Top 15 Companies in the Global Bio-based Polyurethane Market (2024–2035): Spherical Insights Analysis

RELEASE DATE: Mar 2026 Author: Spherical InsightsRequest Free Sample Speak to Analyst

Introduction

Bio-based Polyurethane (PU) is a sustainable polymer engineered by replacing traditional petroleum-derived polyols and isocyanates with renewable feedstocks such as castor oil, soybean oil, or wood-derived lignin. This shift in molecular architecture allows for the creation of high-performance foams and coatings that maintain the same durability as fossil-fuel plastics while significantly lowering the carbon footprint of the manufacturing process. As we move into the 2024–2035 forecast period, this material evolved from a niche green alternative into a strategic industrial necessity powered by Green Chemistry advancements in resin engineering. These technologies now enable bio-based PU to match the rigorous standards required for high-stakes use cases, including high-resiliency automotive seating and ultra-efficient rigid building insulation. The momentum is further accelerated by recent government initiatives, such as the EU Bioeconomy Strategy 2025 and the U.S. Sustainable Procurement Mandates, which provide the regulatory framework and financial incentives for massive industrial scale-up. The ultimate impact of this transition is a fundamental decoupling of the global plastics industry from crude oil, projected to push market volume to over 11 million metric tons by 2035 while slashing sector-wide emissions.

Navigate Future Markets with Confidence: Insights from Spherical Insights LLP

The insights presented in this blog are derived from comprehensive market research conducted by Spherical Insights LLP, a trusted advisory partner to leading global enterprises. Backed by in-depth data analysis, expert forecasting, and industry-specific intelligence, our reports empower decision-makers to identify strategic growth opportunities in fast-evolving sectors. Clients seeking detailed market segmentation, competitive landscapes, regional outlooks, and future investment trends will find immense value in the full report. By leveraging our research, businesses can make informed decisions, gain a competitive edge, and stay ahead in the transition toward sustainable and profitable solutions.

Unlock exclusive market insights—Download the Brochure now and dive deeper into the future of the Bio-based Polyurethane Market.

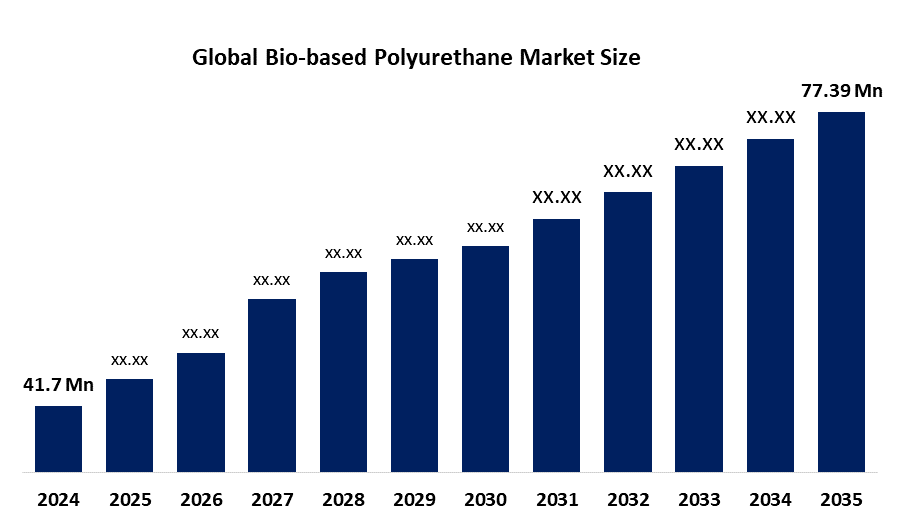

Global Bio-based Polyurethane Market Size & Statistics

- The Global Bio-based Polyurethane Market was estimated to be worth USD 41.7 Million in 2024.

- The market is projected to expand at a robust CAGR of 5.78% between 2024 and 2035.

- The Global Bio-based Polyurethane Market Size is anticipated to reach USD 77.39 Million by 2035.

