Global Pine Derived Chemicals Market Size, Share, and COVID-19 Impact Analysis, By Type (Tall oil fatty acid, Tall oil rosin, Gum turpentine, Gum rosin, Sterols, Pitch, Others), By Source(Living trees, Dead pine stumps & logs, By-product of sulfate pulping), By Process (Kraft, Tapping), By Application (Adhesives & sealants, Paints & coatings, Surfactants, Printing inks, Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2022 – 2032

Industry: Chemicals & MaterialsGlobal Pine Derived Chemicals Market Insights Forecasts to 2032

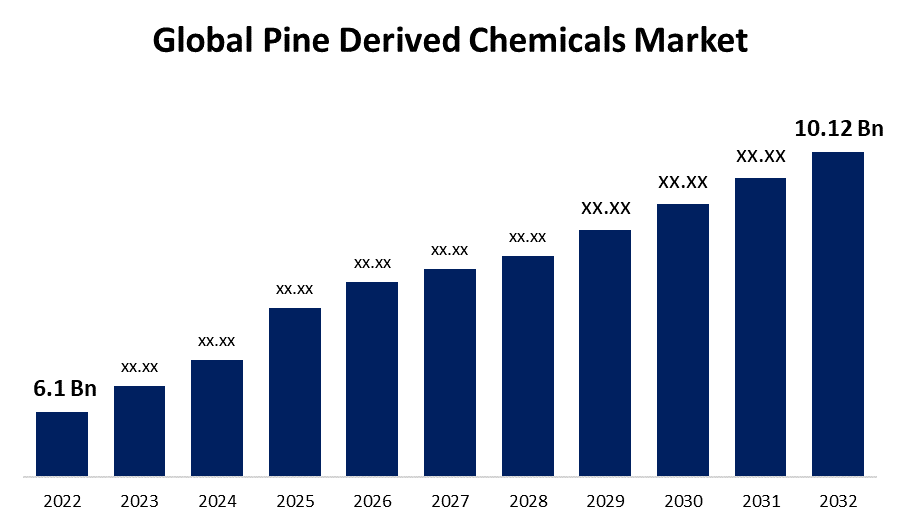

- The Global Pine Derived Chemicals Market Size was valued at USD 6.1 Billion in 2022.

- The Market Size is Growing at a CAGR of 5.19% from 2022 to 2032

- The Worldwide Pine Derived Chemicals Market Size is expected to reach USD 10.12 Billion by 2032

- Asia-Pacific is expected to Grow the fastest during the forecast period

Get more details on this report -

The Global Pine Derived Chemicals Market Size is expected to reach USD 10.12 Billion by 2032, at a CAGR of 5.19% during the forecast period 2022 to 2032.

Pine tree chemicals occur naturally and are environmentally beneficial. When compared to traditional sources, their utilization results in decreased carbon dioxide emissions. In recent years, the growing usage of crude oil and natural gas products has contributed to increased emissions and environmental challenges. As a result, there is an increasing need to limit fossil fuel consumption to reduce carbon footprints and carbon dioxide emissions. Over decades, the pine-derived chemicals industry has consistently changed and is now at the forefront of renewable bio-based industries. As a result, continuous growth in demand for these environmentally beneficial compounds generated from pine is anticipated during the projection period. Pine trees, the source of these pine-derived chemicals, are not found widely throughout the world, but are concentrated in regions of North America, Latin America, and some European and Asian nations; this limited availability is expected to impede the growth of the global chemical pine derived market over the period.

The market has seen a rise in demand for green and bio-based goods, particularly chemicals generated from pine. Consumers and companies are increasingly looking for environmentally sustainable alternatives to traditional petrochemicals. Ongoing research and development efforts have resulted in breakthroughs in extraction and processing technology for pine-derived compounds. These developments have increased production efficiency and product quality. Beyond traditional applications, pine-derived compounds are finding use in a variety of sectors.

