Global Aniline Derivatives Market Size, Share, and COVID-19 Impact Analysis, By Derivative Type (Aniline, Nitroaniline, Chloroaniline, Toluidine, and Others), By Application (Rubber Chemicals, Dyes Pigments, Pharmaceuticals, Agrochemicals, and Others), By End User (Automotive, Textile, Pharmaceutical, Agriculture, and Others), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2025 - 2035.

Industry: Chemicals & MaterialsGlobal Aniline Derivatives Market Insights Forecasts to 2035

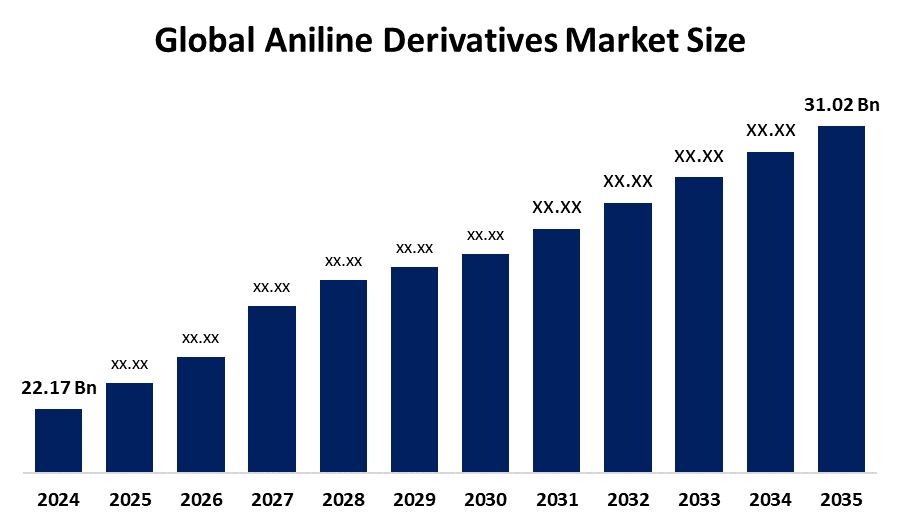

- The Global Aniline Derivatives Market Size Was Estimated at USD 22.17 Billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 3.1% from 2025 to 2035

- The Worldwide Aniline Derivatives Market Size is Expected to Reach USD 31.02 Billion by 2035

- North America is expected to grow the fastest during the forecast period.

Get more details on this report -

According to a research report published by Spherical Insights and Consulting, the global aniline derivatives market size was worth around USD 22.17 billion in 2024 and is predicted to grow to around USD 31.02 billion by 2035 with a compound annual growth rate (CAGR) of 3.1% from 2025 to 2035. Global expansion of catalytic processes, digital transformation, eco-friendly manufacturing methods, innovations in producing MDI for polyurethane insulation, and expansion of high performance rubber chemicals for the automotive sector are all driving opportunities in the aniline derivatives market.

Market Overview

The aniline derivatives market refers to the global industry involved in the production, distribution, and application of chemicals derived from aniline, which is an aromatic amine that originates from benzene and functions as a vital component for manufacturing products that include methylene diphenyl diisocyanate, which is used in polyurethane foams, rubber processing chemicals, dyes and pigments, pharmaceutical products, agrochemical substances, and specialized chemical compounds. The market consists of various segments which include construction materials, automotive components, textiles, packaging, and agricultural inputs to which these derivatives are extensively utilized. The market presents growth opportunities due to rising polyurethane demand for insulation and furniture products, expansion of the automotive and construction industries, increased adoption of high performance materials, and the development of sustainable bio based chemical applications in emerging markets.

The government supply chain for the aniline derivatives market receives its main support from domestic chemical manufacturing policies, infrastructure development programs, industrial growth subsidies, and environmental regulations which promote safe production methods and research and development incentives which together create an environment that fosters innovation, regulatory compliance, and supply chain development. For example, in March 2026, India’s PLI scheme outlay of INR 6940 crore for bulk drugs and intermediates, with ongoing investments and commissioned projects supports the domestic chemical production capacity and December 2025 PLI Scheme for Bulk Drugs, INR 4763.34 crore investment had already been made in domestic manufacturing of chemical intermediates and related products, which strengthens the supply chain for derivatives like aniline.