- Europe is identified as the region with the highest revenue demand for bio-based polymers. This is primarily fuelled by stringent Green Deal regulations and circular economy mandates that require industries to replace fossil-fuel plastics with renewable alternatives, particularly in Germany and France.

- Asia-Pacific is identified as the fastest-growing region, with growth spearheaded by China’s massive shift toward sustainable manufacturing and India’s rapid infrastructure development, where bio-based rigid foams are increasingly used for energy-efficient building insulation.

Regional Growth & Demand Analysis

Europe is the Highest Revenue region through 2035, maintaining its global lead through a rigorous transition toward a circular economy. Growth is centered on the European Green Deal and the 2025 EU Bioeconomy Strategy, which have turned sustainable material procurement into a legal necessity rather than a corporate choice. With major chemical hubs in Germany and France scaling up production of plant-derived polyols, the region is seeing a massive shift in the construction and automotive sectors. The dominance of the European market is sustained by high demand for Energy-Efficiency Class A building insulation and the integration of carbon-neutral foams in the luxury mobility sector, where brands like BMW and Mercedes-Benz are mandating bio-content in every interior component.

Asia-Pacific is the fastest-growing region in this sector, driven by its dual role as the world’s primary manufacturing hub and the leader in rapid urbanization. The surge is fueled by China’s 14th Five-Year Plan, which prioritizes Green Manufacturing, and India’s Smart Cities Mission, which is driving unprecedented demand for bio-based rigid insulation foams and sustainable coatings. As regional giants like Wanhua Chemical and Mitsui Chemicals expand their bio-PU capacities, Asia-Pacific becomes the global epicenter for high-volume, cost-effective sustainable innovation. This growth is effectively bridging the gap between mass-market affordability and high-performance Green Chemistry, particularly in the electronics and footwear industries.

Global Bio-based Polyurethane Market Segmentation

The Global Bio-based Polyurethane Market is segmented By Product Type (Flexible Foam, Rigid Foam, Coatings, Adhesives & Sealants, and Elastomers), End-User Industry (Building & Construction, Furniture & Bedding, Automotive, Footwear & Textile, and Packaging), and Raw Material Source (Castor Oil, Soybean Oil, Rapeseed Oil, and Other Bio-based Polyols). The analysis also provides a comprehensive geographic breakdown across major regions (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa), offering a detailed strategic forecast for the 2024–2035 period.

Ready to lead the Bio-based Polyurethane Market ?

Discover the regional trends and growth factors shaping the industry. We’re here to assist with expert, personalized data.

Call +1 303 800 4326 or Send us a message for a personalized consultation.

Top 10 Trends in the Global Bio-based Polyurethane Market

- Mass-Balance Decoupling from Crude Oil

- Transition to 2nd-Generation Non-Food Feedstocks

- Rise of CO2-to-Polyol Carbon Capture Technology

- Adoption of Non-Isocyanate Polyurethane (NIPU) Chemistries

- Integration of Bio-PU in High-Efficiency Net-Zero Building Insulation

- Development of Zero-VOC and Waterborne Bio-based Coatings

- Lightweighting Foams for Extended Electric Vehicle (EV) Range

- Expansion of Circular Chemical Upcycling for End-of-Life PU

- Shift Toward Lignin-Based Rigid Foams for Industrial Durability

- Growth of Smart, Bio-based Encapsulation for Wearable Electronics

- Mass-Balance Decoupling from Crude Oil

The industry is moving away from traditional petroleum-dependent production toward Mass Balance accounting, which allows manufacturers to mix renewable and fossil feedstocks during the early stages of chemical processing. While industrial polyurethane was once synonymous with crude oil derivatives, leading chemical giants like BASF and Covestro are now using this methodology to drop bio-based precursors directly into existing value chains without compromising material performance. This transition allows companies to maintain the high mechanical strength of traditional PU while significantly reducing their scope 3 emissions, effectively decoupling industrial growth from fossil fuel volatility.