Global Pine Derived Chemicals Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2022 |

| Market Size in 2022: | USD 6.1 Billion |

| Forecast Period: | 2022-2032 |

| Forecast Period CAGR 2022-2032 : | 5.19% |

| 2032 Value Projection: | USD 10.12 Billion |

| Historical Data for: | 2018-2021 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 100 |

| Segments covered: | By Type, By Source, By Process, By Application, By Region and COVID-19 Impact Analysis |

| Companies covered:: | Eastman Chemical Company, Renessenz, Harima Chemicals Group, Arakawa Chemical Industries, Arizona Chemical Company, DRT, Georgia-Pacific Chemicals, Mentha & Allied Products, Preverest Resources Ltd., Kraton Corporation, Ingevity Corporation, Forchem, Eastman Chemical, Wuzhou Sun Shine Forestry Ltd., and Others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenges, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

A wide range of items developed from pine trees influence practically every aspect of our lives, from perfumes, fragrances, and cosmetics to food additives, adhesives to autos, and printing inks to oil wells. Pine-derived compounds are used to make flavors for soft drinks and food, as well as soaps, household cleaners, vitamins, food additives, and other products.

The demand for substances based on pine is going to be primarily driven by rising environmental concerns. In addition, demand from the automotive industry is growing, notably in Europe. Total sales are rising as a result of the increased usage of chemicals derived from pine in the personal care industry. Innovations in biotechnology and the biofuel industry are also significant drivers. As a result of these expanded applications, demand for pine-derived compounds is increasing in the chemical industry and is expected to rise further in the coming years. Furthermore, as fossil fuel consumption rises, so do carbon dioxide emissions and carbon footprints. The growing need to reduce carbon emissions is encouraging the adoption of more environmentally friendly pine-derived chemicals, which is fueling the expansion of the pine-derived chemicals market.

Restraining Factors

Pine-derived compounds are governed by major governmental organizations like the Food and Drug Administration (FDA), the American Chemistry Council, the Environment Protection Agency (EPA), and the Pine Compounds Association. These agencies are in charge of product registration, as well as overseeing product safety, usage, and residual limits allowed in food and other applications. Deterioration of the environment is mostly to blame for the restriction of regulations and laws pertaining to compounds obtained from pine. These limitations delay the release of new items while largely affecting chemical products made from pine that are already on the market.

Market Segmentation

By Type Insights

The gum rosin segment dominates the market with the largest revenue share over the forecast period.

Based on type, the global pine-derived chemicals market is segmented into tall oil fatty acid, tall oil rosin, gum turpentine, gum rosin, sterols, pitch, and others. Among these, the gum rosin segment is dominating the market with the largest revenue share of 38.6% over the forecast period. The gum rosin segment is expected to increase at the fastest rate in terms of usefulness, owing to rising producer demand and its commercial viability. Rosin, for example, has been used as a flux in soldering. The lead-tin solder used in electronics contains approximately 1% rosin as a flux core, which aids in the smooth flow of molten metal and makes a good connection by reducing the solid oxide layer generated at the surface back to metal. Furthermore, the numerous applications of gum rosin in adhesives, paints & coatings, ink, rubber, paper, and gum-based sweets drive demand for gum rosin in the pine-derived chemicals market. Furthermore, the development of those downstream industries is expected to accelerate.

By Process Insights

The kraft segment is witnessing significant CAGR growth over the forecast period.

On the basis of process, the global pine-derived chemicals market is segmented into kraft and tapping. Among these, the kraft segment is witnessing significant CAGR growth over the forecast period. The kraft category dominated the global market because the kraft method is used by the majority of enterprises worldwide to extract pine compounds that assist in preventing environmental damage. It is the most frequent type of chemical pulping, accounting for 80% of the overall chemical pulping business. Kraft category is the digestion of wood chips in "white liquor" at high temperatures and pressures. Spent cooking liquor and pulp water are mixed to form black liquor, condensed to about 55% solids in an evaporator system.

By Source Insights

The by-product sulfate pulping segment accounted for the largest revenue share of more than 57.2% over the forecast period.

Based on the source, the global pine-derived chemicals market is classified into living trees, dead pine stumps & logs, and by-products of sulfate pulping. Among these, the by-product sulfate pulping segment is expected to hold the largest pine-derived chemicals market share during the forecast period. Pine wood pulp, which is made entirely of cellulose fiber, is made using a sulfate processing method. It is a common method to extract pine compounds and is referred to as the "kraft process" throughout. CTO and CST are the two main by-products produced by this process, and both have several uses in the end-user sector.

