Global Space Launch Services Market Size To worth USD 11.2 billion by 2033 | CAGR of 6.26%

Category: Aerospace & DefenseGlobal Space Launch Services Market worth $11.2 billion by 2033

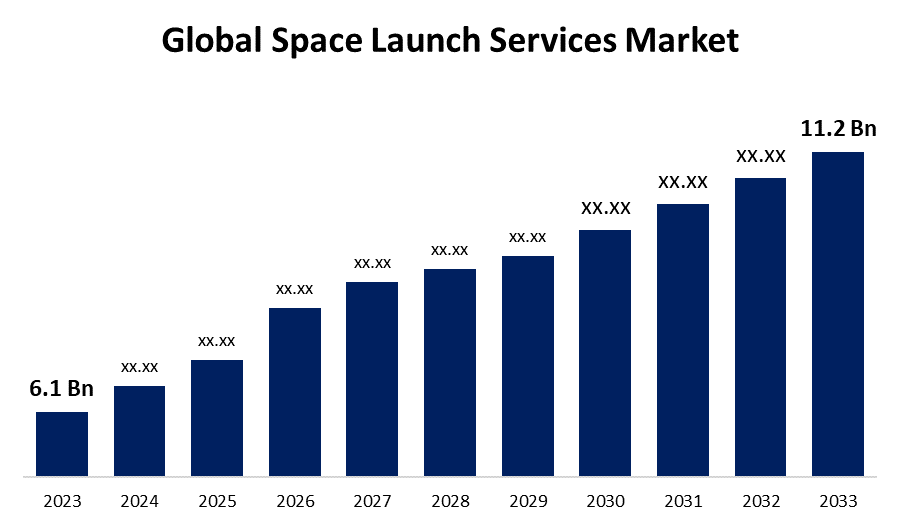

According to a research report published by Spherical Insights & Consulting, The Global Space Launch Services Market Size to grow from USD 6.1 billion in 2023 to USD 11.2 billion by 2033, at a Compound Annual Growth Rate (CAGR) of 6.26% during the forecast period.

Get more details on this report -

Browse key industry insights spread across 238 pages with 119 Market data tables and figures & charts from the report on the "Global Space Launch Services Market Size, Share, and COVID-19 Impact Analysis, By Orbit Type (LEO, GEO, and Others), By Launch Vehicle (Small Lift Launch Vehicle, Medium Lift Launch Vehicle, and Heavy Lift Launch Vehicle), By Payload (Satellite, Cargo, Human Spacecraft, and Testing Probes), By End User (Civil & Military and Commercial), and By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa), Analysis and Forecast 2023 - 2033." Get Detailed Report Description Here: https://www.sphericalinsights.com/reports/space-launch-services-market

The space launch services market is experiencing robust growth, driven by a surge in satellite deployments, innovations in reusable launch technologies, and escalating investments from both government and commercial sectors in space exploration. The demand for small satellite launches, particularly in telecommunications, Earth observation, and navigation, is growing rapidly. Leading companies like SpaceX, Blue Origin, and ULA are concentrating on cost-effective, reusable launch systems to improve access to space. Government agencies such as NASA, ESA, and ISRO are also increasing investments in deep-space exploration and fostering commercial partnerships. Additionally, the growth of private space tourism and lunar exploration is shaping the market's future. Despite this, challenges such as high launch costs, regulatory hurdles, and environmental concerns remain significant. The market is poised for evolution with ongoing technological progress and greater international collaboration.

Space Launch Services Market Value Chain Analysis

The space launch services market value chain involves several interconnected stages, starting with raw material and component suppliers who provide key elements such as composite materials, propulsion systems, and avionics. Following this, launch vehicle manufacturers like SpaceX, ULA, and Rocket Lab design and build rockets with advanced engineering techniques. Launch service providers handle mission planning, payload integration, and the execution of launches for both government and commercial clients. Ground support and infrastructure, which includes spaceports, tracking stations, and communication networks, ensure operational efficiency. Regulatory bodies, such as NASA, ESA, and the FAA, enforce compliance and safety standards. Finally, end-users, including satellite operators, defense agencies, and space tourism companies, rely on launch services for applications such as telecommunications, Earth observation, and deep-space missions. Cooperation across these stages fosters industry efficiency and drives innovation.

Space Launch Services Market Opportunity Analysis

The space launch services market offers substantial growth opportunities, driven by rising demand for satellite deployments, deep-space exploration, and commercial space activities. The growing use of small satellites and large-scale constellations for communication, Earth observation, and IoT applications is propelling market growth. Innovations in reusable rocket technology by companies like SpaceX and Blue Origin are reducing costs and increasing accessibility to space. New revenue streams are emerging from space tourism, lunar exploration, and asteroid mining. Government programs and public-private collaborations are fostering further advancements in launch services. Additionally, progress in hypersonic travel and interplanetary missions presents long-term potential. However, challenges such as regulatory hurdles, space debris management, and cost efficiency must be addressed to maintain growth. The market is set for continued expansion with growing global involvement.

SpaceX, Blue Origin, and Rocket Lab are transforming the industry through reusable rocket technology, cutting launch costs and enhancing space accessibility. Private companies are also collaborating with government agencies such as NASA and ESA for satellite launches, deep-space missions, and lunar exploration. The rising demand for commercial satellite deployment, space tourism, and interplanetary exploration is further driving market growth. Venture capital and corporate investments are fueling innovations in propulsion systems, small satellite launches, and hypersonic travel. With intensifying competition, the industry is set to experience rapid technological advancements, making space more accessible for commercial, scientific, and defense purposes.

