Iran - Israel - US War and Fighter Jet Importance with Top Manufacturing Companies Analysis: Spherical Insights Analysis

RELEASE DATE: Mar 2026 Author: Spherical InsightsRequest Free Sample Speak to Analyst

Article summary

The war between Iran, Israel, and the United States intensified dramatically, with missile strikes, drone warfare, and territorial disputes extending throughout the Middle East. As fighter jets integrate with drones and missile defence systems to provide quick strike capability, deterrence, and control of contested airspace, air power has become crucial to the war. Along with US deployments of F-15EX and naval aviation, Israel's F-35s and improved F-16s have highlighted the critical role that cutting-edge aircraft play in determining war results. Globally, the conflict has caused trade routes to be disrupted, oil and gold prices to soar, and defence stocks for firms like Lockheed Martin, Boeing, and Israel Aerospace Industries to rise. The US and Israel are supported by Western allies, but China and Russia denounce the strikes, creating a sharp geopolitical rift.

Navigate Future Markets with Confidence: Insights from Spherical Insights LLP

The insights presented in this blog are derived from comprehensive market research conducted by Spherical Insights LLP, a trusted advisory partner to leading global enterprises. Backed by in-depth data analysis, expert forecasting, and industry-specific intelligence, our reports empower decision-makers to identify strategic growth opportunities in fast-evolving sectors. Clients seeking detailed market segmentation, competitive landscapes, regional outlooks, and future investment trends will find immense value in the full report. By leveraging our research, businesses can make informed decisions, gain a competitive edge, and stay ahead in the transition toward sustainable and profitable solutions.

Unlock exclusive market insights-Download the Brochure now and dive deeper into the future of the Point of Entry Water Treatment System Market.

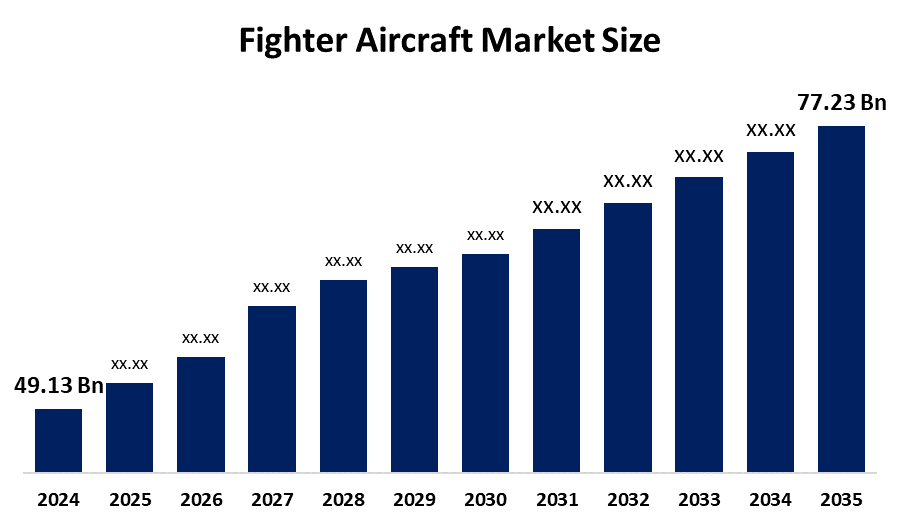

Current Market Size and Global Market Growth

Global markets in the next few years will be shaped by rising demand pressures and intensifying regional conflicts. The demand for fighter aircraft is rising as a result of increased defence budgets and increased focus on the development of unmanned combat aerial vehicles (UCAVs). Energy flows, commercial routes, and investor confidence are anticipated to be influenced by this industry and recent tensions between Iran and the United States, Russia and Europe, and India and Pakistan. The dispute between the United States, Israel, and Iran in particular has the potential to develop into a protracted battle that would destabilise the Middle East and raise oil prices.

- The Global Fighter Aircraft Market Size is projected to Grow USD 49.13 Billion in 2024.

- The Fighter Aircraft Market Size is expected to reach at USD 77.23 Billion in 2035.

- The Fighter Aircraft Market is expected to grow at a CAGR of 4.2% during the forecast period 2025–2035.

- North America is anticipated to generate the highest demand during the forecast period in the Fighter Aircraft Market.

- Asia-Pacific is predicted to grow the fastest during the forecast period in the Fighter Aircraft Market.

Why are fighter jets important in modern-day conflict?

