Global Anti-VEGF Market Size, Share, and COVID-19 Impact Analysis, By Product (Eylea, Lucentis, and Beovu), By Disease (Macular Edema, Diabetic Retinopathy, Retinal Vein Occlusion, and Age-Related Macular Degeneration), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: HealthcareGlobal Anti-VEGF Market Insights Forecasts to 2035

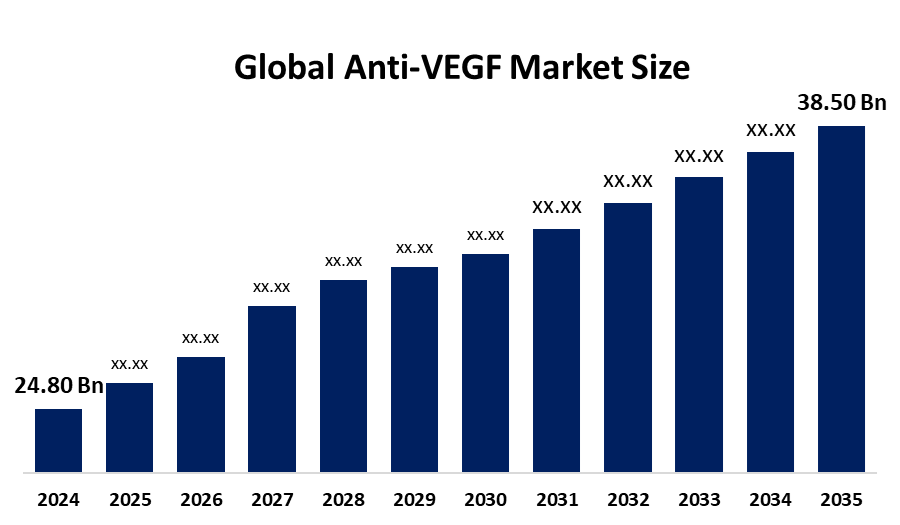

- The Global Anti-VEGF Market Size Was Estimated at USD 24.80 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 4.08% from 2025 to 2035

- The Worldwide Anti-VEGF Market Size is Expected to Reach USD 38.50 Billion by 2035

Get more details on this report -

Key Takeaways -

- North America dominated the market with the largest share in 2024.

- Asia Pacific is expected to grow the fastest during the forecast period.

- By product, the Eylea segment dominates the Anti-VEGF market with the largest share, while the Beovu segment is the emerging segment in the market.

