Global Automotive Corner Detecting And Ranging System Market Size, Share, By System Type (Corner Detecting Systems, Passive Corner Detecting Systems, and Combined Corner Detecting & Ranging Systems), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Two Wheelers, and Off-Highway Vehicles), By Application (Advanced Driver Assistance System, Autonomous Driving, Parking Assistance, Safety & Collision Avoidance, Navigation & Mapping, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035

Industry: Automotive & TransportationGlobal Automotive Corner Detecting And Ranging System Market Insights Forecasts to 2035

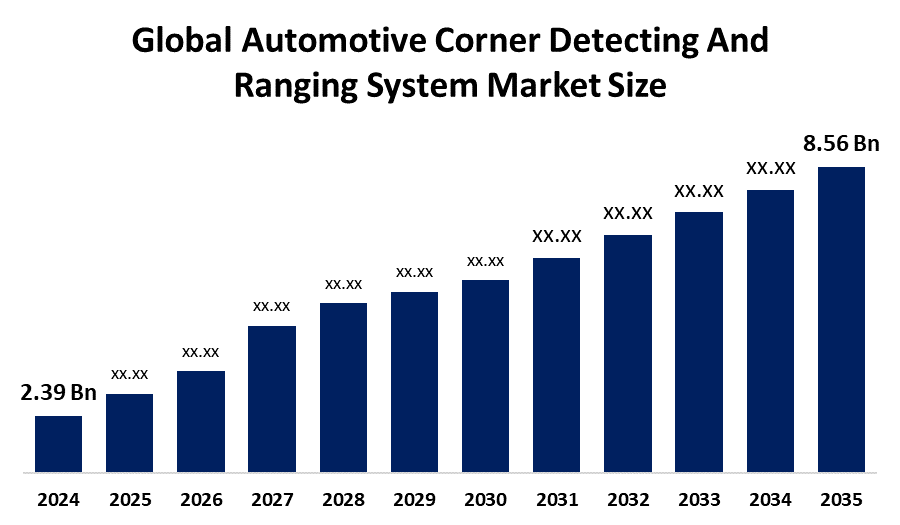

- The Global Automotive Corner Detecting And Ranging System Market Size Was Estimated at USD 2.39 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 12.3% from 2025 to 2035

- The Worldwide Automotive Corner Detecting And Ranging System Market Size is Expected to Reach USD 8.56 Billion by 2035

- Asia Pacific is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global automotive corner detecting and ranging system market size was worth around USD 2.39 billion in 2024 and is predicted to grow to around USD 8.56 billion by 2035 with a compound annual growth rate (CAGR) of 12.3% from 2025 to 2035. Global advancements in sensors, improvements in miniaturization, cost reduction, and signal processing, and growth of ADAS, electric, and autonomous vehicles are all driving opportunities in the automotive corner detecting and ranging system market.

Market Overview

The automotive corner detecting and ranging system market refers to the industry that develops technologies which allow vehicles to detect objects and determine their distance from the vehicle using sensors such as radar, LiDAR cameras, and ultrasonic systems. The system requires hardware components which include sensors, control units, and software that consists of AI algorithms and signal processing functions together with advanced driver-assistance systems (ADAS) and autonomous driving platforms. The market is expanding due to sensor fusion advancements, artificial intelligence developments, and electric self-driving vehicle adoption that create requirements for complete 360 degree situational awareness which ensures safe operation and efficient navigation.

Government policies establish mandatory vehicle safety requirements that support autonomous vehicle research and development while creating regulatory frameworks that promote system adoption and ensure reliability and road safety.

For instance, in August 2022, the U.S. Department of Transportation introduced the Safe Streets and Roads for All (SS4A) Grant Program under the Infrastructure Investment and Jobs Act (IIJA), allocating USD 5 billion for fiscal years 2022–2026 to support local and tribal safety initiatives and reduce roadway fatalities and serious injuries.

Similarly, in November 2021, Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) mandated that all new passenger vehicles sold in the country must be equipped with automatic emergency braking (AEB) systems. This requirement highlights the importance of advanced driver assistance systems (ADAS), which enhance vehicle safety through technologies such as radar and LiDAR-based object detection.

Therefore, the rapid pace of technological advancement is a key driver of the growth of the automotive corner detecting and ranging system market.

Report Coverage

This research report categorizes the automotive corner detecting and ranging system market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the automotive corner detecting and ranging system market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the automotive corner detecting and ranging system market.