In September 2024, the U.S. Department of Defense initiated funding programs offering up to USD 24 million per project to expand domestic production of critical chemicals including dyes and intermediates, which directly strengthens the supply chain for derivatives like aniline.

The quick speed of technological advancement is one of the main drivers of the aniline derivatives market's expansion.

Report Coverage

This research report categorizes the aniline derivatives market based on various segments and regions, forecasts revenue growth, and analyzes trends in each submarket. The report analyses the key growth drivers, opportunities, and challenges influencing the aniline derivatives market. Recent market developments and competitive strategies, such as expansion, product launch, development, partnership, merger, and acquisition, have been included to draw the competitive landscape in the market. The report strategically identifies and profiles the key market players and analyses their core competencies in each sub-segment of the aniline derivatives market.

Global Aniline Derivatives Market Report Coverage

| Report Coverage | Details |

|---|---|

| Base Year: | 2024 |

| Market Size in 2024: | USD 22.17 Billion |

| Forecast Period: | 2025-2035 |

| Forecast Period CAGR 2025-2035 : | CAGR Of 3.1% |

| 2035 Value Projection: | USD 31.02 Billion |

| Historical Data for: | 2020-2023 |

| No. of Pages: | 188 |

| Tables, Charts & Figures: | 118 |

| Segments covered: | By Derivative Type,By End User,By Application |

| Companies covered:: | BASF SE, Covestro AG, Wanhua Chemical Group Co., Ltd., Huntsman Corporation, Sumitomo Chemical Co., Ltd., Dow Company, Mitsui Chemicals Co., Ltd., Tosoh Corporation, LANXESS, Aarti Industries Ltd., Bondalti, SP Chemicals Holdings Ltd., Jilin Conell Chemical Industry Co., Ltd., SABIC, GNFC Limited, and Other key players |

| Pitfalls & Challenges: | COVID-19 Empact, Challenge, Future, Growth, & Analysis |

Get more details on this report -

Driving Factors

Rapid technological innovation is one of the main drivers of the aniline derivatives market's growth. The factor driving the market for aniline derivatives comes from the increased usage of aniline derivatives for insulation purposes in furniture and automotive parts, ongoing development of urban areas, and infrastructure systems in developing countries. The pharmaceutical industry growth together with technological progress rising demand for specialty chemicals and high value chemicals, and the present shift toward sustainable materials and energy efficient products drive innovation and investment in this field. The market growth results from government policies in chemical manufacturing investments and increasing foreign direct investment.

In May 2022, the U.S. Department of Energy launched the Net-Zero Labs Pilot Initiative with initial funding of USD 38 million to develop technologies which will help decarbonize industrial and energy intensive facilities of chemical manufacturing plants and In 2020, the Indian government established the Bulk Drug Parks Scheme with total funding of INR 3000 crore to create shared facilities which will support chemical and pharmaceutical manufacturing hubs as well as their associated downstream product development.

Restraining Factors

High development and deployment costs, environmental and health concerns, strict government regulations, fluctuations in crude oil prices, supply chain disruptions, geopolitical uncertainties, and operational risks in chemical manufacturing facilities are the main factors restricting the aniline derivatives market.

Market Segmentation

The aniline derivatives market share is classified into component, application, and end user.

- The aniline segment dominated the market in 2024, approximately 75%, and is projected to grow at a substantial CAGR during the forecast period.

Based on the derivative type, the aniline derivatives market is divided into aniline, Nitroaniline, Chloroaniline, toluidine, and others. Among these, the aniline segment dominated the market in 2024, approximately 75%, and is projected to grow at a substantial CAGR during the forecast period. The growing need as a precursor for methylene diphenyl diisocyanate, booming construction and automotive industries, rapid urbanization, crucial for synthesizing various pharmaceutical products, and essential for producing rubber chemicals is driving the aniline industry.

