Global Airborne Electronic Warfare Market Size, Share, and COVID-19 Impact Analysis, By Capability (Electronic Attack, Electronic Protection, Electronic Support and Others), By Platform Type (Manned Aircraft and Unmanned Aircraft), By Frequency Band (HF/ VHF, UHF/L/S, C/X, and Ku/Ka), By Architecture (Pod-Mounted, Internally Integrated, Payload/Pod for UAV and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Aerospace & DefenseGlobal Airborne Electronic Warfare Market Insights Forecasts to 2035

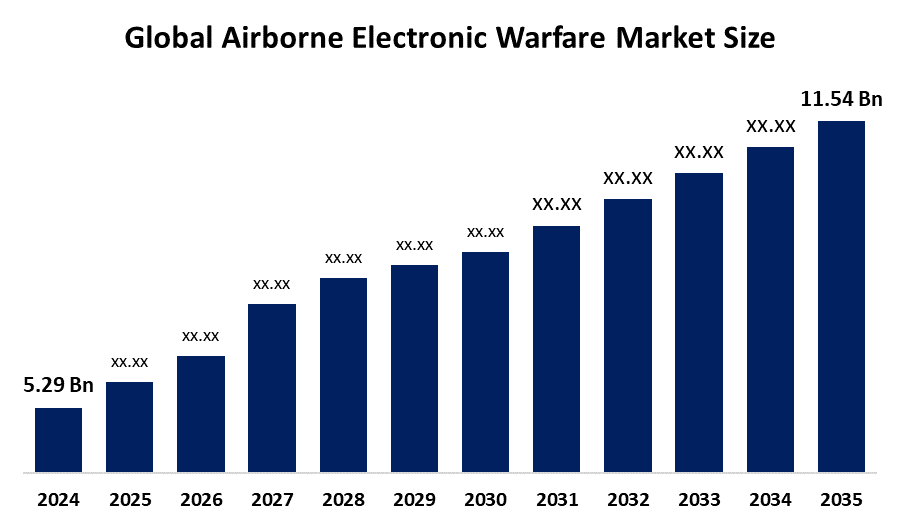

- The Global Airborne Electronic Warfare Market Size Was Estimated at USD 5.29 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 7.35% from 2025 to 2035

- The Worldwide Airborne Electronic Warfare Market Size is Expected to Reach USD 11.54 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a Research Report Published by Spherical Insights and Consulting, The Global Airborne Electronic Warfare Market Size was Worth Around USD 5.29 Billion in 2024 and is Predicted to Grow to Around USD 11.54 Billion by 2035 with a Compound Annual Growth Rate (CAGR) of 7.35% from 2025 to 2035. Rising geopolitical tensions, increased defense spending, and urgent modernization of aircraft are driving the airborne electronic warfare market. Growth is propelled by the integration of AI-powered cognitive jamming, rising UAV deployment, and the need to counter advanced radar threats and signal intelligence.The global airborne electronic warfare (EW) market encompasses advanced systems designed to detect, intercept, disrupt, and protect against threats operating within the electromagnetic spectrum. These include radar jammers, signal intelligence (SIGINT) sensors, and electronic countermeasure (ECM) suites. Such systems are essential for modern military aircraft, enabling capabilities like threat detection, electronic attack, and self-protection—ultimately ensuring mission success and aircraft survivability in highly contested environments.

In February 2026, OCCAR signed a co-funding agreement for the REACT II airborne electronic warfare program, led by Indra, with participation from Spain, Italy, Germany, Sweden, Poland, the Netherlands, and France. This €69 million initiative—partly supported by €40 million from the European Commission—focuses on developing modular EW systems featuring AESA antennas, digital RF memory, and advanced command-and-control (C2) capabilities.Market growth is primarily driven by rising geopolitical tensions and increasing global defense spending, which reached approximately $2.1 trillion in 2023. In parallel, rapid technological advancements—particularly the integration of artificial intelligence (AI) for cognitive jamming and autonomous threat response—are enhancing threat identification accuracy by over 30%.