Global Automotive Corner Detecting And Ranging System Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 2.39 billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR of 12.3% |

| 2035 Value Projection: | USD 8.56 billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 158 |

| Tables, Charts & Figures: | 123 |

| Segments covered: | By System Type,By Vehicle Type,By Application |

| Companies covered:: | Robert Bosch GmbH, Continental AG, Valeo SA, Aptiv PLC, ZF Friedrichshafen AG, Autoliv Inc., Sensata Technologies, Magna International Inc., Texas Instruments, NXP Semiconductors N.V., Infineon Technologies AG, Texas Instruments Incorporated, Mobileye N.V., Hitachi Automotive Systems, Ltd., and other key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

Rapid technological innovation is one of the main drivers of the automotive corner detecting and ranging system market's growth. Rapid adoption of advanced driver assistance systems and continuous technological advancements that enhance detection accuracy and reduce system costs, which is the main factor driving the market for automotive corner detecting and ranging system. In this field, innovation and investment are driven by the governments and private players in smart transportation, connected vehicles, and autonomous driving programs. The combination of increasing consumer demands for vehicle protection and collision avoidance systems together with the growth of electric and autonomous vehicle markets creates higher requirements for accurate environmental perception technology. The combination of these elements creates a strong ecosystem which supports global adoption of automotive corner detecting and ranging systems worldwide.

In March 2025, India’s MoRTH issued a draft proposal which requires all newly manufactured passenger vehicles exceeding eight seats buses and trucks to include Advanced Driver Assistance Systems which must contain Advanced Emergency Braking System, Driver Drowsiness and Attention Warning System, and Lane Departure Warning System.

Restraining Factors

High development and deployment costs, terahertz frequency technology complexity, standardization and regulatory variations, technical challenges, limited awareness among consumers, and cybersecurity and data privacy concerns, and supply chain constraints are the main factors restricting the automotive corner detecting and ranging system market.

Market Segmentation

The automotive corner detecting and ranging system market share is classified into system type, vehicle type, and application

- The combined corner detecting and ranging systems segment dominated the market in 2024, approximately 50%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the system type, the automotive corner detecting and ranging system market is divided into active corner detecting systems, passive corner detecting systems, and combined corner detecting and ranging systems. Among these, the combined corner detecting and ranging systems segment dominated the market in 2024, approximately 50%, and is projected to grow at a substantial CAGR during the forecast period. Integration of active sensing and passive system technologies offers higher accuracy, wider detection range, and improved reliability in various driving conditions, and meets stringent government and safety regulations, which is driving the combined corner detecting and ranging systems industry.

- The passenger vehicles segment accounted for the largest share in 2024, approximately 55%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the vehicle type, the automotive corner detecting and ranging system market is divided into passenger vehicles, commercial vehicles, two-wheelers, and off-highway vehicles. Among these, the passenger vehicles segment accounted for the largest share in 2024, approximately 55%, and is anticipated to grow at a significant CAGR during the forecast period. The highest global production volume, primary focus of government-mandated safety regulations, increasing consumer demand for advanced safety features, and widespread adoption of ADAS is driving the passenger vehicles industry.

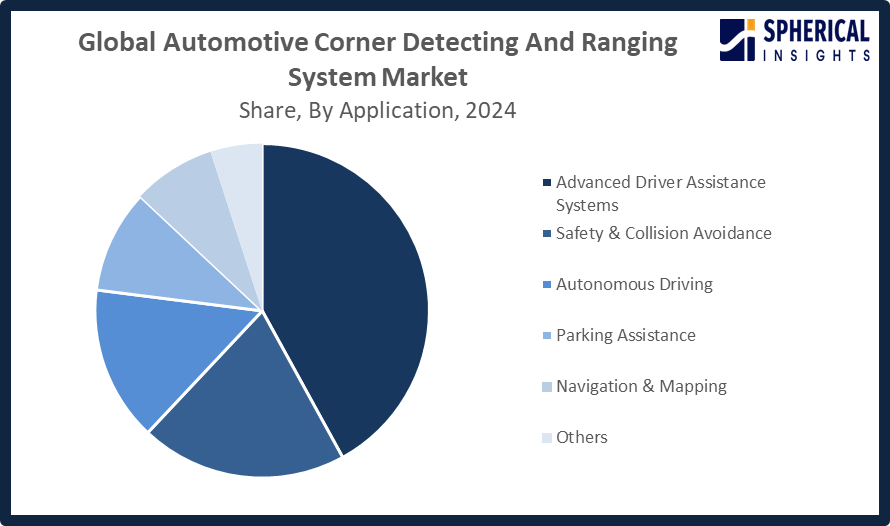

- The advanced driver assistance systems segment accounted for the highest market revenue in 2024, approximately 25%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the automotive corner detecting and ranging system market is divided into advanced driver assistance systems, autonomous driving, parking assistance, safety & collision avoidance, navigation & mapping, and others. Among these, the advanced driver assistance systems segment accounted for the highest market revenue in 2024, approximately 25%, and is anticipated to grow at a significant CAGR during the forecast period. Increased demand by consumers for safety, widely mandated by governments, rely heavily on corner detecting and ranging technologies, and their early adoption across passenger and commercial vehicles is bolstering advanced driver assistance systems market.

