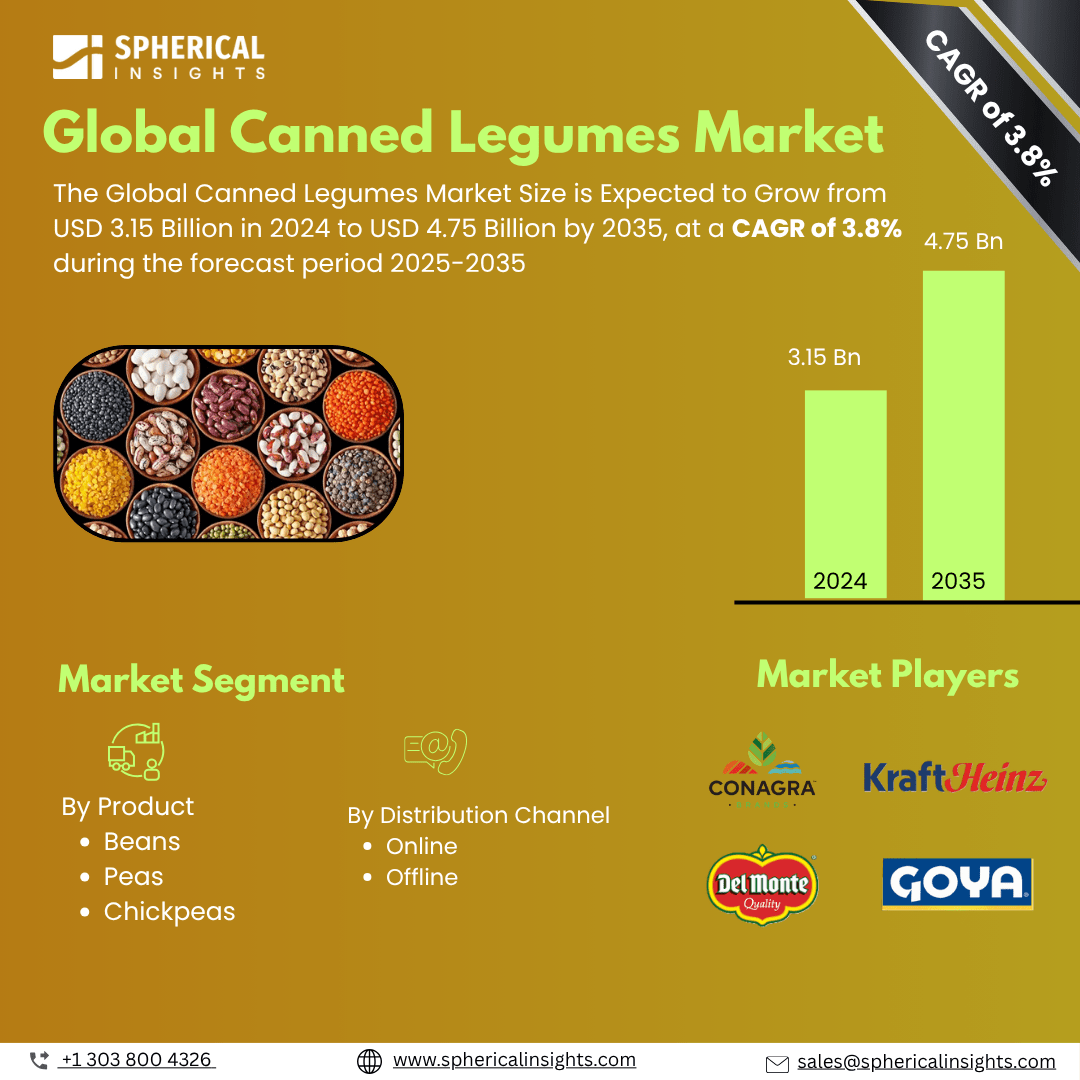

Global Canned Legumes Market Insights Forecasts to 2035

- The Global Canned Legumes Market Size Was Estimated at USD 3.15 billion in 2024

- The Market Size is Expected to Grow at a CAGR of around 3.8% from 2025 to 2035

- The Worldwide Canned Legumes Market Size is Expected to Reach USD 4.75 billion by 2035

- North America is expected to grow the fastest during the forecast period.

Canned Legumes Market

The canned legumes market involves the production and distribution of legumes such as beans, lentils, chickpeas, and peas preserved in cans for convenient use. These products provide a quick and easy way for consumers to incorporate nutrient-rich legumes into their meals, offering benefits like high protein, fiber, and essential nutrients. Canned legumes come in various forms, including plain, flavored, and ready-to-eat options, addressing different taste preferences and culinary uses. Manufacturers focus on ensuring product quality, safety, and shelf stability through advanced preservation and packaging techniques. The market includes a wide range of players, from large food corporations to smaller specialty brands. Overall, canned legumes serve as a versatile and accessible food choice, supporting consumers who value both nutrition and convenience. As part of the broader packaged food sector, the canned legumes market continues to sustain demand through ongoing product innovation and consumer interest in wholesome, easy-to-prepare foods.