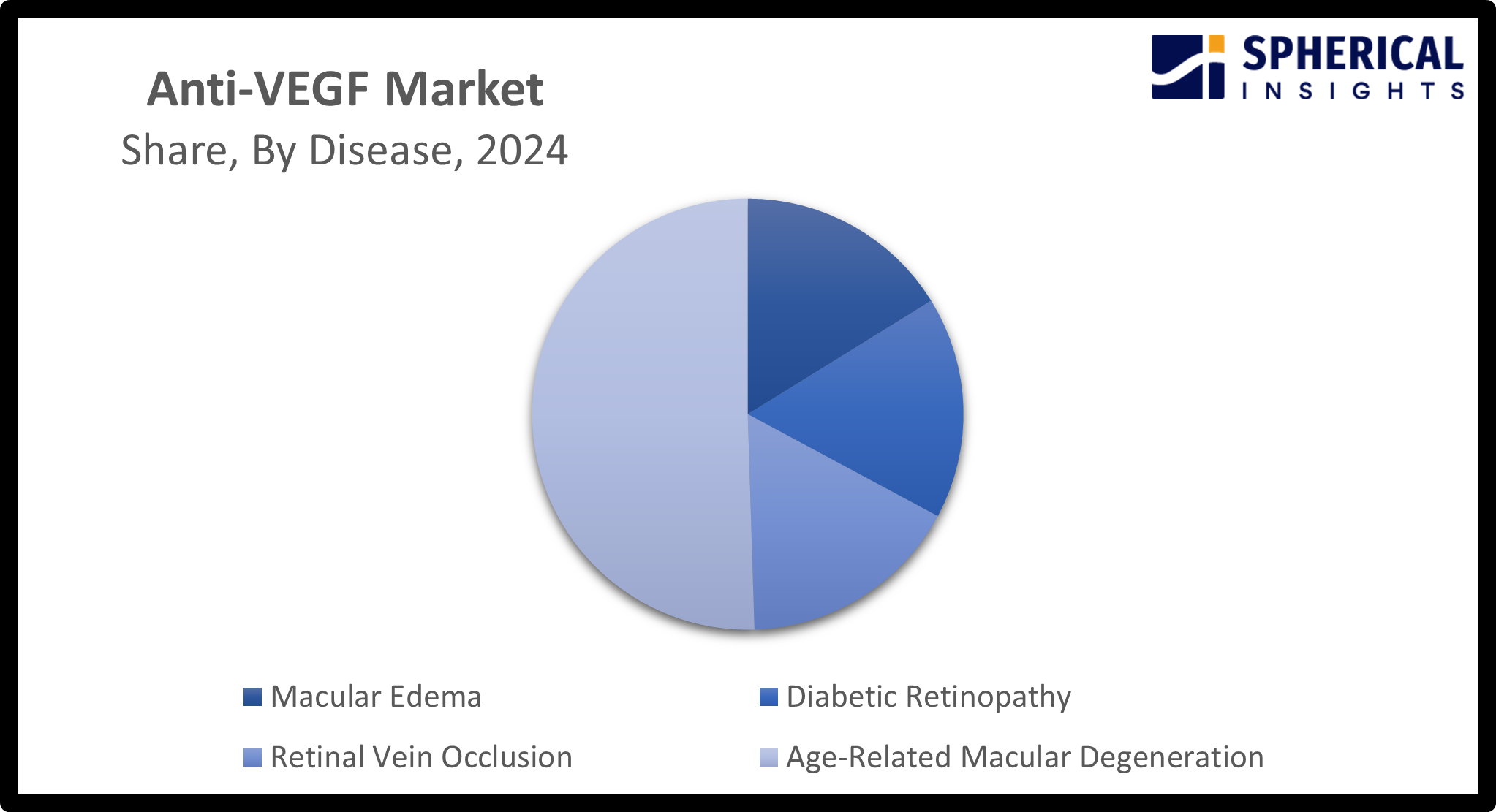

- By disease, the age-related macular degeneration segment is anticipated to hold the largest share; on the other hand, the diabetic retinopathy segment is the fastest growing segment in the anti-VEGF market.

According to a research report published by Spherical Insights and Consulting, the Global Anti-VEGF Market size was worth around USD 24.80 Billion in 2024 and is predicted to grow to around USD 38.50 Billion by 2035 with a compound annual growth rate (CAGR) of 4.08% from 2025 and 2035. The market for anti-VEGF has a number of opportunities to grow due to the ongoing research on developing long-acting, durable agents, biosimilars, gene therapies, and novel delivery systems for reducing injection frequency.

Key Trends in Medical Anti-VEGF Market –

- Combining gene therapy with anti-VEGF to eliminate the need for frequent, lifetime intravitreal injections

- Increasing use of Bispecific antibodies like Faricimab targeting both VEGF and angiopoietin-2

- AI and digital health integration, adoption of biosimilars, and treat-and-extend regimes with anti-VEGF in age-related macular degeneration

Market Overview

The global anti-VEGF industry is the market encompassing drugs used for inhibiting abnormal blood vessel growth, primarily treating retinal eye conditions such as AMD, diabetic macular edema, and retinal vein occlusion. An anti-VEGF treatment involves the anti-VEGF medicine that blocks VEGF (vascular endothelial growth factor), which reduces leaking abnormal blood vessels in the retina, ultimately helps in slowing and stopping the damage from the abnormal blood vessels and slows down vision loss. It was estimated that anti-VEGF treatment improves vision in about one-third (1 out of 3) people who take it, and for the vast majority (9 out of 10), it at least stabilizes vision.

Innovation and market expansion are anticipated as a result of major players' growing R&D expenditures and expanding partnerships. For instance, in July 2025, Harrow entered into commercialization agreement with Samsung Bioepis for Ophthalmology Biosimilars portfolio (BYOOVIZ and OPUVIZ) in the United States.

Report Coverage

This research report categorizes the anti-VEGF market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the anti-VEGF market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the anti-VEGF market.