Significant opportunities are emerging in next-generation GaN-based AESA jammers, lightweight EW payloads for Group 1–3 UAVs, and cognitive electronic warfare powered by machine learning. Additionally, strong demand from Asia-Pacific military modernization programs is further accelerating market expansion.In July 2025, General Dynamics Information Technology (GDIT) secured a $143 million contract from the Naval Air Warfare Center Weapons Division to support airborne electronic warfare platforms. The contract includes engineering, logistics, intelligence analysis, and demonstration services focused on low-cost EW jammers for aircraft, helicopters, and unmanned aerial systems (UAS), aimed at countering advanced radar and missile threats.

Report Coverage

This research report categorizes the Global Airborne Electronic Warfare Market Size based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the airborne electronic warfare market. Recent market developments and competitive strategies, such as expansion, type launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the airborne electronic warfare market.

Global Airborne Electronic Warfare Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 5.29 Billion |

| Forecast Period: | 2024-2035 |

| Forecast Period CAGR 2024-2035 : | 7.35% |

| 2035 Value Projection: | USD 11.54 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 245 |

| Tables, Charts & Figures: | 100 |

| Segments covered: | By Capability ,By Frequency Band |

| Companies covered:: | Elbit Systems Ltd., Northrop Grumman Corporation, Saab AB, BAE Systems plc, Thales Group, Lockheed Martin Corporation, Boeing, L3Harris Technologies, Inc, ASELSAN AS, Israel Aerospace Industries, Leonardo S.p.A., RTX Corporation, and Other Key Players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The Global Airborne Electronic Warfare Market Size is primarily driven by escalating geopolitical tensions and ongoing conflicts, such as the Russia-Ukraine War, which have underscored the critical role of EW in jamming GPS signals and disrupting enemy communications. This has significantly accelerated defense modernization efforts worldwide.Technological advancements are another major driver, particularly the emergence of cognitive EW systems that integrate artificial intelligence (AI) and machine learning. These systems enable real-time threat discrimination and adaptive response capabilities, generating substantial demand across modern air forces.Rising defense budgets further support market growth. For instance, the United States Department of Defense reported a defense budget of approximately $877 billion, reflecting a 3% increase from the previous year. Notably, around $5 billion was allocated specifically for electronic warfare programs in 2024, emphasizing continued investment in next-generation EW capabilities.Additionally, the growing threat from advanced multi-band surface-to-air missile (SAM) systems and sophisticated radar technologies is driving the need for more resilient and agile EW solutions. At the same time, the rapid expansion of unmanned aerial vehicle (UAV) fleets is increasing demand for ultra-lightweight, high-performance EW payloads, further reinforcing global market growth.In September 2025, Collins Aerospace secured a contract from the NATO Communications and Information Agency to deliver its Electronic Warfare Planning and Battle Management (EWPBM) solution. This advanced software provides a Recognized Electromagnetic Picture and Electronic Order of Battle, significantly enhancing NATO’s ability to plan, coordinate, and assess electromagnetic warfare operations.

Restraining Factors

The Global Airborne Electronic Warfare Market Size faces major constraints, including high costs and complex integration, with multi-domain systems increasing development expenses by up to 50%. Supply chain fragility, such as 12 to 18 months' lead times for critical optics, creates bottlenecks. Additionally, strict export controls and regulations delay projects by 18-24 months, hindering market growth.

Market Segmentation

The Airborne Electronic Warfare market share is classified into capability, platform type, frequency band, and architecture.

- The electronic attack segment dominated the market in 2024, approximately 48% and is projected to grow at a substantial CAGR during the forecast period.

Based on the capability, the Global Airborne Electronic Warfare Market Size is divided into electronic attack, electronic protection, electronic support and others. Among these, the electronic attack segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The electronic attack segment led market growth as militaries increasingly require systems to disrupt and neutralize enemy radar, communications, and missile guidance networks. Escalating geopolitical tensions, defense modernization initiatives, and the adoption of advanced technologies such as AI-driven jamming and cognitive electronic warfare have further accelerated its demand, establishing electronic attack as vital for modern operations.

