Global Anti-Fog Lidding Films Market Size, Share, and COVID-19 Impact Analysis, By Sealing Type (Peelable, Easy Peel, Medium Peel, Weld/Lock Seal, and Resealable), By Material Type (PET, APET, CPET, PE, PP, and PA), By Application (Trays, Cups & Bowls, and Jars), By End-use (Meat, Poultry & Seafood, Dairy Products, Fresh Produce, Ready-to-eat, Bakery & Confectionery, Frozen Food, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Anti-Fog Lidding Films Market Insights Forecasts to 2035

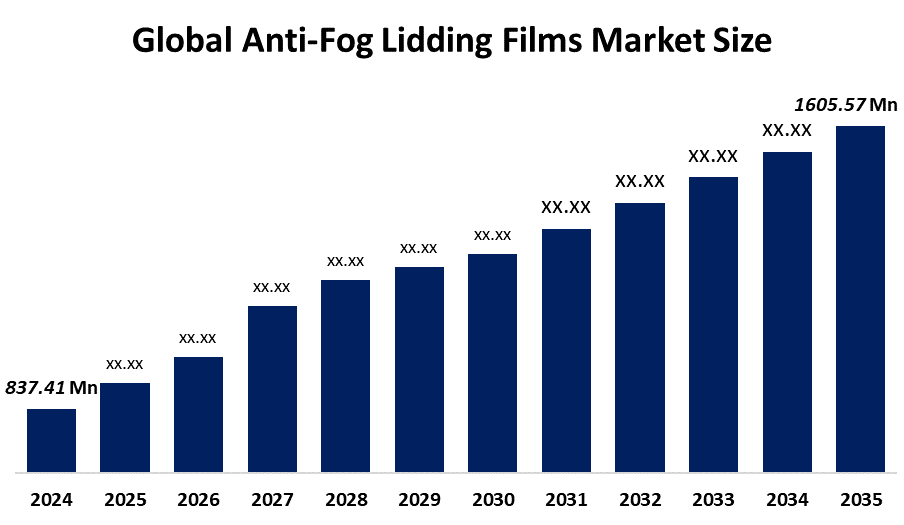

- The Global Anti-Fog Lidding Films Market Size Was Estimated at USD 837.41 Million in 2024

- The Market Size is Expected to Grow at a CAGR of around 6.1% from 2025 to 2035

- The Worldwide Anti-Fog Lidding Films Market Size is Expected to Reach USD 1605.57 Million by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global anti-fog lidding films market size was worth around USD 837.41 million in 2024 and is predicted to grow to around USD 1605.57 million by 2035 with a compound annual growth rate (CAGR) of 6.1% from 2025 to 2035. The anti-fog lidding films market is expanding as rising demand for packaged, ready-to-eat foods and fresh produce, coupled with hygiene concerns and the growth of organized retail and e-commerce, boosts the adoption of high-barrier, anti-condensation films.

Market Overview

The global anti-fog lidding films market consists of specialized flexible packaging films, typically made from PP, PET, or PE with advanced anti-fog coatings or additives, designed to prevent condensation and fogging on the inner surface when sealing trays, cups, or containers holding high-moisture food products. Key uses include lidding for fresh produce, ready-to-eat meals, salads, dairy, meat, seafood, and convenience foods, enabling clear visibility of contents, extended shelf life, and enhanced consumer appeal in retail and foodservice packaging. Primary market drivers are the booming demand for packaged fresh and convenience foods, rising consumer preference for visually attractive packaging, growth in e-grocery and meal-kit deliveries, strict food safety regulations, and the need to reduce food waste through better moisture control.

Opportunities arise in sustainable mono-material and recyclable anti-fog structures, integration of high-barrier properties, expansion in emerging markets with rising organized retail, and development of bio-based or PCR (post-consumer recycled) anti-fog films. In August 2025, China’s Ministry of Industry and Information Technology released the HG/T 6393-2025 standard for PET anti-fog films. The guideline outlines product structure, requirements, testing, inspection, and handling procedures for applications including protective face shields, bathroom mirrors, and refrigerators, promoting consistency and quality in the industry.

Report Coverage

This research report categorizes the anti-fog lidding films market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the anti-fog lidding films market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the anti-fog lidding films market.

