Global Digital Pathology Market Size, Share, and COVID-19 Impact Analysis, By Product (Software, Device, and Storage System), By Application (Drug Discovery & Development, Academic Research, and Disease Diagnosis), By End-Use (Hospitals, Biotech & Pharma Companies, Diagnostic Labs, and Academic & Research Institutes), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2022 - 2032.

Industry: HealthcareGlobal Digital Pathology Market Insights Forecasts to 2032

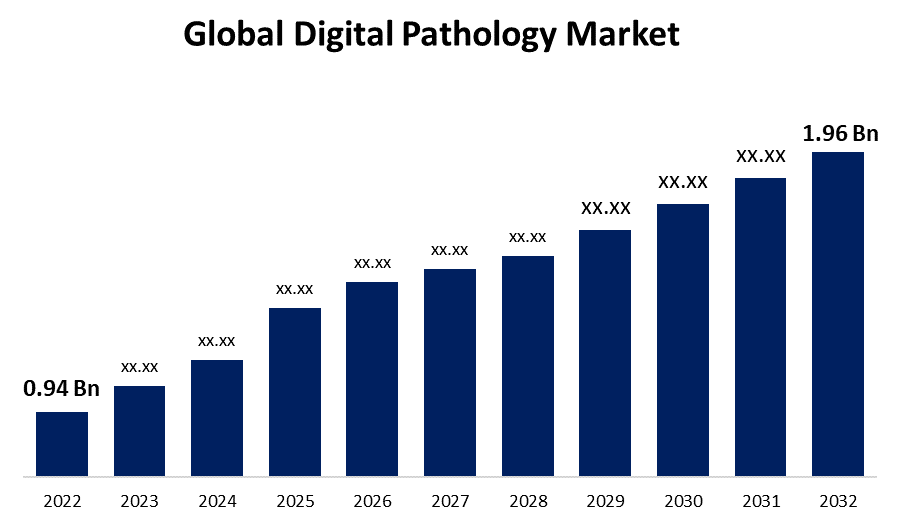

- The Global Digital Pathology Market Size was valued at USD 0.94 Billion in 2022.

- The Market Size is Growing at a CAGR of 7.6% from 2022 to 2032

- The Worldwide Digital Pathology Market Size is expected to reach USD 1.96 Billion by 2032

- Asia-Pacific is expected To Grow fastest during the forecast period

Get more details on this report -

The Global Digital Pathology Market Size is expected to reach USD 1.96 Billion by 2032, at a CAGR of 7.6% during the forecast period 2022 to 2032.

Market Overview

Digital pathology is a rapidly evolving field that merges pathology with digital imaging technology. It involves the acquisition, management, and interpretation of high-resolution images of tissue samples for diagnostic purposes. Traditional pathology relies on glass slides and microscopes for examination, but digital pathology replaces these with digital slides that can be viewed and analyzed on computer screens. This transformative technology enables pathologists to access and share digitized images remotely, fostering collaboration and enhancing efficiency in diagnosis, research, and education. It also enables the integration of advanced image analysis techniques, such as machine learning and artificial intelligence, for automated detection and quantification of pathological features. Digital pathology offers numerous advantages, including improved workflow, streamlined consultations, standardized reporting, and enhanced archival capabilities. As it continues to advance, digital pathology has the potential to revolutionize pathology practice and contribute to more accurate and personalized patient care.

Report Coverage

This research report categorizes the market for digital pathology market based on various segments and regions and forecasts revenue growth and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the digital pathology market. Recent market developments and competitive strategies such as expansion, product launch, and development, partnership, merger, and acquisition have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segments of the digital pathology market.