- The rubber chemicals segment accounted for the largest share in 2024, approximately 32%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the application, the aniline derivatives market is divided into rubber chemicals, dyes pigments, pharmaceuticals, agrochemicals, and others. Among these, the rubber chemicals segment accounted for the largest share in 2024, approximately 32%, and is anticipated to grow at a significant CAGR during the forecast period. Massive demand for high performance tires, automotive components, and industrial belts, crucial for vulcanization, and increasing the durability, elasticity, and strength of rubber products in automotive sector is driving the rubber chemicals industry.

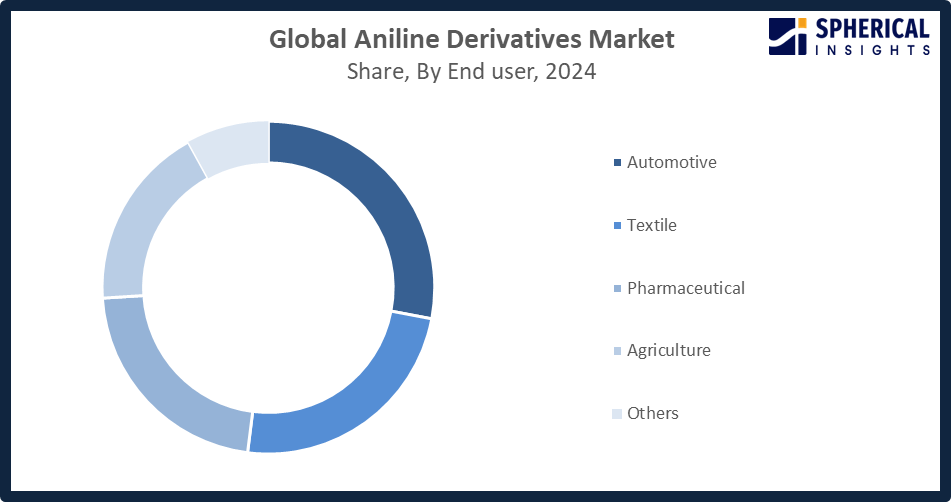

- The automotive segment accounted for the highest market revenue in 2024, approximately 30%, and is anticipated to grow at a significant CAGR during the forecast period.

Based on the end user, the aniline derivatives market is divided into automotive, textile, pharmaceutical, agriculture, and others. Among these, the automotive segment accounted for the highest market revenue in 2024, approximately 30%, and is anticipated to grow at a significant CAGR during the forecast period. Increased demand for polyurethane foams in vehicle interiors, need for lightweight materials, increased vehicle production, and the usage of rubber chemicals for tires is bolstering automotive market.

Get more details on this report -

Regional Segment Analysis of the Aniline Derivatives Market

- North America (U.S., Canada, Mexico)

- Europe (Germany, France, U.K., Italy, Spain, Rest of Europe)

- Asia-Pacific (China, Japan, India, Rest of APAC)

- South America (Brazil and the Rest of South America)

- The Middle East and Africa (UAE, South Africa, Rest of MEA)

Asia Pacific is anticipated to hold the largest share of the aniline derivatives market over the predicted timeframe.

Asia Pacific is anticipated to hold the largest share of the aniline derivatives market over the predicted timeframe. The Asia Pacific region develops through government support which drives industrialization and urbanization in China and India and Japan. The region attracts manufacturers from both domestic and international sources because it offers inexpensive labor and plentiful raw materials with strong government policies which provide investment incentives and develop industrial infrastructure. The region maintains its leadership position in the worldwide aniline derivatives market through its extensive chemical manufacturing centers and high export capacity.

Government initiatives the Chinese government made public its petrochemical development objectives and industrial advancement plans through its MIIT in September 2025, the Department of Chemicals and Petrochemicals in India expanded PCPIR chemical parks in December 2025 to boost domestic production capabilities, and the Chemical Substances Control Law which METI in Japan updated became operational in February 2022 to establish safer chemical production methods and support aniline derivatives market development.

