Global Anthracite Market Size, Share, and COVID-19 Impact Analysis, By Grade (High Grade, Standard Grade, Ultra-High Grade, and Others), By End-Use (Steel Production, Energy & Power, Bricks, Silicon & Glass, Synthetic Fuels, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Anthracite Market Insights Forecasts to 2035

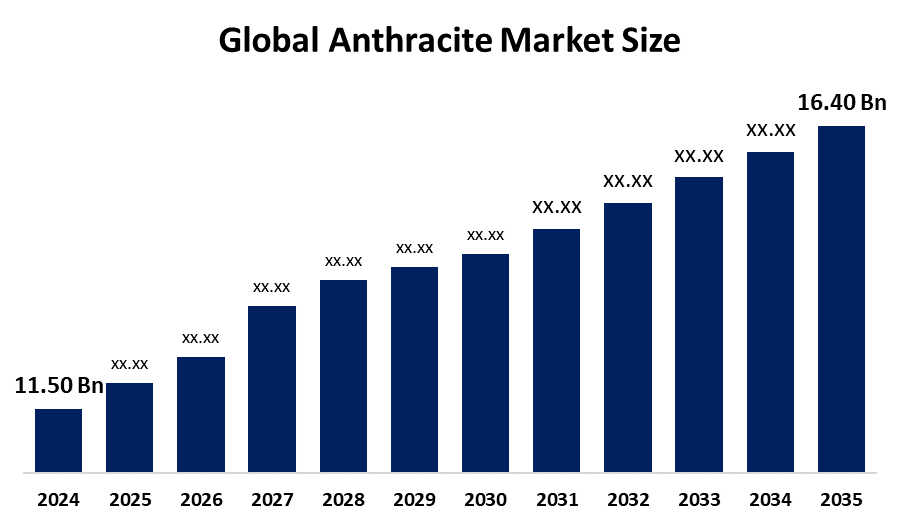

- The Global Anthracite Market Size Was Estimated at USD 11.50 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 3.28% from 2025 to 2035

- The Worldwide Anthracite Market Size is Expected to Reach USD 16.40 Billion by 2035

Get more details on this report -

Key Takeaways -

- Asia Pacific dominated the market with the largest share in 2024.

- North America is expected to grow the fastest during the forecast period.

- By grade, the high grade segment dominates the anthracite market with the largest share of about 47.0% share, while the standard segment is the fastest growing segment in the market.

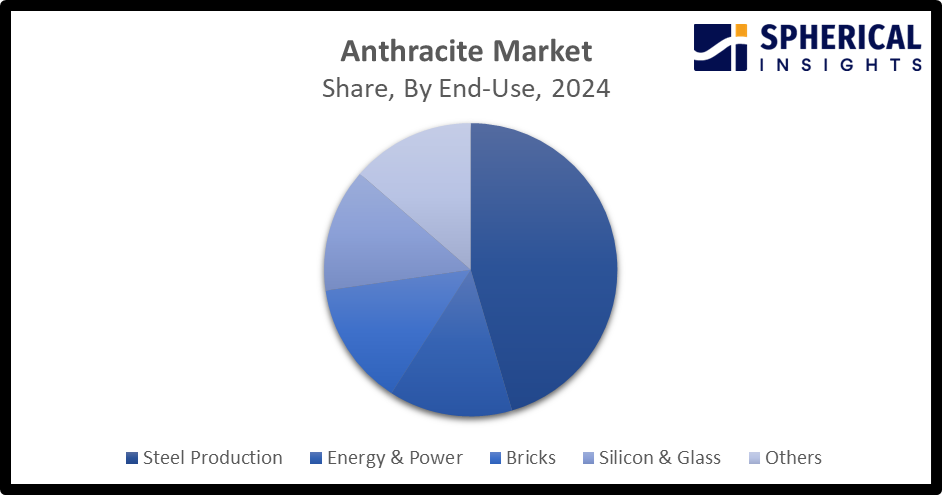

- By end-use, the steel production segment is anticipated to hold the largest market share of about 50.0% in 2024, on the other hand, the energy & power segment is the fastest growing segment in the anthracite market.