Global Digital Pathology Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2022 |

| Market Size in 2022: | USD 0.94 Billion |

| Forecast Period: | 2022-2032 |

| Forecast Period CAGR 2022-2032 : | 7.6% |

| 2032 Value Projection: | USD 1.96 Billion |

| Historical Data for: | 2018-2021 |

| No. of Pages: | 200 |

| Tables, Charts & Figures: | 110 |

| Segments covered: | By Product, By Application, By End-Use, By Region |

| Companies covered:: | Leica Biosystems Nussloch GmbH, Hamamatsu Photonics, Inc., Koninklijke Philips N.V., Olympus Corporation, F. Hoffmann-La Roche Ltd., Mikroscan Technologies, Inc., Inspirata, Inc., Epredia, Visiopharm A/S, Huron Technologies International Inc., and ContextVision AB |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

The digital pathology market is driven by several factors that are shaping its growth and adoption, the increasing demand for efficient and accurate diagnostic techniques is a major driver. Digital pathology enables pathologists to access and analyze digital slides remotely, improving workflow and reducing turnaround time. The integration of artificial intelligence (AI) and machine learning algorithms in digital pathology has opened new avenues for automated analysis and interpretation of pathology images, enhancing diagnostic accuracy. The growing need for centralized data storage, archiving, and sharing of pathology images among healthcare professionals for collaborative decision-making is driving the market. Additionally, the expanding applications of digital pathology in research, drug discovery, and personalized medicine are fueling its adoption. Overall, the advancements in digital imaging technology and the increasing availability of cost-effective digital pathology solutions are further propelling market growth.

Restraining Factors

While the digital pathology market presents numerous opportunities, it also faces certain restraints. One significant restraint is the high initial setup and implementation costs associated with digital pathology systems, including scanners, storage infrastructure, and software. This can pose a financial burden for healthcare facilities, particularly smaller clinics and laboratories. Another restraint is the need for extensive training and expertise to effectively utilize and interpret digital pathology images, which may require additional investments in education and skill development. Furthermore, concerns related to data security, privacy, and regulatory compliance can hinder the widespread adoption of digital pathology. Additionally, the resistance to change among pathologists accustomed to traditional methods and the lack of standardized guidelines and protocols for digital pathology can impede its implementation.

Market Segmentation

- In 2022, the device segment accounted for around 48.2% market share

On the basis of the product, the global digital pathology market is segmented into software, device, and storage system. The device segment held the largest share in the digital pathology market, accounting for a significant portion of the overall market. Several factors contribute to the dominance of the device segment, the development and adoption of advanced digital pathology devices have revolutionized the way pathology is practiced. These devices include slide scanners, whole-slide imaging systems, and digital microscope systems, which enable the acquisition and digitization of high-resolution pathology images. They offer benefits such as improved workflow, remote access to images, and enhanced collaboration among pathologists. The continuous advancements in digital imaging technology have contributed to the growth of the device segment. Manufacturers are constantly introducing innovative devices with improved image quality, faster scanning speeds, and higher throughput, making them more efficient and reliable for pathology applications. The increasing demand for digital pathology devices is driven by the growing need for accurate and timely diagnosis, especially in the field of oncology. Digital pathology devices allow pathologists to review and analyze digitized slides, enabling faster and more precise diagnosis, leading to better patient outcomes. Furthermore, the device segment's dominance can be attributed to the rising investments in healthcare infrastructure, particularly in developed regions like North America and Europe. Hospitals, clinics, and research laboratories are investing in digital pathology devices to improve their diagnostic capabilities and enhance operational efficiency. Overall, the device segment's largest share underscores the pivotal role played by digital pathology devices in transforming pathology practice, improving diagnostics, and driving the growth of the digital pathology market.