North America is expected to grow at a rapid CAGR in the aniline derivatives market during the forecast period. The U.S. and Canadian markets experience growth because of their increasing interest in advanced polyurethane applications, insulation materials and lightweight composite materials. Government initiatives together with funding programs that support domestic chemical manufacturing, supply chain resilience, and sustainable production technologies create an environment that attracts investment while companies expand their operations. North America serves as the fastest developing market because its chemical infrastructure, research facilities and innovative product development systems enable quick market entry for new chemical derivatives.

Government launches include The U.S. EPA launched the Green Chemistry Program in January 2026 to promote sustainable chemical technologies and the DOE introduced a USD 6 billion IDP in March 2024 to assist heavy industries including chemicals and manufacturing. The Chemicals Management Plan established by the Canadian government creates a controlled framework for chemical safety and industrial development which supports the aniline derivative market.

Competitive Analysis:

The report offers the appropriate analysis of the key organizations/companies involved within the aniline derivatives market, along with a comparative evaluation primarily based on their product of offering, business overviews, geographic presence, enterprise strategies, segment market share, and SWOT analysis. The report also provides an elaborative analysis focusing on the current news and developments of the companies, which includes product development, innovations, joint ventures, partnerships, mergers & acquisitions, strategic alliances, and others. This allows for the evaluation of the overall competition within the market.

List of Key Companies

- BASF SE

- Covestro AG

- Wanhua Chemical Group Co., Ltd.

- Huntsman Corporation

- Sumitomo Chemical Co., Ltd.

- Dow Company

- Mitsui Chemicals Co., Ltd.

- Tosoh Corporation

- LANXESS

- Aarti Industries Ltd.

- Bondalti

- SP Chemicals Holdings Ltd.

- Jilin Conell Chemical Industry Co., Ltd.

- SABIC

- GNFC Limited

- Others

Key Target Audience

- Market Players

- Investors

- End-users

- Government Authorities

- Consulting and Research Firm

- Venture capitalists

- Value-Added Resellers (VARs)

Recent Development

• In February 2026, BASF announced the expansion of its dispersions production capacity at its Mangalore site in India. The new production line will boost the supply of high-performance dispersions used in coatings and construction chemicals. This expansion will also support an extended derivative supply network.

• In September 2024, BASF partnered with Future Foam to develop the first flexible foam product using 100% biomass-balanced TDI, produced at its Geismar, Louisiana facility. This innovation marks a significant step toward sustainability by utilizing eco-friendly feedstocks.

• In July 2024, Covestro and Neste announced a collaboration to produce bio-based aniline using renewable feedstocks, achieving up to a 90% reduction in carbon footprint compared to conventional petrochemical methods.

• In May 2024, Huntsman Corporation acquired specialty chemical assets for USD 1.1 billion, strengthening its portfolio of aniline-based products for the electronics and automotive sectors.

• In May 2024, Wanhua Chemical Co., Ltd. inaugurated a new aniline production facility in Yantai, China, with an annual capacity of 400,000 metric tons. The facility utilizes advanced catalytic technology to enhance energy efficiency and reduce waste.

• In January 2024, Dow entered into a strategic collaboration with Ford Motor Company to develop advanced polyurethane foam formulations for electric vehicles, leveraging aniline derivatives for improved thermal management and lightweight components.

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the aniline derivatives market based on the below-mentioned segments:

Global Aniline Derivatives Market, By Derivative Type

- Aniline

- Nitroaniline

- Chloroaniline

- Toluidine

- Others

Global Aniline Derivatives Market, By Application

- Rubber Chemicals

- Dyes Pigments

- Pharmaceuticals

- Agrochemicals

- Others

Global Aniline Derivatives Market, By End User

- Automotive

- Textile

- Pharmaceutical

- Agriculture

- Others

Global Aniline Derivatives Market, By Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

Need help to buy this report?