Global Anti-Fog Lidding Films Market Growth Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 1605.57 Million |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | 6.1% |

| 2035 Value Projection: | USD 837.41 Million |

| Historical Data for: | 2021-2023 |

| No. of Pages: | 198 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Sealing Type, By Application |

| Companies covered:: | Amcor plc, Sealed Air Corporation, Berry Global Inc., Uflex Ltd., Mondi Group, Toray Plastics, Coveris Holdings S.A., Winpak Ltd., Cosmo Films Limited, Flexopack S.A., Constantia Flexibles Group GmbH, ProAmpac Intermediate Inc., Plastopil Hazorea Company Ltd., Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The global anti-fog lidding films market is driven by growing demand for convenience and ready-to-eat foods, which require clear, moisture-free packaging to enhance consumer appeal. Rising awareness of food safety and hygiene motivates manufacturers to adopt anti-fog films that reduce microbial growth and spoilage. Technological innovations, including multi-layer co-extrusion and biodegradable coatings, improve film performance and sustainability, further stimulating demand. Expansion in frozen and fresh food sectors, especially in the Asia Pacific and North America, supports market growth. Additionally, stringent regulations on packaging quality and shelf-life extension globally encourage widespread adoption of anti-fog lidding films. In November 2025, Mondi expanded its food packaging portfolio, adding solid board solutions and digital printing capabilities after acquiring Schumacher Packaging. The enhanced range, including flexible and corrugated packaging, strengthens Mondi’s European presence, supporting sustainability, regulatory compliance, and evolving consumer demand for convenient, innovative, and standout food packaging.

Restraining Factors

The global anti-fog lidding films market is restrained by high production costs, dependence on specialized raw materials, and stringent regulatory requirements. Competition from alternative packaging, limited recycling infrastructure, and price sensitivity further hinder adoption, especially among small and mid-sized food manufacturers, potentially slowing overall market growth.

Market Segmentation

The anti-fog lidding films market share is classified into sealing type, material type, application, and end-use.

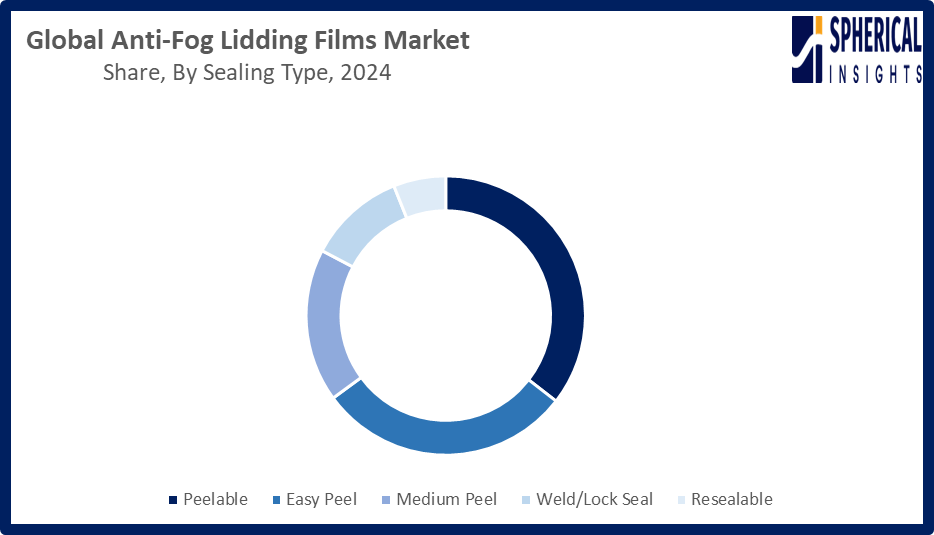

- The peelable segment dominated the market in 2024, approximately 35% and is projected to grow at a substantial CAGR during the forecast period.

Based on the sealing type, the anti-fog lidding films market is divided into peelable, easy peel, medium peel, weld/lock seal, and resealable. Among these, the peelable segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment led market growth due to its widespread use in ready-to-eat meals, fresh produce, and dairy packaging, offering convenience, tamper evidence, and easy opening. Its ability to maintain product integrity, enhance consumer experience, and ensure moisture-free, clear visibility has driven strong adoption, making it the leading sealing type in the anti-fog lidding films market.