- The manned aircraft segment accounted for the largest share in 2024, approximately 74% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the platform type, the Global Airborne Electronic Warfare Market Size is divided into manned aircraft and unmanned aircraft. Among these, the manned aircraft segment accounted for the largest share in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The segment growth is due to its versatility, operational reliability, and ability to carry advanced electronic warfare (EW) payloads. Rising defense budgets, the need for real-time threat assessment, and the integration of sophisticated jamming and surveillance systems in fighter jets and support aircraft have driven demand, supporting sustained growth in this segment globally.

- The UHF/L/S segment dominated the market in 2024, approximately 41% and is projected to grow at a substantial CAGR during the forecast period.

Based on the frequency band, the Global Airborne Electronic Warfare Market Size is divided into HF/ VHF, UHF/L/S, C/X, and Ku/Ka. Among these, the UHF/L/S segment dominated the market in 2024 and is projected to grow at a substantial CAGR during the forecast period. The segment dominance is attributed to its wide adoption in military communication, radar, and electronic warfare systems. These bands offer superior range, signal penetration, and reliability for jamming, surveillance, and intelligence operations. Increasing demand for multi-band EW systems, advanced electronic countermeasures, and integration in airborne platforms has further fueled the segment’s expansion globally.

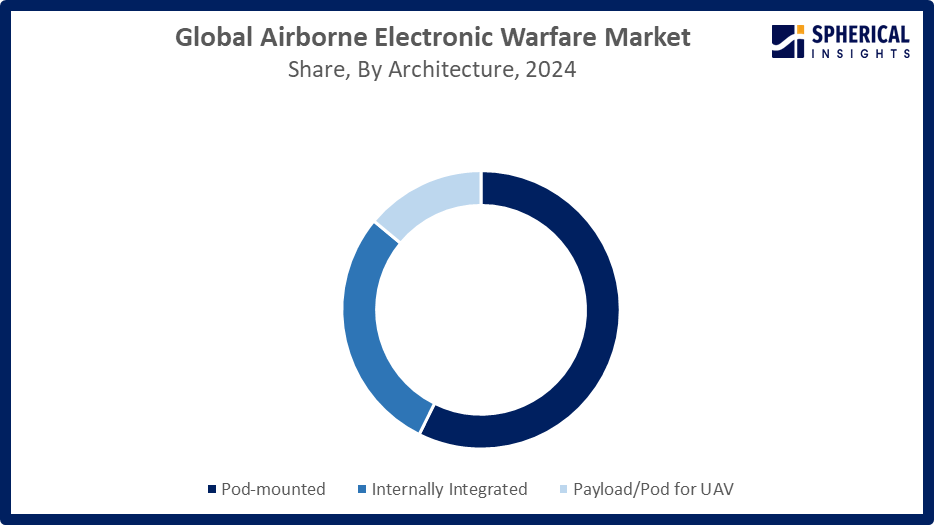

- The pod-mounted segment accounted for the highest market revenue in 2024, approximately 57% and is anticipated to grow at a significant CAGR during the forecast period.

Based on the architecture, the Global Airborne Electronic Warfare Market Size is divided into pod-mounted, internally integrated, payload/pod for UAV, and others. Among these, the pod-mounted segment accounted for the highest market revenue in 2024 and is anticipated to grow at a significant CAGR during the forecast period. The pod-mounted segment market is growing due to its flexibility, ease of integration, and rapid deployment across various aircraft platforms. These systems enable quick upgrades, modular electronic warfare capabilities, and reduced aircraft downtime. Rising demand for adaptable, mission-specific EW solutions in modern air forces has further driven the adoption and growth of pod-mounted platforms globally.

Get more details on this report -

Regional Segment Analysis of the Airborne Electronic Warfare Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the airborne electronic warfare market over the predicted timeframe.

North America is anticipated to hold the largest share of the Global Airborne Electronic Warfare Market Size over the forecast period, accounting for approximately 45% of the total market.The region led the market in 2024, primarily driven by the United States. This dominance is supported by robust defense budgets, advanced military infrastructure, and continuous modernization of both manned and unmanned aircraft equipped with next-generation EW systems.The United States Navy and the United States Air Force are making significant investments in electronic attack platforms such as the EA-18G Growler, along with advanced airborne jamming technologies. Strong research and development capabilities, increased government funding for AI-enabled EW systems, and strategic procurement programs further reinforce North America’s leadership in the market.In March 2026, the United States Navy awarded Boeing a $60.1 million contract for the EA-18G Growler Block II upgrade. This modernization initiative replaces legacy jamming and mission systems with advanced hardware, enhanced EW algorithms, and modular avionics—enabling faster software updates and seamless integration of next-generation electronic attack capabilities.