According to a research report published by Spherical Insights and Consulting, the Global Anthracite Market size was worth around USD 11.50 Billion in 2024 and is predicted to grow to around USD 16.40 Billion by 2035 with a compound annual growth rate (CAGR) of 3.28% from 2025 and 2035. The market for anthracite has a number of opportunities to grow due to the growing technological advancement in mining and processing for improving operational efficiency and cost competitiveness, along with upsurging needs for extensive infrastructure and industrialization.

Key Trends in Medical Anthracite Market –

- High grade anthracite in steelmaking (PCI applications)

- Electrically calcined anthracite in electric vehicle (EV) batteries

Market Overview

The global anthracite industry is the market encompassing the production and sale of the highest grade of coal (86-97% carbon), utilized for its high energy density, low impurities, and minimal emissions in steelmaking, power generation, and water filtration. Anthracite, also known as “hard coal” or “black diamond”, is a hard, shiny, metamorphic rock that produces intense, long-lasting heat with little smoke or impurities. It has the highest carbon content, the fewest impurities, and the highest energy density of all types of coal and is the highest ranking of coals. Major players' growing R&D expenditures and the expanding partnerships are expected to promote innovation in the anthracite market. For instance, in May 2025, Menar acquired the anthracite mine, Springlake Colliery, from Mylotex (Pty) Ltd after the mine was placed under business rescue.

Report Coverage

This research report categorizes the anthracite market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the anthracite market. Recent market developments and competitive strategies such as expansion, type launch, development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the anthracite market.

Driving Factors

Application of anthracite in steel production

With an expected increase in the use of Electric Arc Furnace (EAF) technology, anthracite is becoming increasingly important in steelmaking as steel manufacturers seek to balance growing demand with the need to curtail emissions. It serves as a key reducing agent in blast furnaces and as a carbon raiser in electric arc furnaces (EAF), enhances steel quality, optimized heat in production, and offers a cleaner, cost-effective, or technically superior alternative to traditional coke.

Increasing use of anthracite in power generation

In the energy industry, anthracite coal has taken over bituminous coal, making it a preferred fuel in a wide range of applications, including power generation. It is prized in power generation for high heat output (13,000-15,000 BTU/lb) and low emissions.

For instance, in August 2025, China put into operation the world’s first 660 megawatt ultra-supercritical double-arch coal-fired generating unit, marking a significant breakthrough in high-efficiency, clean coal power technology, as reported.

Application in water filtration systems

When combined with filtering sands, anthracite is used as a filter medium for industrial or drinking water purification and is among the most used media for filtering. In combination with sand or green manganese sand, it works well with mixed filters. Its unique grain shape enables the suspended particles to be held in the filtering bed’s depth. This filtering media permits a greater flow, less pressure drop, and a better and quicker backwash than a sand filter.

Restraining Factors

Increased extraction & processing costs, as well as environmental concerns associated with mining activities, are challenging the anthracite market. An increased investment in cleaner practices due to regulatory requirements and reputation risks is contributing to restricting market growth.

Market Segmentation

The Anthracite Market share is classified into grade and end-use.

- The high grade segment dominated the market with the largest share of around 47.0% in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on the grade, the anthracite market is divided into high grade, standard grade, ultra-high grade, and others. Among these, the high grade segment dominated the market with the largest share of around 47.0% in 2024 and is projected to grow at a substantial CAGR during the forecast period. This is due to its elevated carbon content and minimal impurities. High grade is widely used as a substitute for coke in sintering, pelletizing, and pulverized coal injection in steelmaking. While the standard segment is the fastest segment in the anthracite market during the forecast period. Standard anthracite is semi-anthracite, high-ranking, hard, shiny coal with low volatile matter, primarily used for power generation, industrial heating, and as a clean-burning fuel.

- The steel production segment accounted for the largest market share of about 50.0% in 2024 and is projected to grow at a substantial CAGR during the forecast period.

Based on the end-use, the anthracite market is divided into steel production, energy & power, bricks, silicon & glass, and others. Among these, the steel production segment accounted for the largest market share of about 50.0% in 2024 and is projected to grow at a substantial CAGR during the forecast period. The extensive use of anthracite as a vital raw material and energy source in the steel manufacturing process contributes to driving the segmental market growth. Anthracite is used in steel production, especially in electric arc furnaces and blast furnaces. Further, the energy & power segment is the fastest growing segment, driven by its high calorific value and lowest ash content and impurities of all coals, which make it an efficient fuel.