Get more details on this report -

- The PET segment accounted for the largest share in 2024, approximately 37% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the material type, the anti-fog lidding films market is divided into PET, APET, CPET, PE, PP, and PA. Among these, the PET segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The PET segment market grows owing to its excellent clarity, strength, and barrier properties, making it ideal for fresh produce, dairy, and ready-to-eat food packaging. Its compatibility with anti-fog coatings, recyclability, and cost-effectiveness drive widespread adoption, supporting growth while meeting consumer demand for transparent, durable, and hygienic packaging solutions.

- The trays segment dominated the market in 2024, approximately 42% and is projected to grow at a substantial CAGR during the forecast period.

Based on the application, the anti-fog lidding films market is divided into trays, cups & bowls, and jars. Among these, the trays segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment dominance is attributed to its extensive use in fresh produce, meat, and ready-to-eat meal packaging, where maintaining product visibility and extending shelf life are critical. Trays provide stability, convenience, and compatibility with anti-fog lidding films, driving high adoption across retail and foodservice sectors, making them the leading application in the market.

- The meat, poultry & seafood segment accounted for the highest market revenue in 2024, approximately 28% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end-use, the anti-fog lidding films market is divided into meat, poultry & seafood, dairy products, fresh produce, ready-to-eat, bakery & confectionery, frozen food, and others. Among these, the meat, poultry & seafood segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The segment market growth is due to increasing demand for packaged, high-protein foods that require extended freshness and clear visibility. Anti-fog lidding films prevent condensation, maintain hygiene, and enhance shelf appeal, making them essential for preserving quality and safety in retail and frozen food applications, driving strong adoption globally.

Regional Segment Analysis of the Anti-Fog Lidding Films Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the anti-fog lidding films market

Get more details on this report -

over the forecast period, accounting for approximately 35% of the total market. The region, led by the United States, dominates due to strong demand for fresh and packaged foods, advanced retail infrastructure, and strict food safety regulations. Consumers in the region increasingly prefer ready-to-eat and refrigerated products, which is driving the adoption of anti-fog lidding films that help prevent condensation and extend shelf life.

Additionally, ongoing technological advancements, the growing emphasis on sustainable packaging, and well-established cold-chain logistics further support market growth. These factors position North America as a key hub for high-quality, regulation-compliant anti-fog packaging solutions.

In March 2026, the United States continues to enforce 21 CFR 178.3130, which regulates antistatic and antifogging agents used in food packaging materials. This regulation specifies permitted substances, maximum allowable concentrations (such as 0.15% for polyolefin films), and film thickness limits, ensuring that manufacturers of anti-fog lidding films comply with established safety standards.Manufacturers of anti-fog lidding films maintain compliance with established safety standards.

Asia Pacific is expected to grow at a rapid CAGR in the anti-fog lidding films market during the forecast period. The region, led by China and India, is experiencing significant growth due to rising demand for fresh, packaged, and ready-to-eat foods, along with the expansion of modern retail and e-commerce sectors and increasing cold-chain infrastructure. Rapid urbanization, rising disposable incomes, and growing awareness of food safety and quality standards are further driving the adoption of anti-fog lidding films. Additionally, technological innovations and the shift toward sustainable packaging solutions are accelerating market growth across the region.

Europe is witnessing steady growth in the anti-fog lidding films market, supported by strong demand for packaged fresh produce, ready-to-eat meals, and dairy products, along with stringent food safety and hygiene regulations. Germany leads the regional market due to its advanced retail infrastructure, strong consumer preference for high-quality and transparent packaging, and increasing adoption of recyclable and sustainable anti-fog films, which support both market expansion and regulatory compliance.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the anti-fog lidding films market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Amcor plc

- Sealed Air Corporation

- Berry Global Inc.

- Uflex Ltd.

- Mondi Group

- Toray Plastics

- Coveris Holdings S.A.

- Winpak Ltd.

- Cosmo Films Limited

- Flexopack S.A.

- Constantia Flexibles Group GmbH

- ProAmpac Intermediate Inc.