Attractive Opportunities in the Canned Legumes Market

- Expanding offerings to include organic, non-GMO, low-sodium, gluten-free, vegan, and allergy-friendly canned legumes caters to evolving consumer preferences for health-conscious and specialized diets.

- Rapid urbanization, rising disposable incomes, and changing dietary habits in emerging economies present untapped demand for convenient, nutritious foods like canned legumes.

- Partnering with foodservice providers, meal delivery services, and boosting presence on e-commerce platforms and digital marketing helps brands engage tech-savvy consumers and extend their reach efficiently.

Global Canned Legumes Market Dynamics

DRIVER: Increasing consumer awareness about health and nutrition

Increasing consumer awareness about health and nutrition encourages the consumption of legumes, which are rich in protein, fiber, and essential nutrients. The rising demand for plant-based and vegetarian diets also contributes significantly, as legumes serve as an affordable and sustainable protein source. Convenience plays a major role, with busy lifestyles prompting consumers to choose ready-to-eat and easy-to-prepare foods like canned legumes. Innovations in packaging and preservation methods have improved product shelf life and quality, making canned legumes more appealing. Additionally, growing interest in sustainable and environmentally friendly food options supports the market, as legumes have a lower carbon footprint compared to animal proteins. These factors collectively enhance the acceptance and integration of canned legumes into everyday diets, fueling steady market growth worldwide.

RESTRAINT: Perception of canned foods as less fresh or less natural compared to dried or fresh legumes

One significant challenge is the perception of canned foods as less fresh or less natural compared to dried or fresh legumes, which can deter health-conscious consumers. Additionally, concerns over the presence of preservatives, sodium content, and BPA in can linings contribute to consumer hesitation. Price fluctuations in raw legume crops due to climate conditions or supply chain disruptions can also impact production costs and market stability. Moreover, competition from alternative protein sources, such as fresh legumes, frozen options, and plant-based meat substitutes, can reduce demand for canned varieties. Limited awareness in certain consumer segments and cultural preferences for fresh ingredients further restrict market expansion. These factors, combined with the availability of dried legumes that offer longer shelf life without preservatives, present challenges for the canned legumes market to capitalize on its growth potential fully.

OPPORTUNITY: Expanding into niche markets such as gluten-free

There is growing potential in product diversification, including organic, non-GMO, low-sodium, and ready-to-eat meal kits that cater to evolving consumer preferences for health and convenience. Expanding into niche markets such as gluten-free, vegan, and allergy-friendly options can attract a broader customer base. Innovations in sustainable packaging, such as recyclable or biodegradable cans, offer opportunities to appeal to environmentally conscious consumers. Additionally, emerging markets with rising urbanization and changing dietary habits present untapped demand for convenient and nutritious foods like canned legumes. Collaborations with foodservice providers and meal delivery services also open new distribution channels. Lastly, leveraging digital marketing and e-commerce platforms can help brands increase consumer engagement and accessibility, driving growth by meeting the needs of tech-savvy shoppers. These opportunities position the canned legumes market for expansion through innovation and targeted outreach.

CHALLENGES: Maintaining consistent product quality and taste

One major challenge is maintaining consistent product quality and taste, especially when scaling production to meet growing demand. Ensuring uniformity across batches while preserving nutritional value requires advanced processing technologies and rigorous quality control. Another challenge lies in supply chain complexities, such as sourcing high-quality legumes amidst variable agricultural yields influenced by weather and pests. Additionally, regulatory compliance related to food safety standards and labeling varies across regions, creating hurdles for manufacturers expanding globally. Marketing canned legumes to younger generations, who may prefer fresh or trendy plant-based alternatives, also poses a challenge in terms of consumer education and brand positioning. Finally, managing competition not only from other legumes but also from emerging protein sources like insect-based foods or lab-grown options adds pressure for innovation and differentiation. Addressing these challenges is crucial for sustained growth and competitiveness in the market.

Global Canned Legumes Market Ecosystem Analysis

The global canned legumes market ecosystem includes raw material suppliers (farmers), manufacturers who process and can legumes, and packaging suppliers providing sustainable cans. Distribution channels span wholesalers, retailers, e-commerce, and foodservice providers, ensuring product availability. Consumers drive demand with preferences for convenience and nutrition, while regulatory bodies enforce food safety and quality standards. Marketing agencies play a key role in promoting products and building brand loyalty. Together, these components form a dynamic network that supports the production, distribution, and consumption of canned legumes worldwide.

