Global Medical Polymers Market Size, Share, and COVID-19 Impact Analysis, By Product (Fibers & Resins, Medical Elastomers, Biodegradable Polymer, and Others), By Application (Medical Device Packaging, Medical Components, Orthopedic Soft Goods, Wound Care, Cleanroom Supplies, BioPharm Devices, Mobility Aids, Sterilization & Infection Prevention, Tooth Implants, Denture-based Materials, Others), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2032

Industry: Chemicals & MaterialsGlobal Medical Polymers Market Insights Forecasts to 2032

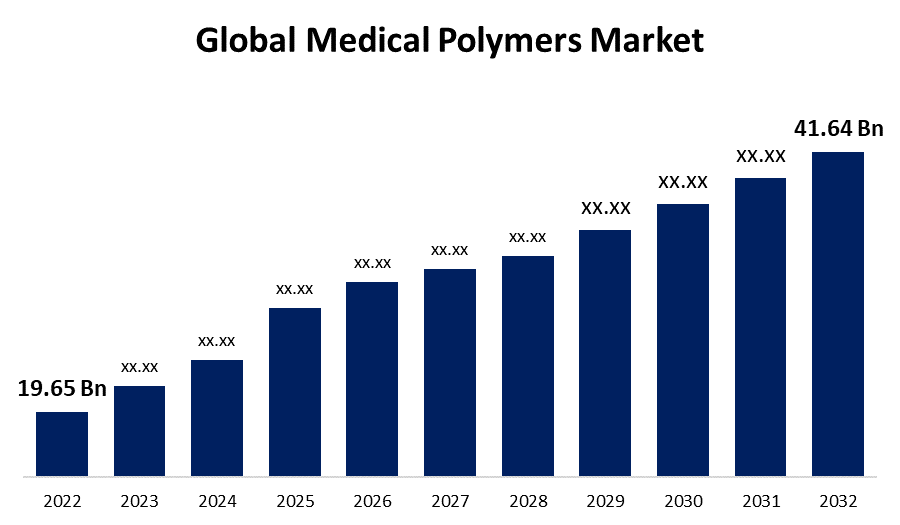

- The Medical Polymers Market was valued at USD 19.65 Billion in 2022.

- The Market is growing at a CAGR of 7.8% from 2023 to 2032

- The Worldwide Medical Polymers Market is expected to reach USD 41.64 Billion by 2032

- MEA is expected to grow the highest during the forecast period

Get more details on this report -

The Global Medical Polymers Market is expected to reach USD 41.64 Billion by 2032, at a CAGR of 7.8% during the forecast period 2022 to 2032.

Market Overview

Medical polymers are essential materials used in various healthcare applications due to their unique properties and biocompatibility. These polymers play a vital role in medical devices, drug delivery systems, tissue engineering, and surgical procedures. They are designed to meet stringent requirements such as sterilization compatibility, chemical resistance, mechanical strength, and biodegradability. Common medical polymers include polyethylene, polypropylene, polyurethane, polyvinyl chloride, and silicone rubber. These materials offer advantages such as flexibility, low friction, non-toxicity, and ease of fabrication. Medical polymers are used in a wide range of applications, including implants, catheters, surgical sutures, wound dressings, and drug capsules. With ongoing advancements in polymer science, medical polymers continue to contribute significantly to the improvement of healthcare outcomes and patient well-being.

Report Coverage

This research report categorizes the market for medical polymers market based on various segments and regions and forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the medical polymers market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segments of the Medical polymers market.

Global Medical Polymers Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2022 |

| Market Size in 2022: | USD 19.65 Billion |

| Forecast Period: | 2022-2032 |

| Forecast Period CAGR 2022-2032 : | 7.8% |

| 2032 Value Projection: | USD 41.64 Billion |

| Historical Data for: | 2018-2021 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 100 |

| Segments covered: | By Product, By Product, By Region and COVID-19 Impact Analysis |

| Companies covered:: | BASF SE, NatureWorks LLC, Covestro AG, Celanese Corporation, Eastman Chemical Corporation, Evonik Industries AG, Dow Inc., Exxon Mobil Corporation, Arkema, Koninklijke DSM NV, Formosa Plastics Corporation, Foryou Medical, Kraton Corporation, SABIC, Trinseo S.A., and others. |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The medical polymers market is driven by several key factors due to rising demand for advanced healthcare solutions and the increasing prevalence of chronic diseases drive the need for medical devices and implants, thus fueling the demand for medical polymers. Additionally, the growing geriatric population, coupled with an increase in surgical procedures, contributes to the market growth. Moreover, technological advancements in polymer science and engineering have led to the development of innovative medical polymers with enhanced properties and performance, further boosting market demand. Furthermore, the shift towards minimally invasive surgeries and the rising focus on personalized medicine are driving the adoption of medical polymers in drug delivery systems and regenerative medicine. Stringent regulations and standards for medical devices and materials also play a significant role in shaping the market, ensuring the safety and efficacy of medical polymers.