High launch costs continue to be a significant challenge, limiting access for smaller companies and emerging markets. Regulatory hurdles, including stringent safety and environmental standards, create delays for new entrants and complicate launch approval processes. The growing issue of space debris increases collision risks and requires advanced mitigation measures. Technical difficulties, such as propulsion failures, payload integration problems, and mission delays, also affect operational efficiency. Geopolitical tensions and fluctuating government funding can further impact market stability. The dominance of a few major players intensifies competition, making it hard for startups to break into the market. Overcoming these obstacles through cost reduction, policy adjustments, and technological innovation will be key to ensuring long-term growth in the sector.

Insights by Orbit Type

The LEO segment accounted for the largest market share over the forecast period 2023 to 2033. LEO, which spans from 180 to 2,000 km above Earth, is favored for communication, Earth observation, and navigation satellites because of its low latency and cost efficiency. Companies like SpaceX (Starlink), OneWeb, and Amazon (Project Kuiper) are leading the deployment of LEO satellites for global broadband coverage. Government agencies such as NASA and ISRO are also focusing on LEO for research and space station projects. The growth of small satellite launches and advancements in reusable rocket technology are further driving expansion in LEO. However, challenges such as space debris and orbital congestion require advanced mitigation strategies to support the sustainable growth of this rapidly developing segment.

Insights by Launch Vehicle

The heavy lift launch vehicle segment accounted for the largest market share over the forecast period 2023 to 2033. Heavy lift launch vehicles (HLVs), designed to carry large and multiple payloads to geostationary orbits and beyond, are essential for deploying satellite constellations, deep-space exploration, and large-scale infrastructure projects. Leading players like SpaceX’s Falcon Heavy, ULA’s Delta IV Heavy, and NASA’s Space Launch System (SLS) are driving innovations in HLV technology. The growing demand for both government and private sector missions, including interplanetary exploration and lunar landings, further accelerates market growth. Although the cost of launching heavy payloads remains high, technological advancements such as reusability and cost-reduction strategies are making HLVs increasingly viable for both commercial and governmental purposes.

Insights by Payload

The satellite segment accounted for the largest market share over the forecast period 2023 to 2033. The growing demand for small satellites, especially for communication networks and Internet of Things (IoT) services, has fueled a surge in commercial satellite launches. Companies such as SpaceX, Rocket Lab, and Arianespace are actively deploying satellite constellations, including SpaceX's Starlink, which aims to provide worldwide broadband coverage. Government agencies like NASA and ESA also play a significant role in the market, supporting missions related to communication satellites, space exploration, and environmental monitoring. The shift toward cost-efficient, reusable launch systems is further accelerating satellite deployment, enhancing space accessibility for both commercial and governmental organizations.

Insights by End User

The commercial segment accounted for the largest market share over the forecast period 2023 to 2033. The growing deployment of small satellite constellations for global communications, IoT services, and Earth observation is creating substantial market opportunities. Additionally, the rising interest in space tourism, driven by companies like Virgin Galactic and Blue Origin, is contributing to the expansion of the commercial space sector. Venture capital investments and the increasing commercialization of space missions, such as lunar and Mars exploration, are driving innovation and improving accessibility. As private companies form more partnerships with government agencies, the commercial segment is poised to play a crucial role in shaping the future of space exploration and commercialization.

Insights by Region

Get more details on this report -

North America is anticipated to dominate the Space Launch Services Market from 2023 to 2033. The rising demand for small satellite launches, deep-space exploration, and space tourism is driving further market growth. Innovations in reusable rocket technology and public-private partnerships are improving cost efficiency and fostering innovation. The U.S. government's backing of space commercialization, coupled with collaborations with Canada's space sector, bolsters regional growth. However, regulatory hurdles and increasing competition from other regions continue to be important factors for market expansion.

Asia Pacific is witnessing the fastest market growth between 2023 to 2033. China’s CNSA and private companies like iSpace and LandSpace are making strides in reusable rocket technology and satellite deployment. India’s ISRO, along with private startups like Skyroot Aerospace, is enhancing low-cost launch capabilities. Japan’s JAXA is also advancing innovative launch systems, including collaborations for lunar exploration. The growing demand for satellite-based communication, Earth observation, and navigation services is driving market growth. Emerging players from South Korea and Australia are also entering the market. However, regulatory challenges, competition from Western companies, and the need for cost-effective launch solutions remain crucial factors influencing the market’s future development.

Recent Market Developments

- In July 2023, Land Space, a private Chinese company, has successfully developed and launched the world’s first methane-liquid oxygen rocket into orbit. The Suzaku-2 rocket took off from the Jiuquan Satellite Launch Center in northwestern China at 9 am, completing its flight successfully.

Major players in the market

- SpaceX

- Blue Origin

- Virgin Galactic

- Rocket Lab

- United Launch Alliance

- Arianespace

- China Aerospace Science and Technology Corporation

- Mitsubishi Heavy Industries

- Eurockot Launch Services

- Northrop Grumman

- ExPace

- Firefly Aerospace

- Relativity Space

- Orbital ATK

- International Launch Services

- Antrix Corporation

- Vector Launch

- Spaceflight Industries

- ISRO

- NASA

- Virgin Orbit

- Boeing

Market Segmentation

This study forecasts revenue at global, regional, and country levels from 2023 to 2033.

Space Launch Services Market, Orbit Type Analysis

- LEO

- GEO

- Others

Space Launch Services Market, Launch Vehicle Analysis

- Small Lift Launch Vehicle

- Medium Lift Launch Vehicle

- Heavy Lift Launch Vehicle

Space Launch Services Market, Payload Analysis

- Satellite

- Cargo

- Human Spacecraft

- Testing Probes

Space Launch Services Market, End User Analysis

- Civil & Military

- Commercial

Space Launch Services Market, Regional Analysis

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- Uk

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?