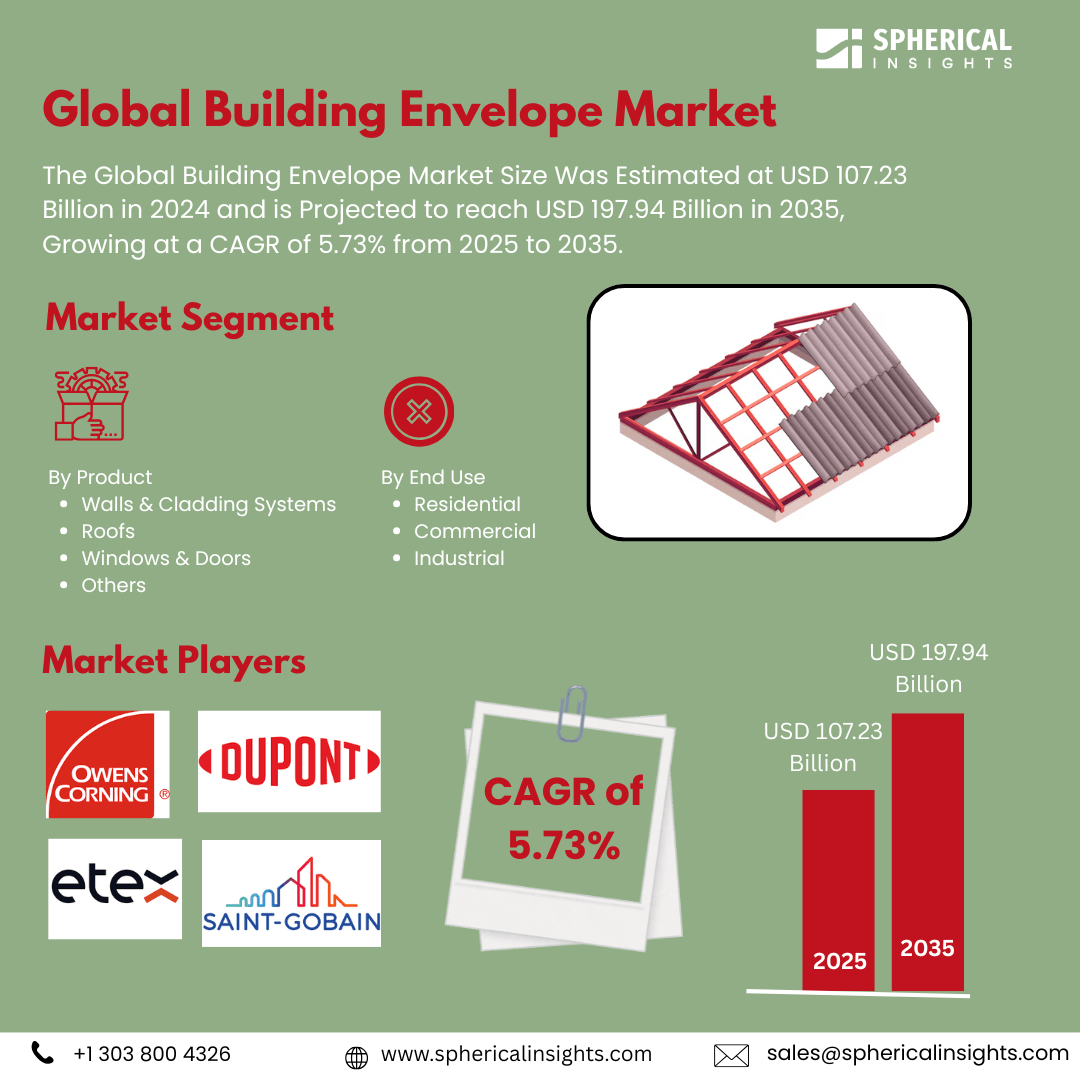

Building Envelope Market Summary

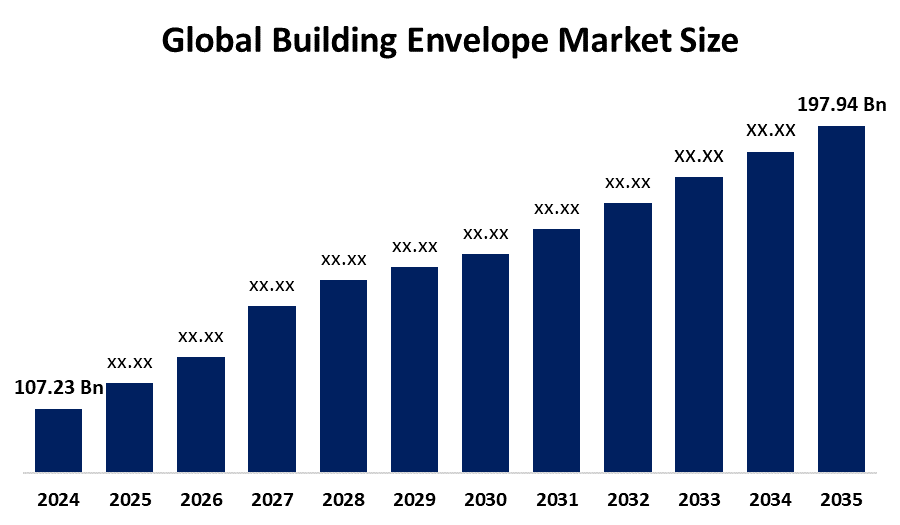

The Global Building Envelope Market Size Was Estimated at USD 107.23 Billion in 2024 and is Projected to reach USD 197.94 Billion in 2035, Growing at a CAGR of c% from 2025 to 2035. Rapid urbanization, which leads to increased construction and renovation activities, strict government rules encouraging sustainable construction, and rising energy efficiency demand are the main factors propelling the building envelope market's expansion.

Key Regional and Segment-Wise Insights

- In 2024, North America held the greatest revenue share of 31.2% in the global building envelope market.

- With a revenue market share of 37.4% in 2024, the walls & cladding systems sector led the industry by product.

- In 2024, the residential category accounted for 41.5% of total revenue by end use.

Global Market Forecast and Revenue Outlook

- 2024 Market Size: USD 107.23 Billion

- 2035 Projected Market Size: USD 197.94 Billion

- CAGR (2025-2035): 5.73%

- North America: Largest market in 2024

The Building Envelope Market Size is the segment of the construction industry that targets structural components that separate the interior from external environments through walls, roofs, windows, doors, and foundation systems. The building envelope controls heat movement and air movement, moisture transfer, and light penetration, which directly impacts structural durability and occupant well-being and energy-saving capabilities. The building envelope market grows because of stricter building codes to reduce carbon emissions, together with increased urbanization and rising demand for energy-efficient buildings. The increasing recognition of sustainable practices and cost reduction goals for residential and commercial buildings supports the implementation of advanced building envelope solutions for both new builds and renovations.

