-air updates, real-time AI copilots, and predictive maintenance, with SDV deployment increasing 35% annually, driving faster GenAI copilot integration and revenue growth.

Need help to buy this report?