Get more details on this report -

Asia Pacific is expected to grow at a rapid CAGR in the Global Airborne Electronic Warfare Market Size during the forecast period. The region is rapidly growing in the airborne electronic warfare (EW) market with approximately 28% share, driven primarily by India, Japan, and Australia. Rising geopolitical tensions in the Indo-Pacific region, expansion of air forces, and modernization of both manned and unmanned platforms are key factors. Increasing investments in advanced EW systems, including AI-enabled jammers and modular pod-mounted solutions, along with defense procurement programs, are accelerating adoption, making Asia-Pacific the fastest-growing region globally. In September 2024, China’s Y-9LG electronic warfare (EW) aircraft was highlighted during Falcon Strike 2024 exercises in Thailand. Entering PLAAF service in 2023, the platform features a balance beam radar for long-range jamming, ELINT, and standoff disruption of enemy communications, radar, and navigation systems, advancing China’s EW capabilities.

Europe is witnessing significant growth in the Global Airborne Electronic Warfare Market Size, led by key countries such as Germany, France, and United Kingdom. This growth is driven by rising defense modernization programs, increased integration of advanced EW systems, and strong regional collaboration.The adoption of next-generation technologies—such as Arexis electronic warfare system by Saab and the AGM-88E AARGM missile by Northrop Grumman—is accelerating the region’s capabilities in electronic attack and suppression of enemy air defenses (SEAD). Additionally, collaborative initiatives like the REACT II program are further strengthening Europe’s position in airborne EW innovation.Growing investments in multi-role fighter upgrades and enhanced electronic attack capabilities are also contributing to the region’s expanding market presence.In September 2025, Germany announced plans to award a €1.2 billion ($1.3 billion) contract to Saab and Northrop Grumman for upgrading its Eurofighter Typhoon fleet. The agreement includes integration of Saab’s Arexis electronic warfare system and Northrop Grumman’s AARGM missiles, forming the core of Germany’s new Eurofighter Typhoon EK (electronic combat) variant.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the Global Airborne Electronic Warfare Market Size, along with a comparative evaluation primarily based on their type of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes type development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Elbit Systems Ltd.

- Northrop Grumman Corporation

- Saab AB

- BAE Systems plc

- Thales Group

- Lockheed Martin Corporation

- Boeing

- L3Harris Technologies, Inc

- ASELSAN AS

- Israel Aerospace Industries

- Leonardo S.p.A.

- RTX Corporation

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In March 2026, HawkEye 360 was selected by a European Ministry of Defense for an electronic warfare program valued at up to $75 million. This space-based initiative is designed to enhance sovereign defense planning, operational awareness, and monitoring of complex air defense environments, delivering trusted EW capabilities integrated into national defense frameworks.

- In January 2026, Elbit Systems secured contracts worth $275 million to supply advanced airborne self-protection EW suites to an Asia-Pacific country. The offering includes DIRCM (Directed Infrared Countermeasures) and Mini-MUSIC system solutions, which enhance the survivability of helicopters and light aircraft by detecting, tracking, and countering missile threats through integrated electronic sensing, signal processing, and laser-based countermeasures.

- In November 2025, Airborne Tactical Advantage Company secured a $200 million IDIQ contract to provide Stand-Off Jamming (SOJ) training for the United States Navy and United States Marine Corps through 2030. Using contractor-operated aircraft, ATAC will simulate airborne threats and deliver advanced electronic warfare training, including communications jamming and air defense support across the United States.

- In December 2024, Electronic Attack Squadron 133 completed a five-month deployment with the USS Abraham Lincoln Carrier Strike Group, marking the operational debut of the ALQ-249 Next Generation Jammer on EA-18G Growler platforms. The system, featuring AESA technology and advanced digital software, enhances multi-band jamming capabilities and represents a significant milestone in airborne electronic warfare.