Global Anti-VEGF Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 24.80 Billion |

| Forecast Period: | 2025 – 2035 |

| Forecast Period CAGR 2025 – 2035 : | 4.08% |

| 025 – 2035 Value Projection: | USD 38.50 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 215 |

| Tables, Charts & Figures: | 113 |

| Segments covered: | By Product, By Disease |

| Companies covered:: | Regeneron Pharmaceuticals, Novartis AG, Roche, Bayer AG, Allergan plc, Pfizer Inc., Bausch Health Companies Inc., AbbVie Inc., Santen Pharmaceutical Co., Ltd., Alcon Inc., Others, and |

| Pitfalls & Challenges: | COVID-19 Impact, Challenges, Future Growth, and Analysis |

Get more details on this report -

Driving Factors

Growing prevalence of eye diseases

Retinal diseases are an emerging cause of visual impairment in the developing world. It was found that the prevalence of retinal disorder was 52.37% at the age of 60 years and above, in which AMD, hypertensive retinopathy, ERM, BRVO, and DR were the most common retinal disorders. Anti-VEGF therapies are sight-saving injections for retina diseases, stopping abnormal blood vessel growth and leaks that cause vision loss.

Technological advancements in delivery systems

Transitioning from frequent, invasive IV injections to sustained release platforms, reducing the treatment burden and improving patient compliance, is driving the anti-VAGF market. For instance, second-generation anti-VEGF agents such as aflibercept 8 mg and faricimab show improved efficacy and treatment durability in DME and AMD. Aflibercept 8 mg provides better anatomic responses and extended treatment intervals due to its slower clearance rate and higher molar dose.

Emergence of biosimilars

Biosimilar medicines (biosimilars) are clinically equivalent, potentially economic alternatives to reference products. For instance, there is ongoing work in developing Ranibizumab biosimilar. For instance, Razumab, a biosimilar to ranibizumab of Intas Pharmaceuticals Ltd., which is approved in India, Byooviz (SB11), from Samsung Bioepis, South Korea, has recently been approved by the US-FDA and EMA. While six other biosimilars, namely FYB 201(Germany), Xlucane (Sweden), R-TPR-024(India), SJP-0133(Japan), LUBT010(India), and CKD-701 (South Korea), are in advanced stages of clinical trials.

Restraining Factors

Adverse effects associated with VEGF inhibitors and price fluctuation

Common ocular side effects include subconjunctival hemorrhage, high intraocular pressure, endophthalmitis, and dry eye, while rare systemic side effects include hypertension, proteinuria, stroke, and heart attack, negatively affecting the adoption of anti-VEGF therapy. This may result in hampering the market growth. Additionally, significant price fluctuation due to the entry of biosimilars, new drug launches, and strategic collaborations is restricting the anti-VEGF market.

Market Segmentation

The Anti-VEGF Market share is classified into product and disease.

- The Eylea segment dominated the market with the largest share of about 61.5% in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on the product, the anti-VEGF market is divided into Eylea, Lucentis, and Beovu. Among these, the Eylea segment dominated the market with the largest share of about 61.5% in 2024 and is projected to grow at a substantial CAGR during the forecast period. This is due to its high durability and “Trap” mechanism. Eylea is an aflibercept solution for injection, approved for the treatment of macular edema following central retinal vein occlusion in Japan from the Japanese Ministry of Health, Labour and Welfare. While the Beovu segment is the emerging segment in the anti-VEGF market, due to its ability to allow longer dosing intervals and enable retinal fluid dryness in wet AMD patients.

- The age-related macular degeneration segment accounted for the largest market share of about 51.5% in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on the disease, the anti-VEGF market is divided into macular edema, diabetic retinopathy, retinal vein occlusion, and age-related macular degeneration. Among these, the age-related macular degeneration segment accounted for the largest market share of about 51.5% in 2024 and is projected to grow at a substantial CAGR during the forecast period. Anti-VEGF drugs are the first-line treatment for wet AMD and are injected into the eye, slowing down the disease progression. Further, the diabetic retinopathy segment is the fastest-growing segment, driven by the increasing diabetes prevalence and blindness caused by diabetes, which leads to the demand for anti-VEGF therapeutics.

Get more details on this report -

Regional Segment Analysis of the Anti-VEGF Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the anti-VEGF market over the predicted timeframe.