Get more details on this report -

Regional Segment Analysis of the Anthracite Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the anthracite market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of about 70.0% in the anthracite market over the predicted timeframe. The demand for anthracites has been driven by the region's rapid industrialization, increased demand for high-grade fuel in steel production, and a strong investment in infrastructure development. China is leading the Asia Pacific anthracite market, holding around 60% region’s share, supported by strategic investments into cleaner and highly efficient carbon materials.

North America is expected to grow at a rapid CAGR of approximately 2.1% in the anthracite market during the forecast period. The Asia Pacific area has a thriving market for anthracites due to the fast-paced infrastructure development, with the presence of a strong industrial system. The U.S. is the dominant country in the North America anthracite market, due to growing emphasis on cleaner energy sources along with an increasing technological advancement.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the anthracite market, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- China Shenhua Energy Company

- Yanzhou Coal Mining Company

- Kuzbassrazrezugol (KRU)

- Mechel PAO

- Siberian Anthracite

- Reading Anthracite Company

- Blaschak Coal Corporation

- Atlantic Coal Plc

- Lehigh Anthracite

- Jeddo Coal Company

- Vinacomin

- DTEK

- Sadovaya Group

- Xcoal Energy & Resources

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting And Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

In May 2025, MINING investment company Menar bought Springlake Colliery, an anthracite mine previously owned by Mylotex, after the operation was placed under business rescue.

In July 2024, Saint Nicolas Investor Group acquired Blaschak Anthracite. The company’s owners, led by majority shareholder Milestone Partners, have completed the sale of Blaschak in a management-led buyout to Saint Nicholas Investor Group, LLC.

In April 2025, RIE Anthracite Products’ sales marked a growing interest in Schuylkill coal. A Missouri-based company, Guess & Co. Mining, announced the purchase of Rothermel Industrial Enterprises (RIE) Anthracite Products in Branch Township, Schuylkill County, PA.

In July 2024, PT Delta Dunia Makmur Tbk (Delta Dunia Group) completed the strategic acquisition of Atlantic Carbon Group, Inc. (ACG) for US$122.4 million, securing ownership of four producing ultra-high-grade (UHG) anthracite mines in Pennsylvania, USA, and positioning Delta Dunia Group as a pivotal player in the global UHG anthracite market, crucial for the production of low-carbon steel (LC steel).

In August 2022, the Polish state is buying staked in anthracite mine operator Polska Grupa Gornicza (PGG) for a zloty from four state utilities under a conditional deal announced, as Warsaw works to transform the heavily-polluting coal sector.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Anthracite Market based on the below-mentioned segments:

Global Anthracite Market, By Grade

- High Grade

- Standard Grade

- Ultra-High Grade

- Others

Global Anthracite Market, By End Use

- Steel Production

- Energy & Power

- Bricks

- Silicon & Glass

- Others

Global Anthracite Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. What is the market size of the anthracite market?The global anthracite market size is expected to grow from USD 11.50 Billion in 2024 to USD 16.40 Billion by 2035, at a CAGR of 3.28% during the forecast period 2025-2035.

-

2. Which region holds the largest share of the anthracite market?Asia Pacific is anticipated to hold the largest share of the anthracite market over the predicted timeframe.

-

3. What is the forecasted CAGR of the Global Anthracite Market from 2024 to 2035?The market is expected to grow at a CAGR of around 3.28% during the period 2024–2035.

-

4. Who are the top companies that are involved in the Global Anthracite Market?Key players include China Shenhua Energy Company, Yanzhou Coal Mining Company, Kuzbassrazrezugol (KRU), Mechel PAO, Siberian Anthracite, Reading Anthracite Company, Blaschak Coal Corporation, Atlantic Coal Plc, Lehigh Anthracite, Jeddo Coal Company, Vinacomin, DTEK, Sadovaya Group, and Xcoal Energy & Resources.

-

5. What are the main drivers in the anthracite market?An increasing need for anthracite in steel production, use in power generation, and applications in water filtration systems are major market growth drivers of the anthracite market.

-

6. What challenges are limiting the adoption of anthracite?Factors like the increased cost and environmental concerns associated with mining activities remain key restraints in the anthracite market.

-

7. What are the key trends in the anthracite market?The emergence of high grade anthracite in steelmaking (PCI applications) and the use of electrically calcined anthracite in electric vehicle (EV) batteries are major key trends in the anthracite market.

Need help to buy this report?