- In December 2024, India’s Defence Acquisition Council (DAC) approved RS21,772 crore for five projects, including the procurement of 31 New Water Jet Fast Attack Crafts and 120 Fast Interceptor Crafts to strengthen coastal defense. The DAC also approved an Electronic Warfare Suite for Su-30 MKI aircraft, enhancing radar protection and overall mission survivability.

- In July 2024, India’s Ministry of Defence signed an MoU to establish three advanced testing facilities in Chennai under the Tamil Nadu Defence Industrial Corridor, focusing on Unmanned Aerial Systems (UAS), Electronic Warfare, and Electro-Optics. With an outlay of RS400 crore, the Defence Testing Infrastructure Scheme aims to boost indigenous defence production and promote self-reliance.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the Global Airborne Electronic Warfare Market Size based on the below-mentioned segments:

Global Airborne Electronic Warfare Market, By Capability

- Electronic Attack

- Electronic Protection

- Electronic Support

Global Airborne Electronic Warfare Market, By Platform Type

- Manned Aircraft

- Unmanned Aircraft

Global Airborne Electronic Warfare Market, By Frequency Band

- HF/ VHF

- UHF/L/S

- C/X

- Ku/Ka

Global Airborne Electronic Warfare Market, By Architecture

- Pod-mounted

- Internally Integrated

- Payload/Pod for UAV

Global Airborne Electronic Warfare Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Frequently Asked Questions (FAQ)

-

1. How are technological innovations like AI and cognitive EW shaping market trends?Technological innovations such as AI and cognitive EW are driving market trends by enabling real-time threat detection, adaptive jamming, and automated responses, increasing demand for next-generation airborne electronic warfare systems globally.

-

2. How is the integration of software-defined and modular EW systems influencing market dynamics?The integration of software‑defined and modular EW systems is transforming market dynamics by enabling rapid capability updates and interoperability, reducing integration costs by up to 30% compared to legacy designs. This shift toward open‑architecture, plug‑and‑play EW platforms enhances responsiveness and adaptability in contested environments, boosting demand for flexible airborne EW solutions across defence forces worldwide

-

3. What role do government initiatives and procurement programs play in market expansion?Government initiatives and procurement programs significantly expand the airborne electronic warfare market by funding modernization and integration of EW systems, with about 58% of global defense modernization programs prioritizing EW acquisition, thereby boosting demand and accelerating technology deployment across military platforms worldwide.

-

4. What is the economic impact of airborne EW systems on defense modernization programs?Airborne EW systems significantly impact defense modernization, representing 10-20% of avionics budgets, driving USD 15-27 billion market growth (2023-2033), boosting R&D, domestic defense industries, and high-skill employment globally

-

5. How is the integration of AESA antennas and digital RF memory influencing product development?The integration of AESA antennas and Digital RF Memory (DRFM) is accelerating product development by enabling rapid electronic beam steering, multi‑frequency operation, and simultaneous jamming functions, enhancing situational awareness and electronic attack capabilities. AESA adoption now represents 63% of revenue in next‑gen radar systems due to superior agility and resilience, while DRFM improves fidelity in signal capture and retransmission, boosting EW effectiveness against diverse threats.

-

6. What are the key trends in modular and pod-mounted EW systems adoption?The adoption of modular and pod‑mounted EW systems is driven by trends toward standardized, plug‑and‑play designs that allow rapid reconfiguration across platforms, reducing downtime and lifecycle costs. Modular pods with adaptive AI/ML capabilities are increasingly used for jamming and signal intelligence, with demand for such systems rising by up to 29% due to defense modernization and contested airspace requirements.

-

7. How are collaborations like REACT II and international co-funding programs impacting innovation?Collaborations like REACT II and international co‑funding programs drive innovation by pooling 20+ partners from 10 countries and €69.7 million in joint funding, accelerating R&D, modular EW system development, and cross‑national technology transfer in electronic warfare. This collective effort shortens development cycles and enhances competitiveness across participating defense industries.

-

8. What role do export control and regulatory compliance play in market dynamics?Export controls and regulatory compliance significantly influence airborne EW market dynamics by limiting international sales and technology transfer. Approximately 35-40% of potential contracts face delays due to ITAR, EAR, and national security regulations, affecting procurement timelines and global adoption rates.

Need help to buy this report?