Get more details on this report -

Regional Segment Analysis of the Automotive Corner Detecting And Ranging System Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

North America is anticipated to hold the largest share of the automotive corner detecting and ranging system market over the predicted timeframe.

North America is anticipated to hold the largest share of the automotive corner detecting and ranging system market over the predicted timeframe. Strong government backing for automatic emergency braking, lane departure warning, and blind-spot monitoring in new vehicles are what propel North America. The region gains advantages from high consumer awareness and their preference for vehicle safety technologies, principal automotive manufacturers, and first-tier suppliers who conduct extensive research and development activities. The system receives its effective operational capabilities which include well-established road systems and advanced transportation smart technologies. The economic situation enables consumers to purchase vehicles that come with modern sensing equipment which further establishes North America's market leadership.

Government initiatives include Canada’s Safety Framework for Connected and Automated Vehicles 2.0, February 2025, establishes policy guidelines which enable both innovation and safety standards for connected and automated vehicles and their advanced sensing and perception technology and U.S. NHTSA’s, April 2024, AEB mandate that vehicles must have object detection systems which use sensors and processing to identify objects and measure their distance from the vehicle.

Asia Pacific is expected to grow at a rapid CAGR in the automotive corner detecting and ranging system market during the forecast period. China, India, Japan, and South Korea are among the nations making significant investments to develop vehicle production capacity, demand for safety technologies, and increased government commitment to vehicle safety regulations. The combination of strong economic growth and rising disposable incomes drives vehicle sales while governments implement safety requirements and offer incentives for electric vehicles and connected vehicles that use corner detection and ranging technologies. The growth of the Asia Pacific region depends on manufacturers and suppliers who establish operations and research development centers in the area while implement advanced driver assistance systems and autonomous vehicle technology.

Government launches include India’s MRTH, February 2026, mandates Advanced Emergency Braking Systems and Electronic Stability Control for medium and heavy commercial vehicles, Japan’s MLIT, January 2026 announced updated safety standards for ACPE systems to enhance vehicle sensor use boosting demand for advanced detection and ranging systems, and South Korea’s MOLIT’s September 2025, introduced updated vehicle safety and autonomous regulations, requiring ADAS and collision avoidance functions in autonomous vehicles across various testing and deployment programs.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the automotive corner detecting and ranging system market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Aptiv PLC

- ZF Friedrichshafen AG

- Autoliv Inc.

- Sensata Technologies

- Magna International Inc.

- Texas Instruments

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Texas Instruments Incorporated

- Mobileye N.V.

- Hitachi Automotive Systems, Ltd.

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

- In February 2026, Waymo introduced its sixth generation autonomous driving system, which includes improved radar and lidar sensors that enable precise object detection in various environmental conditions, which speeds up the actual deployment of high-accuracy sensor systems.

- In January 2026, Texas Instruments introduced a complete range of automotive radar and computer chips which specifically contain high resolution radar transceivers and AI edge SoCs designed to enable advanced vehicle platform sensing and environmental perception capabilities that support corner detection and ADAS operations.

- In April 2025, Texas Instruments launched a new portfolio of automotive chips which includes the AWR2944P mmWave radar sensor that provides enhanced front and corner radar capabilities together with its built-in high speed lidar laser driver that improves ADAS performance and corner detection accuracy.

- In March 2025, Bosch GmbH and Valeo SA announced a partnership to co-develop next generation corner radar modules and sensor fusion software which will improve 360 degree vehicle awareness that serves as a fundamental component of corner detection systems and ranging systems.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the automotive corner detecting and ranging system market based on the below-mentioned segments:

Global Automotive Corner Detecting And Ranging System Market, By System Type

- Active Corner Detecting Systems

- Passive Corner Detecting Systems

- Combined Corner Detecting & Ranging Systems

Global Automotive Corner Detecting And Ranging System Market, By Vehicle

- Passenger Vehicles

- Commercial Vehicles

- Two Wheelers

- Off-Highway Vehicles

Global Automotive Corner Detecting And Ranging System Market, By Application

- Advanced Driver Assistance Systems

- Autonomous Driving

- Parking Assistance

- Safety & Collision Avoidance

- Navigation & Mapping

- Others

Global Automotive Corner Detecting And Ranging System Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Need help to buy this report?