Global Distributed Energy Generation Market Size, Share, and COVID-19 Impact Analysis, By Technology (Wind Turbine, Solar Photovoltaic, Reciprocating Engines, Fuel Cells, and Gas & Steam Turbine), By End-Use Industry (Residential, Commercial, and Industrial), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 – 2032

Industry: Energy & PowerGlobal Distributed Energy Generation Market Insights Forecasts to 2032

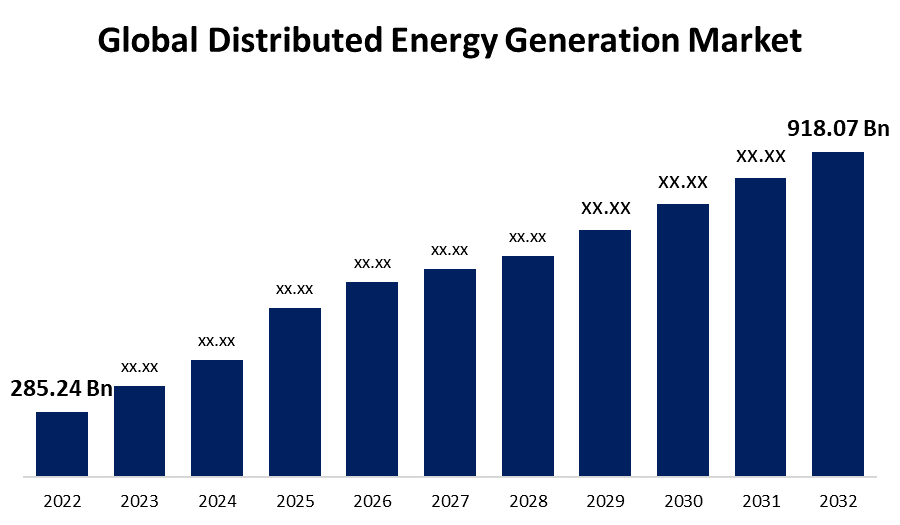

- The Distributed Energy Generation Market was valued at USD 285.24 Billion in 2022.

- The Market is growing at a CAGR of 12.4% from 2023 to 2032

- The Worldwide Distributed Energy Generation Market is expected to reach USD 918.07 Billion by 2032