Control of the sky determines the success of both offensive and defensive operations, making air superiority the crucial aspect in the Iran-Israel-US conflict. Fighter jets are using sophisticated stealth and electronic warfare systems to carry out precision strikes against Iranian missile sites, leadership positions, and nuclear facilities. In addition to being combat assets, the US deployments of F-35s and F-15EX aircraft serve as potent deterrent signals that reassure allies and alert adversaries. Simultaneously, these aircraft are closely linked with drones and air defence systems to provide a multi-layered approach in which jets execute quick strikes and work with missile interceptors, while UAVs support surveillance and targeting. This synergy highlights how the rising conflict is being shaped by modern aerial warfare.

How significant are fighter aircraft as a measure of military power in the current conflict?

In the ongoing Iran–Israel–US war, several fighter jets have become central to shaping the aerial battlefield. The F-35 Lightning II from Lockheed Martin is being deployed by Israel and the US for stealth operations and electronic warfare, giving them a decisive edge in penetrating Iranian defences. The F-15EX from Boeing is handling heavy strike missions and air dominance roles, crucial for sustaining long-range engagements. Israel’s upgraded F-16s and UAVs, developed with Israel Aerospace Industries, are tailored for local conditions, combining precision strikes with drone integration. Further, Iran's fleet of Russian-made Sukhoi Su-35s and domestically improved F-14 Tomcats, coupled with earlier MiG-29s and F-4 Phantoms still in service, has been crucial to the present Iran–Israel–US conflict. MiG-29s and F-4s are used for defensive patrols and strike operations; they are limited in their ability to counter Israel's stealth F-35s and US F-15EX aircraft.

Competitive Analysis: Aerospace Military Strength of Current Countries in Conflict

• USA

The USA has 1 TvF rank in the aerospace defence sector with more than 5000 aircraft models. The US fighter jet market is the largest in the world and a major component of US defence spending. The US maintains air dominance with a defence budget of more than $850 billion, and its exports of fighter jets, especially the F-35, influence international defence markets, strengthening alliances and projecting force in confrontations like the Iran-Israel-US war. RTX Corporation, Boeing, and Lockheed Martin are the top three U.S. aerospace and military corporations in 2026; Northrop Grumman and General Dynamics complete the world's top. These companies lead the industry in terms of market capitalisation and sales, spurring advancements in space, aircraft, and defence technology. Further, Lockheed Martin's F-35 Lightning II is a stealth multirole jet essential to both allied and domestic forces. Heavy strike and carrier operations are still dominated by Boeing's F-15EX and F/A-18 Super Hornet. The development of next-generation systems, such as the sixth-generation F-47 fighter, which is a component of the Air Force's Next Generation Air Dominance (NGAD) program, and modernisation initiatives are driving this expansion.

• Israel

In terms of absolute spending, Israel's defence market is estimated to be worth $49.8 billion in 2026, placing it 10th in the world and accounting for 8%, one of the highest percentages internationally. The country has around 300–340 active fighter aircraft, making it a dominant air power in the region with highly modernised platforms and strong integration of advanced avionics and defence systems. The Israel Defence Industry (IDI) employs 15,000 people, produces about 70% of combat aircraft components, including UAVs and advanced avionics, and generates approximately $12 billion annually. About 15% of all arms sales worldwide are made up of exports, with the US, India, Russia, Ukraine, and China being the main purchasers. Israel Aerospace Industries (IAI), Rafael Advanced Defence Systems, Elbit Systems, IMI Systems (now a part of Elbit), and Aeronautics Ltd. are the five leading businesses in Israel's aerospace and defence sector. Israel's defence exports, which have increased from $8 billion to more than $15 billion in recent years, are dominated by these companies. With its F-35 fleet, missile defence systems like Iron Dome and Arrow, and UAV integration, Israel continues to prioritise air superiority, strengthening its impact in both domestic security and international defence.

• Iran

Iran ranks around 18th globally in the defence sector. Iran has around 150–231 fighter jets in its total inventory. Iran's military market is expected to develop steadily despite sanctions, with a valuation of approximately $7.3 billion in 2026, with 2.6%. In the ongoing conflict between Iran, Israel, and the United States, Iran uses a combination of Russian Su–35s, older F–14 Tomcats, MiG–29s, and F–4 Phantoms in addition to enhanced domestic UAVs for surveillance and targeted strikes. This capability is maintained by local businesses. Iran Electronics Industries (IEI) provides avionics, PANHA concentrates on helicopter support, and HESA (Iran Aircraft Manufacturing Industries Co.) manages aircraft manufacture and modifications. While companies like Meraj Air and Parsun Aviation assist with maintenance and logistics, umbrella organisations like IAIO oversee national aerospace programs. In a high-stakes regional crisis, these businesses work together to maintain Iran's mixed-generation fleet while balancing scarce resources with local innovation.