North America is anticipated to hold the largest share of about 65.0% in the anti-VEGF market over the predicted timeframe. The market ecosystem in North America is strong, due to the ongoing development of anti-VEGF therapeutics. For instance, in February 2026, 4D Molecular Therapeutics completed enrolment in 4FRONT-1, its phase 3 clinical trial evaluating 4D-150 in patients with wet age-related macular degeneration (AMD). The demand for anti-VEGFs has been driven by the region's increasing prevalence of retinal diseases and diabetic retinopathy, along with an increasing ageing population. The U.S. is leading the North America anti-VEGF market, due to the growing prevalence of age-related macular degeneration with an increasing ageing population, necessitating effective treatment options.

Asia Pacific is expected to grow at a rapid CAGR of approximately 4.3% in the Anti-VEGF market during the forecast period. The Asia Pacific area has a thriving market for anti-VEGFs due to the expansion of anti-VEGF biosimilar drugs, favourable government reimbursement policies, and awareness about early diagnosis. Due to their governments’ support for providing treatment for diabetes-related vision loss. For instance, AB-PM-JAY, the largest health assurance scheme in the world, aims to provide a health cover of Rs. 5 lakhs per family per year for secondary and tertiary care hospitalisation to over 12 crore poor and vulnerable families. China holds the dominant regional share of approximately 30.0% in 2024, owing to the healthcare investments and expanding elderly population.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the anti-VEGF market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Regeneron Pharmaceuticals

- Novartis AG

- Roche

- Bayer AG

- Allergan plc

- Pfizer Inc.

- Bausch Health Companies Inc.

- AbbVie Inc.

- Santen Pharmaceutical Co., Ltd.

- Alcon Inc.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In September 2025, Ollin Biosciences, Inc. (Ollin), a clinical-stage biopharmaceutical company, announced its launch with an initial $100 million in financing led by ARCH Venture Partners, Mubadala Capital and Monograph Capital.

- In October 2024, LaNova Medicines Limited, a privately-held clinical-stage innovation-driven biotech specializing in ADCs and immune-oncology, announced the initiation of its Phase 1 clinical trials of LM-299, an anti-PD-1/VEGF BsAb, in China for advanced solid tumors and the successful completion of its $42 million Series C1 financing.

- In August 2024, Sandoz secured approval for an aflibercept biosimilar. Enzeevu (aflibercept-abzv) is the fourth biosimilar referencing Eylea and is approved to treat neovascular age-related macular degeneration (nAMD) and was granted interchangeability.

- In February 2022, EyeBiotech Ltd. announced the completion of a successful $65 million Series A funding round. SV Health Investors led the round, alongside Samsara BioCapital and Jeito Capital, with additional financial backing from MRL Ventures.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the anti-VEGF market based on the below-mentioned segments:

Global Anti-VEGF Market, By Product

- Eylea

- Lucentis

- Beovu

Global Anti-VEGF Market, By Disease

- Macular Edema

- Diabetic Retinopathy

- Retinal Vein Occlusion

- Age-Related Macular Degeneration

Global Anti-VEGF Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the Anti-VEGF market?The global Anti-VEGF market size is expected to grow from USD 24.80 Billion in 2024 to USD 38.50 Billion by 2035, at a CAGR of 4.08% during the forecast period 2025-2035.

-

2. Which region holds the largest share of the Anti-VEGF market?North America is anticipated to hold the largest share of the Anti-VEGF market over the predicted timeframe.

-

3. What is the forecasted CAGR of the Global Anti-VEGF Market from 2024 to 2035?The market is expected to grow at a CAGR of around 4.08% during the period 2024–2035.

-

4. Who are the top companies that are involved in the Global Anti-VEGF Market?Key players include Regeneron Pharmaceuticals, Novartis AG, Roche, Bayer AG, Allergan plc, Pfizer Inc., Bausch Health Companies Inc., AbbVie Inc., Santen Pharmaceutical Co., Ltd., and Alcon Inc.

-

5. What are the main drivers in the Anti-VEGF market?An increasing prevalence of retinal diseases, technological advancements in delivery systems, and the emergence of biosimilars are major market growth drivers of the anti-VEGF market.

Need help to buy this report?