Technological progress serves as a major driving force that shapes the current market for building envelopes. The construction industry uses innovative materials such as prefabricated envelope systems along with dynamic glazing and vacuum insulation panels to enhance thermal performance and decrease energy consumption. The market also favors smart building envelopes, which feature integrated sensors and adaptable operational capabilities. Governments around the world promote energy-efficient building construction by providing incentives and subsidies and implementing LEED, BREEAM, and Energy Star certification standards. The market expansion occurs because programs encourage investment in high-performance envelope technologies, which mainly target sustainable urban development areas and carbon neutrality goals.

Product Insights

The walls and cladding systems category dominated the building envelope market during 2024 by generating 37.4% of total revenue. Walls and cladding systems dominate the building envelope market because they provide essential structural support, together with weather protection and thermal insulation, and decorative attributes to buildings. The demand for energy-efficient and visually appealing facades in residential and commercial construction has caused advanced cladding materials, including vented façade systems, insulated panels, and high-performance composites, to gain popularity. The increasing investment in urban development, along with infrastructure projects in emerging economies, has driven the adoption of long-lasting, eco-friendly wall systems. Regulations concerning building fire protection and insulation standards help drive growth for this segment.

During the forecast period, the building envelope market's windows and doors segment will achieve the fastest CAGR. The increasing demand for smart energy-efficient window and door systems that improve thermal insulation and reduce energy consumption while enhancing indoor comfort drives this sector's growth. The rising popularity of automated shading systems, together with triple glazing and low-E glass, has gained momentum in both residential and commercial construction projects. The combination of strict energy standards with rising sustainability awareness drives the growing market demand for high-performance fenestration solutions. The fast-paced expansion of international markets for this segment occurs because of rising rehabilitation projects combined with government programs that support window and door modernization using energy-efficient solutions.