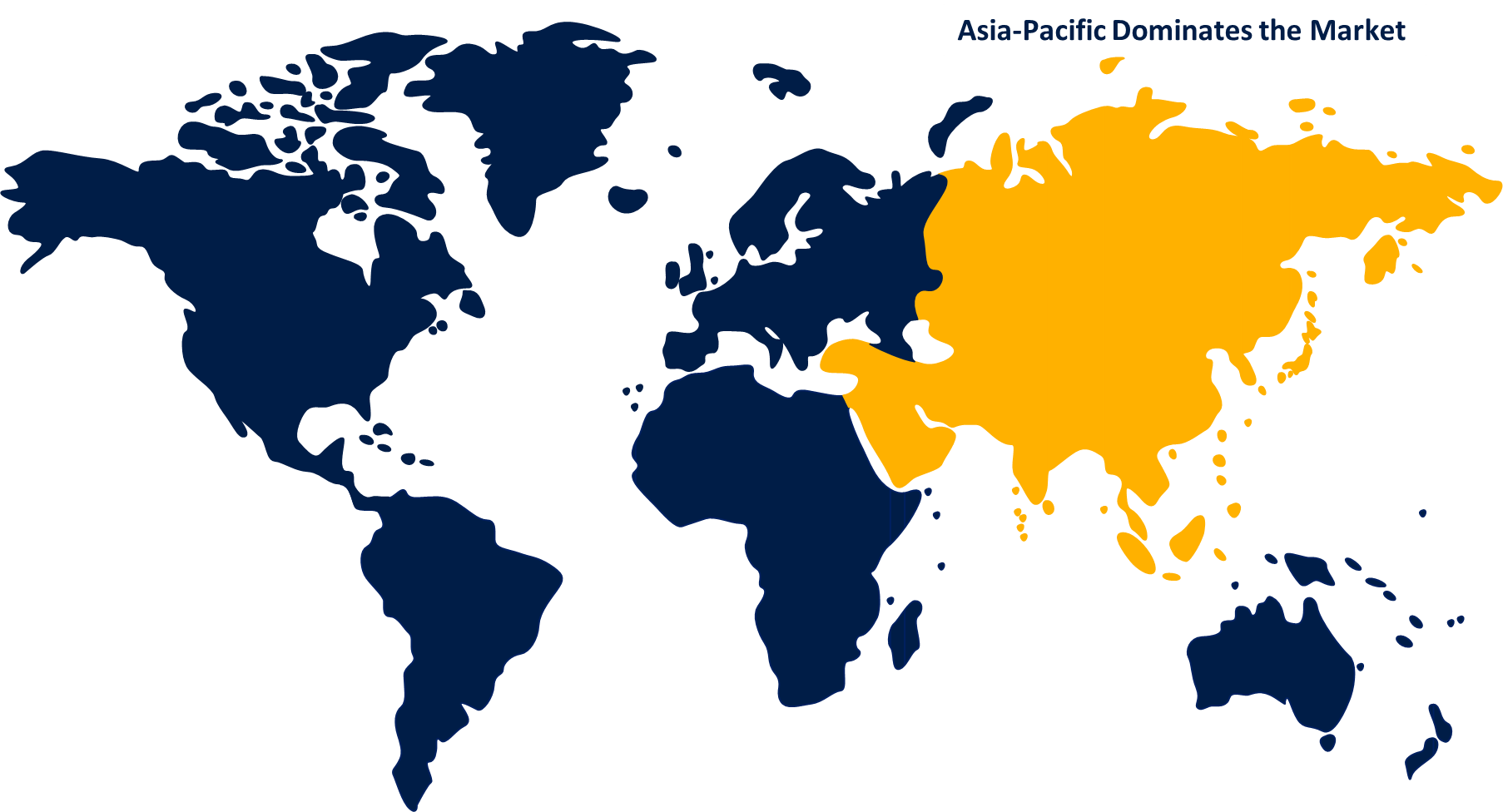

- MEA is expected to have significant growth during the forecast period

Get more details on this report -

The Global Distributed Energy Generation Market is expected to reach USD 918.07 Billion by 2032, at a CAGR of 12.4% during the forecast period 2022 to 2032.

Market Overview

Distributed energy generation (DEG) refers to the decentralized production of electricity from various small-scale energy sources located close to end-users. It is an emerging trend in the energy sector, driven by the need for a more sustainable and resilient power system. DEG encompasses a diverse range of technologies, including solar photovoltaics (PV), wind turbines, biomass, micro-hydro, and fuel cells. By generating electricity closer to the point of consumption, DEG reduces transmission losses and enhances grid reliability. It also promotes renewable energy adoption, mitigates greenhouse gas emissions, and facilitates energy independence. DEG systems can be integrated into existing infrastructure or operate independently, providing opportunities for communities, businesses, and individuals to participate in the clean energy transition and contribute to a more resilient and decentralized energy landscape.

Report Coverage

This research report categorizes the market for distributed energy generation market based on various segments and regions and forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the distributed energy generation market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segments of the distributed energy generation market.

Global Distributed Energy Generation Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2022 |

| Market Size in 2022: | USD 285.24 Billion |

| Forecast Period: | 2022-2032 |

| Forecast Period CAGR 2022-2032 : | 12.4% |

| 2032 Value Projection: | USD 918.07 Billion |

| Historical Data for: | 2018-2021 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 100 |

| Segments covered: | By Technology, By End-Use Industry, By Region and COVID-19 Impact Analysis |

| Companies covered:: | Vestas Wind Systems A/S, Capstone Turbine Corp., Caterpillar, Ballard Power Systems Inc., Doosan Heavy Industries & Construction, Rolls-Royce PLC., Suzlon Energy Ltd., General Electric, Siemens, Schneider Electric, ENERCON GmbH, Sharp Corp., First Solar, Mitsubishi Electric Corp., Toyota Turbine and Systems Inc., and others |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The distributed energy generation (DEG) market is driven by several key factors, due to increasing demand for clean and renewable energy sources is a major driver. DEG allows for the utilization of diverse energy resources such as solar, wind, and biomass, reducing reliance on fossil fuels and mitigating environmental impacts. The advancements in technology, particularly in solar PV and energy storage systems, have made DEG more cost-effective and accessible. Additionally, the need for energy security and grid resilience is pushing the adoption of DEG. By generating electricity closer to the point of consumption, DEG reduces transmission losses and enhances the reliability of the power system. Furthermore, supportive government policies, such as incentives, subsidies, and regulations promoting renewable energy, play a crucial role in driving the DEG market forward. Overall, these drivers are propelling the growth of DEG as a sustainable and decentralized energy solution.