Recent Developments according to regional analysis

North America

In February 2026, DARPA’s LongShot program, now designated the X-68A, cleared key technical milestones and is moving toward flight testing in 2026, marking a major step in revolutionising air combat with air launched, uncrewed aircraft. DARPA’s LongShot X-68A is on the horizon for flight testing in 2026, after clearing critical safety and performance checks. This program represents a leap toward uncrewed, air launched systems that could redefine future aerial warfare.

In January 2026, Mexico officially became the first Latin American operator of the C-130J Super Hercules airlifters, marking a significant modernisation step for its air force. The acquisition enhances Mexico’s strategic airlift capacity, enabling faster troop deployment, humanitarian missions, and disaster relief operations. The C-130J, built by Lockheed Martin, offers advanced avionics, greater fuel efficiency, and increased payload compared to older C-130 variants.

In January 2023, Canada’s Future Fighter Capability Project will replace its aging CF 18 fleet with 88 advanced F-35A jets, marking the country’s largest air force investment in over 30 years. The program is valued at about $27.7 billion, with first deliveries expected in 2026. Future Fighter Capability Project ensures long term air defence with 88 F 35As, boosting national security, allied commitments, and domestic aerospace industry growth. First jets arrive in 2026 for training, with Canadian deployment starting in 2028.

Europe

In March 2026, The French German Future Combat Air System (FCAS) program is faltering, with Dassault accusing Airbus of causing delays and mismanagement. Once envisioned as Europe’s flagship sixth generation fighter initiative, the project now faces uncertainty, raising doubts about its viability and Europe’s defence ambitions.

In February 2026, Germany had considered increasing its purchase of F-35A Lightning II fighter jets from the United States, reflecting heightened security concerns and a drive to modernise its air force. The move underscored Berlin’s NATO commitments and pursuit of advanced airpower integration.

In July 2025, the UK unveiled a prototype design for its sixth generation Tempest fighter jet, a cornerstone of the Future Combat Air System program. Developed by BAE Systems with Rolls Royce, Leonardo, and MBDA, Tempest promises advanced stealth, AI integration, and drone swarming capabilities, reinforcing Britain’s long term airpower ambitions.

Asia Pacific

In February 2026, India approved a multi billion dollar proposal to acquire 114 Rafale fighter jets from France’s Dassault Aviation, valued at about RS3.6 trillion (USD 39.7 billion). This marks a major boost to the Indian Air Force’s combat capability and deterrence power.

In January 2026, China’s upgraded J-20A “5+ generation” fighter entered landmark testing in early 2026, featuring the long awaited WS 15 engines, enhanced avionics, and manned unmanned teaming capabilities. This marks a major leap in China’s airpower, aiming to rival the U.S. F-22 and F-35.

In December 2025, Japan finalised the details of its future sixth generation fighter program, developed jointly with the United Kingdom and Italy under the Global Combat Air Programme (GCAP). The project aims to deliver a highly advanced stealth fighter by the mid 2030s, integrating artificial intelligence, drone teaming, and next generation sensors. This trilateral collaboration strengthens defence ties among the three nations while ensuring interoperability with allied forces.

Middle East and South Africa

In January 2026, Israel signed a contract to acquire 25 F-15IA fighter aircraft from Boeing, marking a major expansion of its air force capabilities. The deal strengthens Israel’s long range strike power and complements its existing fleet of F-35s and F-15 variants. The F 15IA, an advanced version tailored for Israel, features upgraded avionics, extended range, and enhanced payload capacity, making it one of the most powerful multirole fighters in the region.

In January 2025, the United Arab Emirates officially received its first Rafale fighter jet, marking a milestone in its USD19 billion deal with France’s Dassault Aviation. The delivery strengthens the UAE Air Force’s modernisation drive, adding advanced multirole capabilities with superior avionics, stealth features, and long range strike capacity. This acquisition underscores Abu Dhabi’s strategic partnership with France and positions the UAE as a leading operator of next generation fighters in the Middle East.

Top 10 Companies Major the Fighter Aircraft Market

- Airbus Defence and Space

- BAE Systems

- Boeing Defence, Space & Security

- Dassault Aviation

- Lockheed Martin Corporation

- Mitsubishi Heavy Industries

- Northrop Grumman Corporation

- Russian Aircraft Corporation MiG

- Saab AB

- Sukhoi Company

- Airbus Defence and Space

Its headquarters are located in Taufkirchen, Germany. Airbus Defence and Space, a branch of Airbus SE, is a prominent European aerospace and defence business. It was founded in 2014 and unifies intelligence services, space systems, and military aircraft. The division recorded EURO 13.4 billion in revenue in 2025, demonstrating robust growth across all of its business segments. The company provides European and international clients with cutting-edge fighter aircraft capabilities as a major participant in the Eurofighter Typhoon program. With its cutting-edge OneSat platform, which provides adaptable, software-defined solutions for international operators, Airbus Defence and Space has increased its presence in satellite technology in addition to military aircraft. The division, which employs more than 36,000 employees, is still at the forefront of cybersecurity, space, and defence research.