Restraining Factors

The medical polymers market also faces certain restraints. One significant restraint is the high cost associated with the development and production of medical-grade polymers, making them less accessible in some regions. Additionally, the stringent regulatory requirements for medical polymers pose challenges for manufacturers in terms of compliance and approval processes. Moreover, concerns regarding the environmental impact of non-biodegradable polymers and the need for sustainable alternatives create a restraint on the market. Furthermore, the risk of adverse reactions or complications associated with the use of certain polymers in medical applications can impact market growth. The limited availability of skilled professionals and the need for specialized manufacturing capabilities also pose challenges to the market's expansion.

Market Segmentation

- In 2022, the fibers & resins segment accounted for around 36.4% market share

On the basis of the product type, the global medical polymers market is segmented into fibers & resins, medical elastomers, biodegradable polymer, and others. The fibers & resins segment has emerged as the dominant sector in the medical polymers market. This dominance can be attributed to several factors such as fibers and resins offer excellent mechanical strength, chemical resistance, and biocompatibility, making them ideal for a wide range of medical applications. They are widely used in the manufacturing of medical devices, implants, and surgical instruments, where their properties are essential for ensuring durability and performance. The advancements in fiber and resin technology have led to the development of innovative materials with enhanced properties such as antimicrobial activity and biodegradability. Moreover, the increasing demand for biocompatible and bioresorbable materials in tissue engineering and regenerative medicine further drives the growth of the fibers & resins segment. Additionally, the versatility and cost-effectiveness of fibers and resins make them a preferred choice for various healthcare applications, solidifying their dominance in the medical polymers market.

- In 2022, the medical device packaging segment dominated with more than 27.2% market share

Based on the type of application, the global medical polymers market is segmented into medical device packaging, medical components, orthopedic soft goods, wound care, cleanroom supplies, biopharm devices, mobility aids, sterilization & infection prevention, tooth implants, denture-based materials, others. The medical device packaging segment has emerged as the dominant sector in the medical polymers market. This dominance can be attributed to several factors because the packaging of medical devices is of utmost importance to ensure their sterility, protection, and safe handling during transportation and storage. Medical device packaging polymers offer characteristics such as high barrier properties, chemical resistance, and compatibility with sterilization processes, ensuring the integrity and safety of the packaged devices. The increasing demand for medical devices globally, coupled with stringent regulations and standards for device packaging, drives the growth of this segment. Additionally, the growing awareness of infection control and the need for tamper-evident packaging in the healthcare industry further contribute to the dominance of the medical device packaging segment. Moreover, the rising preference for innovative packaging solutions, such as blister packs and pouches, also fuels the market growth in this segment. Overall, the critical role played by medical device packaging in ensuring patient safety and product efficacy solidifies its dominant position in the medical polymers market.

Regional Segment Analysis of the Medical Polymers Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America dominated the market with more than 40.2% revenue share in 2022.

Get more details on this report -

Based on region, North America has emerged as the dominant market for medical polymers, holding the largest market share. Several factors contribute to this leadership position because the region has a well-established healthcare infrastructure and a high level of technological advancements, which drive the demand for medical polymers. North America boasts a large consumer base for medical devices and implants, fueled by a growing aging population and an increasing prevalence of chronic diseases. Moreover, the presence of major pharmaceutical and medical device companies in the region stimulates the development and adoption of medical polymers. Additionally, favorable government regulations and policies that support research and development activities in the healthcare sector further propel market growth. The region's robust economy, high healthcare expenditure, and a strong emphasis on quality healthcare also contribute to North America's significant market share in the medical polymers industry.

Recent Development

- In October 2022, Celanese Corporation has unveiled its plans to enhance its capabilities in response to the growing global need for pharmaceutical-grade polymers used in manufacturing implants and inserts for controlled-release medication. The company will establish a state-of-the-art cleanroom facility spanning 1,000 square feet in Edmonton, Alberta. This specialized facility will focus on cryogenic micronization of VitalDose EVA material, transforming it into powder form for effective blending with small molecules and biologics, catering to diverse pharmaceutical requirements.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global medical polymers market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Companies:

- BASF SE

- NatureWorks LLC

- Covestro AG

- Celanese Corporation

- Eastman Chemical Corporation

- Evonik Industries AG

- Dow Inc.

- Exxon Mobil Corporation

- Arkema

- Koninklijke DSM NV

- Formosa Plastics Corporation

- Foryou Medical

- Kraton Corporation

- SABIC

- Trinseo S.A.

Key Target Audience

- Market Players

- Investors

- End-Users

- Government Authorities

- Consulting and Research Firm

- Venture Capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. Spherical Insights has segmented the global medical polymers market based on the below-mentioned segments:

Medical Polymers Market, By Product

- Fibers & Resins

- Medical Elastomers

- Biodegradable Polymer

- Others

Medical Polymers Market, By Application

- Medical Device Packaging

- Medical Components

- Orthopedic Soft Goods

- Wound Care

- Cleanroom Supplies

- BioPharm Devices

- Mobility Aids

- Sterilization & Infection Prevention

- Tooth Implants

- Denture-based Materials

- Others

Medical Polymers Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Need help to buy this report?