- In 2022, the ABC segment dominated with more than 43.6% market share

Based on the application, the global digital pathology market is segmented into drug discovery & development, academic research, and disease diagnosis. The academic research segment has emerged as the dominant player in the digital pathology market, holding the largest share. The academic research institutions play a crucial role in driving technological advancements and innovation in the field of digital pathology. These institutions have the resources, expertise, and infrastructure to conduct extensive research and development activities, pushing the boundaries of digital pathology technology and applications. Academic research institutions are at the forefront of pathology education and training. Digital pathology offers significant benefits in education, allowing students and trainees to access digitized slides for learning and practice. Academic institutions leverage digital pathology systems and software to provide comprehensive training and develop skilled pathologists who can adapt to the evolving landscape of pathology practice. Furthermore, academic research institutions serve as centers of collaboration and knowledge exchange among pathologists and researchers. The digitization of pathology images enables seamless sharing of data and collaboration on research projects, facilitating scientific advancements in the field. Additionally, academic research institutions often have established relationships with industry players, fostering collaborations for technology development and commercialization. This further contributes to the dominance of the academic research segment in the market. Moreover, academic research institutions receive grants and funding for research projects, which can be allocated towards the adoption and implementation of digital pathology solutions. This financial support enables these institutions to invest in state-of-the-art equipment, software, and infrastructure required for digital pathology, further solidifying their dominant position in the market. Overall, the academic research segment's dominance highlights its pivotal role in driving the advancements, education, and collaborative efforts in the field of digital pathology.

Regional Segment Analysis of the Digital Pathology Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America dominated the market with more than 40.6% revenue share in 2022.

Get more details on this report -

Based on region, North America has emerged as a dominant player in the overall digital pathology market. North America boasts a well-developed healthcare infrastructure with advanced diagnostic capabilities, which creates a conducive environment for the adoption of digital pathology solutions. Additionally, the region has a high prevalence of chronic diseases, driving the demand for accurate and efficient diagnostic techniques like digital pathology. Furthermore, North America is home to several leading market players and technology innovators in the field of digital pathology, fostering research and development activities, and driving market growth. Moreover, favorable government initiatives and investments in healthcare IT and digitalization further support the growth of the digital pathology market in the region. Finally, the presence of skilled healthcare professionals and a strong emphasis on technological advancements contribute to North America's leadership position in the digital pathology market.

Recent Developments

- In June 2023, Minerva Imaging recently formed a strategic collaboration with Visiopharm, focusing on AI-driven image analysis. This partnership aims to leverage Visiopharm's Oncotopix platform, which utilizes artificial intelligence, to develop robust predictive assays in the field of pathology. By combining Minerva Imaging's expertise and Visiopharm's advanced AI capabilities, the collaboration seeks to enhance the accuracy and efficiency of image analysis for improved diagnostics and personalized treatment in pathology.

- In March 2023, Agilent Technologies Inc. announced a strategic partnership with Hamamatsu Photonics K.K., one of the top manufacturers of whole slide imaging systems, to integrate the brand's NanoZoomer line, as well as the S360MD Slide scanner system, into Agilent's end-to-end digital pathology solution.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the global digital pathology market along with a comparative evaluation primarily based on their product offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Companies:

- Leica Biosystems Nussloch GmbH

- Hamamatsu Photonics, Inc.

- Koninklijke Philips N.V.

- Olympus Corporation

- F. Hoffmann-La Roche Ltd.

- Mikroscan Technologies, Inc.

- Inspirata, Inc.

- Epredia

- Visiopharm A/S

- Huron Technologies International Inc.

- ContextVision AB

Key Target Audience

- Market Players

- Investors

- End-Users

- Government Authorities

- Consulting and Research Firm

- Venture Capitalists

- Value-Added Resellers (VARs)

Market Segment

This study forecasts revenue at global, regional, and country levels from 2019 to 2032. Spherical Insights has segmented the Global Digital Pathology Market based on the below-mentioned segments:

Digital Pathology Market, By Product

- Software

- Device

- Storage System

Digital Pathology Market, By Application

- Drug Discovery & Development

- Academic Research

- Disease Diagnosis

Digital Pathology Market, By End-Use

- Hospitals

- Biotech & Pharma Companies

- Diagnostic Labs

- Academic & Research Institutes

Digital Pathology Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East & Africa

Need help to buy this report?