By Application Insights

The paints & coatings segment is expected to hold the largest share of the Global Pine Derived Chemicals Market during the forecast period.

Based on the application, the global pine-derived chemicals market is classified into adhesives & sealants, paints & coatings, surfactants, printing inks, and Others. Among these, the paints & coatings segment is expected to hold the largest pine-derived chemicals market share during the forecast period. The market for pine-derived chemicals in the paints and coatings industry is being pushed by changing lifestyles, an increase in the usage of safe and environmentally friendly items, particularly in metropolitan areas, and growing environmental concerns.

Regional Insights

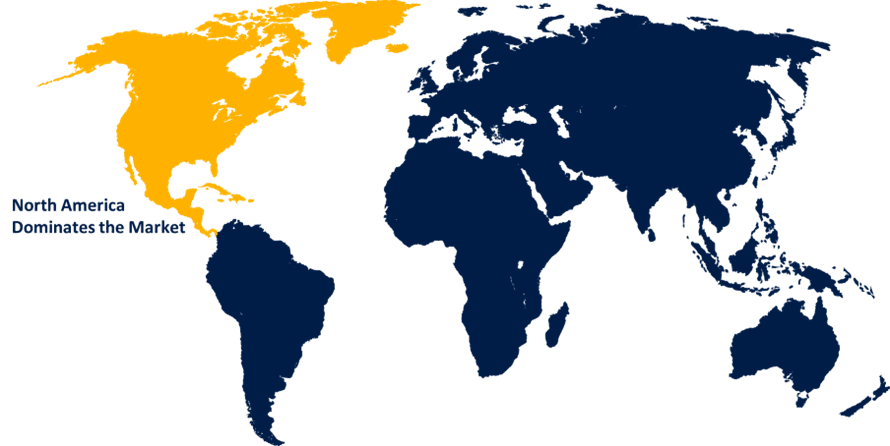

North America dominates the market with the largest market share over the forecast period.

Get more details on this report -

North America is dominating the market with more than 45.56% market share over the forecast. More than half of the market for pine-derived chemicals in North America comes from the US, and as a result, major producers have a significant presence in this region. They are in high demand due to a number of factors, including the favorable climate, the operational benefits they offer, increased environmental concerns, industrialization, ease of conducting business, and a wide range of applications.

Asia Pacific, on the contrary, is expected to grow the fastest during the forecast period. In 2021, Asia Pacific was a significant region in the global market for pine-derived compounds. The district is projected to remain strong during the forecast period. As a result of rising urbanization, higher customer disposable income, and technology improvements, the industry in this field is likely to grow rapidly over the next few years.

List of Key Market Players

- Eastman Chemical Company

- Renessenz

- Harima Chemicals Group

- Arakawa Chemical Industries

- Arizona Chemical Company

- DRT

- Georgia-Pacific Chemicals

- Mentha & Allied Products

- Preverest Resources Ltd.

- Kraton Corporation

- Ingevity Corporation

- Forchem

- Eastman Chemical

- Wuzhou Sun Shine Forestry Ltd.

Key Market Developments

- On April 2023, the Corporation formed a joint venture with Chemiplas, Australia, to become DCL Corporation's only distributor in Australia and New Zealand.

- In March 2022, Kraton Corp., a major global sustainable manufacturer of specialty polymers and high-value bio-based products derived from byproducts of pine wood pulping, announced a formal merger agreement with DL Chemical.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2032. Spherical Insights has segmented the global pine-derived chemicals market based on the below-mentioned segments:

Pine Derived Chemicals Market, Type Analysis

- Tall oil fatty acid

- Tall oil rosin

- Gum turpentine

- Gum rosin

- Sterols

- Pitch

Pine Derived Chemicals Market, Process Analysis

- Kraft

- Tapping

Pine Derived Chemicals Market, Source Analysis

- Living trees

- Dead pine stumps & logs

- By-product of sulfate pulping

Pine Derived Chemicals Market, Application Analysis

- Adhesives & sealants

- Paints & coatings

- Surfactants

- Printing inks

Pine Derived Chemicals Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Need help to buy this report?