- Plastopil Hazorea Company Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Developments

- In March 2026, Amcor expanded its facility in Lugo di Vicenza with a new production line for high-barrier, recycle-ready films. The 7,000 m² extension supports lidding and pouch packaging across the food, beverage, pet food, and healthcare sectors. It also enhances sustainability, recyclability, and quality control through advanced laboratories and temperature-controlled storage.

- In February 2026, Cosmo Films launched its Sealable Peelable Transparent Anti-Fog BOPET lidding film designed for refrigerated and fresh food applications. The film prevents condensation, extends shelf life by 4–5 days, and is compatible with multiple substrates. It is microwaveable, energy-efficient, and fully recyclable when paired with PET trays, improving overall packaging performance.

- In December 2025, Cosmo Films expanded its flexible packaging portfolio for pet food in India by introducing TR-BOPP heat-resistant films, anti-fog BOPET lidding films, and COPET-coated and metallized films. This range enhances barrier performance, sustainability, and food safety, supporting the growing demand across dry, wet, and ready-to-eat pet food segments

- In June 2025, Mondi launched re/cycle PaperPlus Bag Advanced, a high-performance paper bag featuring a 20 µm barrier film designed to protect humidity-sensitive goods. The solution reduces plastic use by up to 60% and lowers the carbon footprint, while being fully recyclable, thereby supporting sustainable packaging in the building, construction, and industrial sectors.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the anti-fog lidding films market based on the below-mentioned segments:

Global Anti-Fog Lidding Films Market, By Sealing Type

- Peelable

- Easy Peel

- Medium Peel

- Weld/Lock Seal

- Resealable

Global Anti-Fog Lidding Films Market, By Material Type

- PET

- APET

- CPET

- PE

- PP

- PA

Global Anti-Fog Lidding Films Market, By Application

- Trays

- Cups & Bowls

- and Jars

Global Anti-Fog Lidding Films Market, By End-use

- Meat, Poultry & Seafood,

- Dairy Products

- Fresh Produce

- Ready-to-eat

- Bakery & Confectionery

- Frozen Food

- Others

Global Anti-Fog Lidding Films Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What role do sustainability trends play in shaping the anti-fog lidding films market?Sustainability trends significantly influence the anti‑fog lidding films market by accelerating demand for recyclable mono‑material and PCR‑content films, with around 18% of new product launches in 2024 featuring recycled or recyclable designs, driven by regulatory pressure and brand commitments to circular packaging and reduced environmental impact.

-

2. How are technological advancements in anti-fog coatings driving industry adoption?Advancements in anti‑fog coatings, boosting film clarity by up to 95% and reducing fogging duration by 30-50%, are increasing adoption in fresh food packaging, extending shelf life and enhancing consumer appeal.

-

3. Which innovations in recyclable and biodegradable films are shaping future opportunities?Innovations in recyclable and biodegradable films are expanding market opportunities, with mono‑material, recyclable PET/PP structures and compostable anti‑fog films gaining traction; over 18% of new lidding film launches in 2024 featured recycled or bio‑based designs, responding to regulatory and consumer sustainability demands.

-

4. How do consumer preferences for fresh and ready-to-eat foods affect market demand?Consumer preference for fresh and ready‑to‑eat foods boosts anti‑fog lidding film demand, as 45% of film usage is tied to fresh and high‑moisture packaged foods that require clear, fog‑free visibility for quality perception, driving packaging adoption in retail and convenience segments.

-

5. What is the economic impact of reducing plastic content in lidding films?Reducing plastic content in anti‑fog lidding films can lower lifecycle costs and environmental penalties, as recyclable mono‑polymer films can be 2-5% cheaper over time in regions with disposal taxes, despite a 10-30% higher upfront production cost, boosting economic viability while cutting waste and regulatory liabilities.

-

6. How do regulatory policies influence production standards and market expansion?Stringent regulatory policies like the EU’s Packaging Waste Regulation, requiring 60%+ recyclable content by 2030, elevate anti‑fog lidding film standards, boost sustainable material adoption, and expand compliant market access globally, driving innovation and higher quality.

-

7. What economic factors are driving investment in anti‑fog lidding film production globally?Rising packaged food demand and cold‑chain expansion, with global food packaging projected to reach USD 1.2 trillion by 2030, drive investment in anti‑fog lidding films for enhanced visibility, safety, and reduced waste.

Need help to buy this report?