- BAE Systems

Its headquarters are located in Farnborough, UK. BAE Systems is a prominent multinational British defence, aerospace, and security firm. Since its founding in 1999, it has developed into one of the biggest defence contractors in the world, with over 109,000 employees worldwide. Due to robust demand in the air, maritime, land, and cyber domains, BAE reported revenues of £27.1 billion (USD 41.3 billion) in 2025. The corporation provides allied nations with cutting-edge fighter aircraft capabilities as a major partner in the F-35 and Eurofighter Typhoon programs. The acquisition of Ball Aerospace in 2024, which increased its presence in space systems and established the Space & Mission Systems division, was a significant strategic move. BAE Systems is influencing sixth-generation air combat through initiatives like the Global Combat Air Program.

- Boeing Defence

The Boeing Company's top division, Boeing Defence, Space & Security (BDS), is based in Arlington, Virginia. Founded in 1939, it now employs around 18,000 people globally and is a key component of the defence capabilities of the United States and its allies. BDS reported USD 23.9 billion in revenue in 2023; satellite deliveries and defence contracts drove additional growth in 2025. Along with the T-7A Red Hawk trainer, the division is well-known for its fighter aircraft, which include the F-15 Eagle, F/A-18 Super Hornet, and the updated F-15EX. Its space portfolio has been strengthened by recent accomplishments such as the delivery of the ViaSat-3 F2 and Satelit Nusantara Lima satellites. BDS is still pushing aerospace innovation in military aviation, satellite systems, and integrated defence solutions with a USD 76 billion backlog.

- Dassault Aviation

The French aerospace firm Dassault Aviation is well-known for its space systems, commercial jets, and military aircraft. It is based in Saint-Cloud, employs over 14,600 employees, and is crucial to French defence sovereignty. Strong Rafale and Falcon deliveries helped Dassault announce revenues of EURO 7.42 billion in 2025, despite a EURO 46.6 billion backlog. With its multirole capabilities, the Rafale continues to be its flagship aircraft, supporting both French and foreign air forces. Additionally, Dassault is a major partner in the FCAS New Generation Fighter program and the nEUROn UCAV. Recent strategic actions include increased Rafale production capacity and a €200 million investment in Harmattan AI to develop autonomous defence systems. Dassault is well-positioned for steady expansion in defence aviation thanks to possible mega-deals.

- Lockheed Martin Corporation

Its headquarters are located in Bethesda, Maryland. Lockheed Martin Corporation is a leading global player in the aerospace and defence industries. Since its founding in 1995, it has grown to be the biggest defence contractor in the world, with more than 122,000 employees. With a record backlog of USD 179 billion in 2025 and revenues of USD 71.0 billion in 2024, the business ensures long-term stability. The F-35 Lightning II, which reached record deliveries of 191 units in 2025, is Lockheed Martin's most famous fighter aircraft. In addition to cutting-edge missile and space systems, its portfolio also includes the F-22 Raptor and F-16 Fighting Falcon. The U.S. Golden Dome missile defence program is being supported, and the production capacity of PAC-3 missiles has been tripled. Lockheed Martin continues to influence the direction of international defence with unparalleled scope and creativity.

Final Wrap-up

The confrontation between Iran, Israel, and the US demonstrates how crucial fighter jets are to contemporary aerial combat. The market for fighter aircraft is expected to grow from its 2024 valuation of USD 49.13 billion to USD 77.23 billion by 2035 with a CAGR 4.20%. Both offensive and defensive operations depend heavily on air superiority, and results are shaped by stealth, electronic warfare, drone integration, and missile defence. Israel uses F-35s and improved F-16s with UAV integration, whereas the US uses F-35 Lightning II and F-15EX for strike and deterrence. Iran responds with Russian Su-35s, MiG-29s, F-4 Phantoms, and older F-14 Tomcats, backed by homegrown UAVs. Global trade routes have been disrupted, oil and gold prices have increased, and Lockheed Martin, Boeing, Airbus, Dassault, and BAE Systems' defence stocks have increased as a result of the fighting.

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?