Restraining Factors

While the distributed energy generation (DEG) market has numerous drivers, it also faces several restraints. One significant challenge is the high upfront costs associated with deploying DEG systems. The initial investment required for the installation and integration of renewable energy technologies can be a barrier, particularly for smaller businesses or individuals. Additionally, grid integration and regulatory barriers pose challenges. The existing grid infrastructure may not be designed to accommodate distributed generation, requiring significant upgrades and investments. Moreover, policy and regulatory frameworks may lack clarity or consistency, creating uncertainties for investors and developers. Finally, intermittency and variability of renewable energy sources can impact the stability and reliability of the power supply, necessitating efficient energy storage and grid management solutions.

Market Segmentation

- In 2022, the fuel cells segment accounted for around 35.4% market share

On the basis of the technology, the global distributed energy generation market is segmented into wind turbine, solar photovoltaic, reciprocating engines, fuel cells, and gas & steam turbine. the fuel cells segment has emerged as the leader, holding the largest market share. Several factors contribute to its dominant position such as fuel cells offer a clean and efficient alternative to traditional combustion-based power generation technologies. They produce electricity through electrochemical reactions, resulting in lower emissions and higher energy conversion efficiencies. The fuel cells have a wide range of applications across industries, including transportation, residential, commercial, and industrial sectors. They can power vehicles, provide backup or off-grid power, and even act as combined heat and power (CHP) systems. Additionally, advancements in fuel cell technology, such as the development of proton exchange membrane fuel cells (PEMFC) and solid oxide fuel cells (SOFC), have enhanced their performance, reliability, and cost-effectiveness. Furthermore, government support through incentives, subsidies, and research funding has spurred the growth of the fuel cells market. These factors have propelled the fuel cells segment to the forefront, driving its large market share.

- In 2022, the commercial segment dominated with more than 56.2% market share

Based on the end-use industry, the global distributed energy generation market is segmented into residential, commercial, and industrial. The commercial segment has emerged as the leader, holding the largest market share in the energy industry. The commercial establishments, including office buildings, shopping malls, hotels, and industrial complexes, have significant energy consumption requirements. This creates a vast market for energy solutions and technologies tailored specifically for commercial applications. Commercial entities are increasingly recognizing the benefits of adopting sustainable and energy-efficient practices. They are motivated by factors such as cost savings, corporate social responsibility, and regulatory compliance. Moreover, governments and organizations worldwide are implementing energy efficiency and sustainability targets, driving the demand for energy-efficient solutions in the commercial sector. Additionally, technological advancements in energy management systems, building automation, and renewable energy technologies have made it easier for commercial establishments to optimize energy consumption and integrate clean energy sources. These factors collectively contribute to the commercial segment's dominant market share in the energy industry.

Regional Segment Analysis of the Distributed Energy Generation Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia-Pacific dominated the market with more than 46.2% revenue share in 2022.

Get more details on this report -

Based on region, the Asia-Pacific region has emerged as a leader in the renewable energy market, holding the largest market share. Several factors contribute to its dominant position such as significant population and rapidly growing economies, leading to an increasing demand for energy. Governments in countries like China, India, and Japan have implemented ambitious renewable energy targets and policies to address energy security, climate change, and air pollution concerns. Additionally, the region boasts abundant renewable energy resources, including solar, wind, hydro, and geothermal, which provide ample opportunities for development. Moreover, the declining costs of renewable technologies, advancements in energy storage, and supportive financing mechanisms have further accelerated the adoption of renewables in the region. These factors have propelled the Asia-Pacific region to the forefront of the global renewable energy market.

Recent Development

- In June 2022, Enrique Razon, a Philippine billionaire, has revealed plans for the construction of the world's largest solar power facility. The infrastructure investment division of Razon's company intends to collaborate with various local firms that are actively involved in the development of renewable energy.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global distributed energy generation market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Companies:

- Vestas Wind Systems A/S

- Capstone Turbine Corp.

- Caterpillar

- Ballard Power Systems Inc.

- Doosan Heavy Industries & Construction

- Rolls-Royce PLC.

- Suzlon Energy Ltd.

- General Electric

- Siemens

- Schneider Electric

- ENERCON GmbH

- Sharp Corp.

- First Solar

- Mitsubishi Electric Corp.

- Toyota Turbine and Systems Inc.

Key Target Audience

- Market Players

- Investors

- End-Users

- Government Authorities

- Consulting and Research Firm

- Venture Capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2022 to 2032. Spherical Insights has segmented the global distributed energy generation market based on the below-mentioned segments:

Distributed Energy Generation Market, By Technology

- Wind Turbine

- Solar Photovoltaic

- Reciprocating Engines

- Fuel Cells

- Gas & Steam Turbine

Distributed Energy Generation Market, By End-Use Industry

- Residential

- Commercial

- Industrial

Distributed Energy Generation Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Need help to buy this report?