- Transition to 2nd-Generation Non-Food Feedstocks

There is a decisive shift occurring in raw material sourcing, moving from first-generation food crops like corn and soy toward second-generation waste-based feedstocks. By utilizing non-edible resources such as castor oil, used cooking oil (UCO), and agricultural residues, the bio-based PU market is resolving the ethical food vs. fuel debate that previously limited its expansion. These advanced feedstocks provide a more stable pricing structure and a superior sustainability profile, making bio-PU a more attractive investment for industries under intense ESG scrutiny, such as the global footwear and textile sectors.

- Rise of CO2-to-Polyol Carbon Capture Technology

One of the most disruptive innovations in Green Chemistry is the commercialization of polyols derived directly from captured CO2 emissions. Instead of relying solely on plant-based biology, companies are now using carbon-capture-and-utilization (CCU) technology to transform industrial waste gases into high-quality polyurethane foam components. This trend turns a primary environmental pollutant into a valuable raw material, allowing for the production of Carbon-Negative foams for mattresses and automotive interiors, which represents the ultimate frontier in the circular economy.

- Adoption of Non-Isocyanate Polyurethane (NIPU) Chemistries

The industry is aggressively pursuing the development of Non-Isocyanate Polyurethanes (NIPUs) to eliminate the health and environmental risks associated with traditional isocyanates. While standard PU long relied on these toxic precursors, recent breakthroughs in cyclic carbonate and amine chemistry are allowing for the creation of Isocyanate-Free bio-polymers. These NIPU materials offer enhanced thermal stability and chemical resistance, providing a safer, high-performance alternative for use in sensitive indoor environments, medical devices, and high-wear industrial coatings.

- Integration of Bio-PU in High-Efficiency Net-Zero Building Insulation

As global building codes pivot toward Net-Zero standards, bio-based rigid polyurethane foams have become the primary solution for extreme thermal insulation. Unlike traditional fiberglass or mineral wool, bio-based spray foams and sandwich panels provide a superior airtight seal with a significantly lower embodied carbon footprint. By integrating renewable lignin and vegetable-based polyols into rigid foam structures, the construction industry is able to achieve the strict R-values required for energy-efficient architecture while simultaneously meeting the demand for non-toxic, sustainable building materials.

Empower your strategic planning:

Stay informed with the latest industry insights and market trends to identify new opportunities and drive growth in the bio-based polyurethane market. To explore more in-depth trends, insights, and forecasts, please refer to our detailed report.

Unlock exclusive market insights—Download the Brochure now and dive deeper into the future of the Bio-based Polyurethane Market.

Top 15 Companies Shaping the Global Bio-based Polyurethane Market

- BASF SE

- Covestro AG

- Huntsman International LLC

- The Dow Chemical Company

- Cargill, Incorporated

- Mitsui Chemicals, Inc.

- The Lubrizol Corporation

- Wanhua Chemical Group Co., Ltd.

- Arkema S.A.

- Rampf Holding GmbH & Co. KG

- Stahl Holdings B.V.

- Alberdingk Boley GmbH

- Miracll Chemicals Co., Ltd.

- Woodbridge Foam Corporation

- MCNS (Mitsui Chemicals & SKC Polyurethanes)

- BASF SE

Headquarters: Ludwigshafen, Germany

The undisputed global leader in chemical diversity, BASF is driving the bio-PU transition through its sophisticated Biomass Balance approach. Unlike traditional manufacturers, BASF integrates renewable feedstocks at the very beginning of its production cycle, allowing them to offer certified bio-based versions of their famous Elastopan and Cosmotherm lines. By 2030, BASF aims to decouple its entire PU portfolio from fossil-based precursors, ensuring that their high-performance foams for the footwear and automotive sectors meet the strictest global Net-Zero mandates without requiring customers to retool their existing machinery.

- Covestro AG

Headquarters: Leverkusen, Germany

Covestro positioned itself as the Circular Economy pioneer of the polyurethane world, specifically through its aggressive investment in CO2-to-Polyol technology. Their cardyon brand represents a breakthrough in sustainable chemistry, where up to 20% of traditional petroleum is replaced by captured industrial carbon dioxide. Following their integration of DSM’s Resins & Functional Materials, Covestro now commands a massive share of the bio-based coating market, focusing on waterborne PU systems that eliminate toxic solvents while delivering the premium, high-gloss finishes required by the luxury consumer electronics and automotive industries.

- Huntsman International LLC

Headquarters: The Woodlands, Texas, USA

A dominant force in the MDI (Methylene Diphenyl Diisocyanate) space, Huntsman is redefining industrial durability through its ACOUSTIFLEX VIO and DALTOFOAM bio-based systems. Their 2035 strategy is centered on the Waste-to-Value pipeline, where they utilize high percentages of recycled PET and bio-derived polyols to create rigid insulation foams for the construction sector. By focusing on the thermal efficiency of the global building envelope, Huntsman is effectively bridging the gap between high-performance structural materials and radical carbon footprint reduction.

- The Dow Chemical Company

Headquarters: Midland, Michigan, USA

Dow is leveraging its massive Scale for Good to mainstream bio-based PU through its RENUVA Circular Economy Program. Their specialty lies in the large-scale production of polyols derived from both renewable vegetable oils and chemically recycled mattress foams. As a primary supplier to the global furniture and bedding industry, Dow’s focus through 2035 is the Closed-Loop foam cycle, ensuring that the polyurethane in home furnishings can be broken down and reborn as new, bio-attributed material, significantly reducing the landfill impact of the comfort-wear industry.

- Cargill, Incorporated

Headquarters: Minnetonka, Minnesota, USA

As a global leader in agricultural supply chains, Cargill is the primary Ingredient Architect of the bio-polyurethane market. Through their BiOH polyols brand, they provide the essential plant-based building blocks primarily derived from soybean and castor oil that other chemical firms use to create sustainable foams. Cargill’s strategic advantage for the 2035 forecast lies in its vertical integration; by controlling the feedstock from the field to the refinery, they offer the most cost-stable and ethically sourced bio-polyols for the automotive seating and bedding markets globally.

Are you ready to discover more about the Bio-Based Polyurethane Market?

The report provides an in-depth analysis of the leading companies operating in the global bio-based polyurethane market. It includes a comparative assessment based on their product portfolios, business overviews, geographical footprint, strategic initiatives, market segment share, and SWOT analysis. Each company is profiled using a standardised format that includes:

Unlock exclusive market insights—Download the Brochure now and dive deeper into the future of the Bio-based Polyurethane Market.

Company Profiles

- BASF SE

- Business Overview

- Company Snapshot

- Products Overview

- Company Market Share Analysis

- Company Coverage Portfolio

- Financial Analysis

- Recent Developments

- Merger and Acquisitions

- SWOT Analysis

- Covestro AG

- Huntsman International LLC

- The Dow Chemical Company

- Cargill, Incorporated

- Mitsui Chemicals, Inc.

- The Lubrizol Corporation

- Wanhua Chemical Group Co., Ltd.

- Arkema S.A.

- Rampf Holding GmbH & Co. KG

- Stahl Holdings B.V.

- Alberdingk Boley GmbH

- Miracll Chemicals Co., Ltd.

- Woodbridge Foam Corporation

- MCNS (Mitsui Chemicals & SKC Polyurethanes)

Conclusion

The global bio-based polyurethane market is witnessing a profound shift as industrial performance and environmental stewardship finally converge through a Green Chemistry philosophy. This transition is defined by molecular-level engineering and carbon-capture innovations that transform traditional polymers into carbon-sequestering assets for the construction and automotive sectors. As manufacturers pivot toward 2nd-generation feedstocks and isocyanate free formulations, the material landscape is being redefined as a sustainable, high-performance foundation for the next generation of global infrastructure. With synchronized efforts from global regulators and material innovators to develop circular, net-zero solutions, the market is set for rapid evolution. This shift offers a unique opportunity for brands to redefine their supply chain resilience through renewable textures and structural foams that are as technologically sophisticated as the high-tech industries they support.

Our Report

https://www.sphericalinsights.com/reports/italy-seed-treatment-market

https://www.sphericalinsights.com/reports/italy-compound-feed-market

https://www.sphericalinsights.com/reports/italy-data-center-market

https://www.sphericalinsights.com/reports/italy-food-colorants-market

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI. Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?