End-use Insights

The residential segment of the building envelope market held the largest revenue share of 41.5% during 2024. Worldwide housing demand growth, along with rapid city development and growing residential investment, particularly in developing nations, drives this market leadership. Homeowners, along with developers, have started using advanced building envelope solutions because they focus more on sustainability and thermal comfort, and energy efficiency. The market offers weather-resistant roofing systems together with high-performance windows and insulated walls to enhance building performance and reduce energy expenses. The residential sector has experienced rising demand for modern building envelope systems because government incentives for energy-saving home improvements and green construction standards have become more prevalent.

The commercial sector of the building envelope market will register the fastest CAGR during the forecast period. The increasing investments into office buildings and retail establishments and hotels, and institutional facilities, which require advanced building envelope solutions to enhance comfort and energy efficiency, drive this market growth. Commercial buildings are adopting advanced materials, including double-skin façades, dynamic glazing, and smart window technology to meet energy regulations and sustainability goals. The rising focus on better indoor air quality, together with decreased operating expenses, generates increased demand for these products. The worldwide adoption of high-performance commercial building envelopes receives support from government programs which back LEED and BREEAM certification and from expanding corporate centers and rapid urbanization trends.

Regional Insights

The worldwide building envelope market is dominated by the North America region with the highest revenue share of 31.2% in 2024. The leadership of this region stems from its focus on energy-efficient construction methods, along with strict building regulations and widespread adoption of sustainable building practices. Large-scale investments target both new construction and building modernization projects across commercial and residential spaces in the United States and Canada. The market growth accelerates because governments provide incentives for green buildings, while consumers have high awareness, and builders use modern construction technology. The building envelope market leadership of North America becomes more established through its major industry players and the rising need for intelligent high-performance building materials, which drives both innovation and adoption across the region.

Asia Pacific Building Envelope Market Trends

The Asia Pacific building envelope market is expected to grow at a significant rate throughout the forecast period because of fast urbanization, together with infrastructure development and increasing construction activities across China, India, and Southeast Asia. The rising acceptance of building envelope technologies stems from government initiatives to promote sustainable development, combined with increasing market interest in energy-efficient structures. The market growth receives additional impetus from expanding middle-class demographics and rising demand for residential and commercial infrastructure development. The adoption rate of innovative materials such as insulated panels, together with modern façade systems and energy-efficient windows, increases because of beneficial regulations and growing foreign capital investments, along with smart urban development programs. The main driver behind this growing trend originates from regional efforts to decrease energy consumption and optimize building efficiency.

Europe Building Envelope Market Trends

The building envelope market in Europe keeps expanding because of environmental regulations and strict energy rules, together with construction standards that maintain a high reputation. Germany and France, together with the UK, lead the adoption of advanced envelope technology because they aim to meet EU environmental targets and reduce building-related carbon emissions. The shift toward net-zero energy buildings, along with the need to fix existing infrastructure, drives people to select high-performance roofs, windows, and walls. The combination of government funding and BREEAM and Passive House building codes supports sustainable construction practices. The European focus on intelligent energy-saving building envelope solutions moves forward because of smart building development and modern architectural design principles.

Key Building Envelope Companies:

The following are the leading companies in the building envelope market. These companies collectively hold the largest market share and dictate industry trends.

- Saint-Gobain

- Etex Corp

- Owens Corning

- DuPont de Nemours

- Rockwool International

- BASF SE

- Kingspan Group

- Sika AG

- 3M Company

- GAF Materials Corporation

- Others

Recent Developments

- In June 2025, Gulf Additive Factory LLC was purchased by Sika in the State of Qatar. The purchase solidifies Sika's position in the nation and offers promising prospects for future growth.

- In January 2025, Saint-Gobain strengthened its global presence in building chemicals by completing the acquisition of OVNIVER Group in Mexico and Central America.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the building envelope market based on the below-mentioned segments:

Global Building Envelope Market, By Product

- Walls & Cladding Systems

- Roofs

- Windows & Doors

- Others

Global Building Envelope Market, By End Use

- Residential

- Commercial

- Industrial

Global Building Envelope Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa