Global Non-Hodgkin Lymphoma Therapeutics Market Size, Share, and COVID-19 Impact Analysis, By Type (Chemotherapy and Targeted Therapy), By Cell type (B Cell Lymphomas and T Cell Lymphoma), By Distribution Channel (Retail Pharmacies & Drug Stores, Hospital Pharmacies, and Online Pharmacies), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2022 - 2032

Industry: HealthcareGlobal Non-Hodgkin Lymphoma Therapeutics Market Size Insights Forecasts to 2032

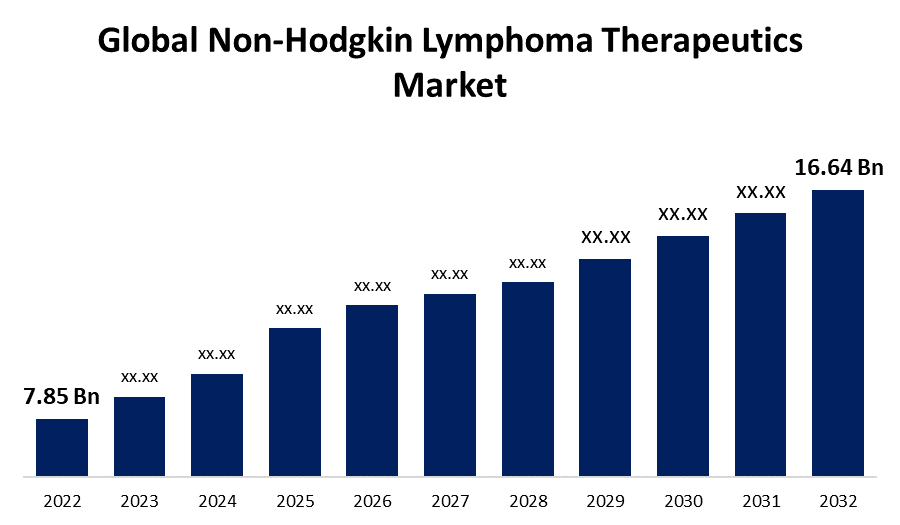

- The Global Non-Hodgkin Lymphoma Therapeutics Market Size was valued at USD 7.85 Billion in 2022.

- The Market Size is Growing at a CAGR of 7.8% from 2022 to 2032

- The Worldwide Non-Hodgkin Lymphoma Therapeutics Market Size is expected to reach USD 16.64 Billion by 2032

- Asia-Pacific is expected to Grow higher during the forecast period

Get more details on this report -

The Global Non-Hodgkin Lymphoma Therapeutics Market Size is expected to reach USD 16.64 Billion by 2032, at a CAGR of 7.8% during the forecast period 2022 to 2032.

Market Overview

Non-Hodgkin lymphoma (NHL) therapeutics encompass a diverse array of treatments designed to combat malignant lymphocyte proliferation in various subtypes of this hematologic malignancy. Standard therapeutic modalities include chemotherapy, targeted therapies, immunotherapy, and radiation. Chemotherapy regimens, such as CHOP (cyclophosphamide, doxorubicin, vincristine, prednisone), have been cornerstones of treatment, while targeted therapies like rituximab (anti-CD20 monoclonal antibody) have transformed care by selectively attacking lymphoma cells. Immunotherapies like CAR T-cell therapy reprogram patients' immune cells to target lymphoma cells more effectively. Novel agents targeting specific signaling pathways and genetic mutations are continually emerging. The landscape of NHL therapeutics is rapidly evolving, leading to personalized and more effective treatment approaches, improved outcomes, and enhanced quality of life for patients.

Report Coverage

This research report categorizes the market for non-hodgkin lymphoma therapeutics market based on various segments and regions and forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the non-hodgkin lymphoma therapeutics market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segments of the non-hodgkin lymphoma therapeutics market.

Global Non-Hodgkin Lymphoma Therapeutics Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2022 |

| Market Size in 2022: | USD 7.85 Billion |

| Forecast Period: | 2022-2032 |

| Forecast Period CAGR 2022-2032 : | 7.8% |

| 2032 Value Projection: | USD 16.64 Billion |

| Historical Data for: | 2018-2021 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Type, By Cell type, By Distribution Channel, By Region and COVID-19 Impact Analysis. |

| Companies covered:: | Bayer AG, Eisai Pharmaceuticals Inc., Cephalon Inc., Accredo Health Group Inc., GlaxoSmithKline PLC, Celgene Corp., F. Hoffman La Roche Ltd., Bristol Myers Squibb Co., Eli Lilly and Co., Baxter International Inc., and other key vendors. |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The non-hodgkin lymphoma (NHL) therapeutics market is influenced by a confluence of factors that collectively shape its dynamics, the increasing global incidence of NHL, attributed to factors like aging populations and environmental exposures, drives market growth as it necessitates enhanced therapeutic options. Moreover, technological advancements in diagnostic techniques enable earlier and accurate NHL detection, fostering demand for corresponding treatments. The growing understanding of NHL's diverse molecular subtypes and genetic abnormalities has spurred the development of targeted therapies, attracting substantial investment and propelling market expansion. Furthermore, the evolving landscape of immunotherapy, exemplified by immune checkpoint inhibitors and CAR T-cell therapies, has revolutionized NHL treatment paradigms. These innovative approaches harness the immune system to combat lymphoma cells, offering promising outcomes for refractory cases and fueling market progression. Additionally, collaborations between pharmaceutical companies and research institutions facilitate the discovery of novel therapeutic agents, fostering competition and innovation within the market.

Patient preferences for personalized treatment strategies have amplified the demand for precision medicine in NHL therapeutics. This demand has prompted pharmaceutical companies to invest in developing drugs tailored to specific genetic mutations or signaling pathways, resulting in a more tailored and effective approach to treatment. Moreover, the emphasis on improving patient quality of life has led to the development of less toxic and more targeted therapies, further augmenting market growth. The influence of healthcare policies and regulatory frameworks cannot be overlooked. Stringent regulatory requirements for drug approvals and reimbursements shape market access and pricing dynamics. Additionally, the market is affected by economic factors such as healthcare expenditure and insurance coverage, which impact patient access to novel and expensive treatments.

Restraining Factors

The non-hodgkin lymphoma therapeutics market faces several significant restraints that impact its growth trajectory. These include the high cost of innovative treatments such as targeted therapies and CAR T-cell therapies, which can limit patient access due to financial constraints and reimbursement challenges. Additionally, the complex and diverse nature of NHL subtypes poses challenges in developing universally effective therapies, hindering streamlined treatment approaches. Moreover, potential side effects and toxicities associated with certain treatments may deter both patients and physicians from pursuing aggressive therapeutic options, impacting overall market adoption.

Market Segmentation

- Chemotherapy segment expected to grow at the fastest CAGR of around 8.2% during the forecast period

On the basis of the type, the global non-hodgkin lymphoma therapeutics market is segmented into chemotherapy and targeted therapy. The chemotherapy segment is anticipated to exhibit rapid growth during the forecast period in the non-hodgkin lymphoma therapeutics market. Despite the emergence of novel therapies, chemotherapy remains a cornerstone due to its broad applicability across various NHL subtypes. Its well-established protocols and familiarity among healthcare professionals contribute to its sustained demand. Additionally, in resource-constrained regions, chemotherapy often serves as a cost-effective treatment option. Furthermore, combination regimens and advancements in supportive care have improved chemotherapy's efficacy and reduced associated side effects, augmenting its attractiveness as a treatment choice and resulting in the projected robust growth of this segment.

- The B cell lymphomas segment held the largest market with more than 60.4% revenue share in 2022

Based on the cell type, the global non-hodgkin lymphoma therapeutics market is segmented into B cell lymphomas and T cell lymphoma. The B cell lymphomas segment's prominence in the non-hodgkin lymphoma (NHL) therapeutics market can be attributed to its higher prevalence and diversity among NHL subtypes. B cell lymphomas encompass a wide range of diseases, including diffuse large B cell lymphoma, follicular lymphoma, and mantle cell lymphoma, collectively constituting a significant portion of NHL cases. This prevalence has driven extensive research and development efforts, resulting in targeted therapies like anti-CD20 monoclonal antibodies (such as rituximab) that specifically address B cell-related malignancies. The availability of effective treatments, coupled with the therapeutic advances tailored to B cell lymphomas, has solidified their position as the largest market segment in NHL therapeutics.

- The hospital pharmacies segment held the largest market with more than 37.5% revenue share in 2022

Based on the distribution channel, the global non-hodgkin lymphoma therapeutics market is segmented into retail pharmacies & drug stores, hospital pharmacies, and online pharmacies. The hospital pharmacies segment's dominance in the non-hodgkin lymphoma therapeutics market can be attributed to several factors. Hospitals serve as major treatment centers for cancer patients, providing comprehensive care, including diagnosis, treatment, and monitoring. This concentrated approach facilitates the effective distribution and administration of various therapies. Moreover, hospitals have the necessary infrastructure to store and handle specialized treatments like chemotherapy and targeted therapies. Collaborations between pharmaceutical companies and hospital networks also enhance accessibility to these therapies. The hospital pharmacies' extensive reach, expertise, and patient-centric care contribute to their holding the largest market share in the distribution of non-hodgkin lymphoma therapeutics.

Regional Segment Analysis of the Non-Hodgkin Lymphoma Therapeutics Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

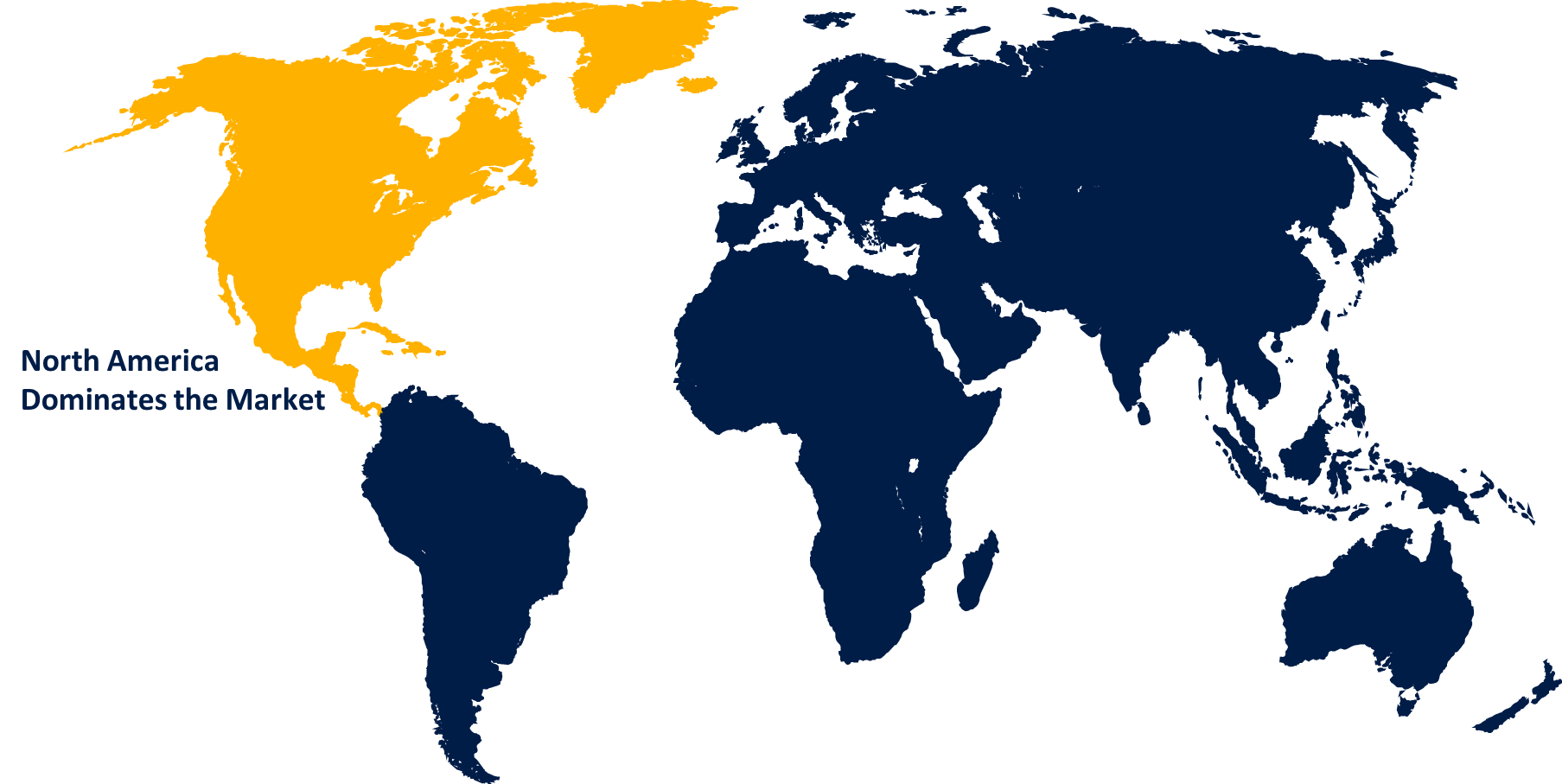

North America dominated the market with more than 35.4% revenue share in 2022.

Get more details on this report -

Based on region, North America's dominance in the non-hodgkin lymphoma therapeutics market can be attributed to its advanced healthcare infrastructure, robust research and development activities, and high adoption of innovative medical technologies. The region benefits from substantial investment in cancer research, a well-established pharmaceutical industry, and a favorable regulatory environment that accelerates drug approvals. Moreover, strong healthcare expenditure, increasing awareness about lymphoma, and access to novel therapies contribute to North America's prominent market share in non-hodgkin lymphoma therapeutics.

Asia-Pacific region is projected for significant growth in the non-hodgkin lymphoma therapeutics market during the forecast period due to increasing incidence of non-hodgkin lymphoma, improving healthcare infrastructure, rising awareness, and growing investments in medical research are driving the demand for effective therapies. Additionally, the region's large and aging population, coupled with changing lifestyles, contributes to the rising disease burden. Increasing accessibility to advanced treatments, along with collaborations between global pharmaceutical companies and local healthcare providers, further supports the projected higher growth rate of the non-hodgkin lymphoma therapeutics market in Asia-Pacific.

Recent Developments

- In January 2022, The Food and Drug Administration (FDA) granted Cellular Biomedicine Group Inc. approval for C-CAR039, a novel autologous bi-specific CAR-T therapy targeting both CD19 and CD20 antigens, with Regenerative Medicine Advanced Therapy (RMAT) Designation and Fast Track Designation for the treatment of patients with relapsed or refractory diffuse large B cell lymphoma (r/r DLBCL).

- In March 2023, AstraZeneca's Calquence has been licenced by China's National Medical Products Administration (NMPA) for the treatment of adult patients with mantle cell lymphoma (MCL).

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global non-hodgkin lymphoma therapeutics market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Companies:

- Bayer AG

- Eisai Pharmaceuticals Inc.

- Cephalon Inc.

- Accredo Health Group Inc.

- GlaxoSmithKline PLC

- Celgene Corp.

- F. Hoffman La Roche Ltd.

- Bristol Myers Squibb Co.

- Eli Lilly and Co.

- Baxter International Inc.

Key Target Audience

- Market Players

- Investors

- End-Users

- Government Authorities

- Consulting and Research Firm

- Venture Capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. Spherical Insights has segmented the global non-hodgkin lymphoma therapeutics market based on the below-mentioned segments:

Non-Hodgkin Lymphoma Therapeutics Market, By Type

- Chemotherapy

- Targeted Therapy

Non-Hodgkin Lymphoma Therapeutics Market, By Cell Type

- B Cell Lymphomas

- T Cell Lymphoma

Non-Hodgkin Lymphoma Therapeutics Market, By Distribution Channel

- Retail Pharmacies & Drug Stores

- Hospital Pharmacies

- Online Pharmacies

Non-Hodgkin Lymphoma Therapeutics Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Need help to buy this report?