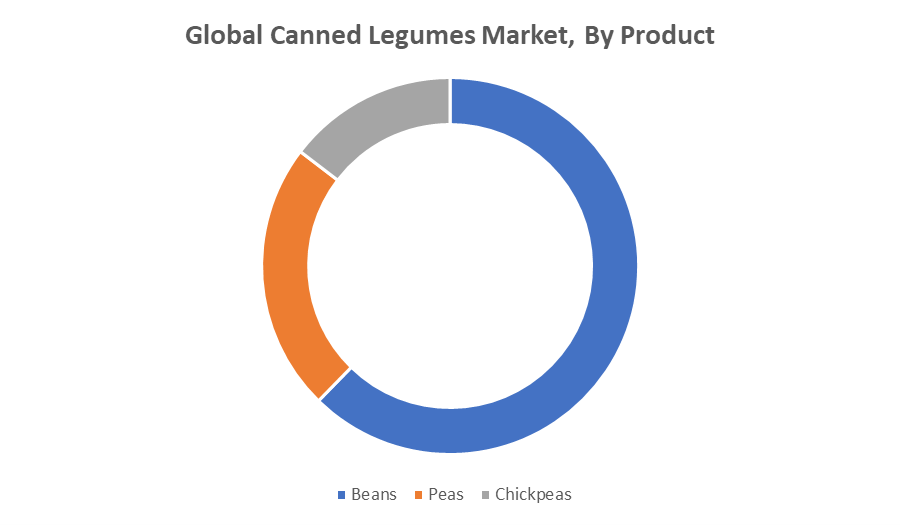

Based on the product, the beans segment dominated the global canned legumes market, with a revenue share over the forecast period

Beans segment dominance is attributed to the widespread popularity and versatile use of various bean varieties, such as kidney beans, black beans, and navy beans, in multiple cuisines worldwide. Beans are favored for their rich nutritional profile, including high protein and fiber content, making them a staple in many diets. Their convenient canned form offers ease of preparation and long shelf life, further driving consumer preference and contributing to the segment’s leading market position.

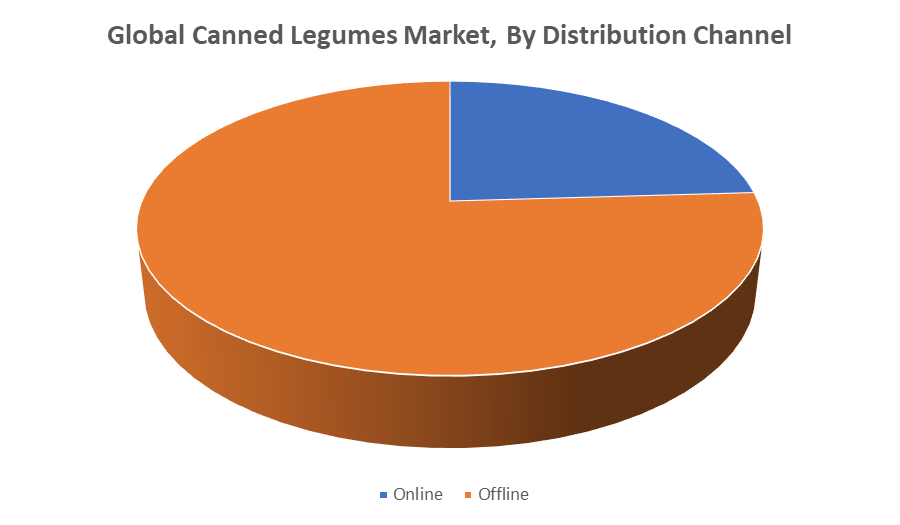

Based on the distribution channel, the offline distribution held the largest canned legume market revenue share over the forecast period

Offline segment held the largest revenue share in the canned legumes market over the forecast period. This is largely due to the strong presence of supermarkets, hypermarkets, grocery stores, and convenience stores, which remain the primary purchasing points for many consumers seeking canned legumes. The offline channel offers easy access, product variety, and the ability to inspect products before purchase, which continues to drive significant sales. Despite the growing popularity of online shopping, traditional retail outlets dominate due to their established networks and consumer trust, securing the offline channel’s leading position in the market revenue share.

Asia Pacific is anticipated to hold the largest market share of the canned legumes market during the forecast period

Asia Pacific is anticipated to hold the largest market share of the canned legumes market during the forecast period. This growth is driven by the region’s large and diverse population, increasing urbanization, and shifting consumer preferences towards convenient and nutritious food options. Rising awareness of health benefits associated with legumes, coupled with expanding retail infrastructure and growing demand for ready-to-eat products, further supports market expansion. Additionally, emerging economies in the region are witnessing higher disposable incomes, encouraging greater consumption of packaged foods like canned legumes. These factors collectively position Asia Pacific as the dominant player in the global canned legumes market throughout the forecast period.

North America is expected to grow at the fastest CAGR in the canned legumes market during the forecast period

North America's growth is driven by increasing consumer demand for convenient, nutritious, and plant-based food options, particularly beans, which are the leading product segment in the region. The popularity of vegetarian, vegan, and flexitarian diets, along with the expansion of online grocery shopping and quick delivery services, further supports the market's expansion. Additionally, the growing inclination towards sustainable and eco-friendly packaging solutions is contributing to the market's development in North America.

Recent Development

- In September 2024, SER!OUS Bean Co. launched its new line of organic beans with Himalayan pink salt. The initial offerings include organic black beans and garbanzo beans, with red kidney beans and pinto beans following later in the fall. These beans are USDA organic, non-GMO, and naturally lower in sodium due to the use of Himalayan pink salt.

Key Market Players

KEY PLAYERS IN THE CANNED LEGUMES MARKET INCLUDE

- Conagra Brands, Inc.

- The Kraft Heinz Company

- Del Monte Foods, Inc.

- General Mills (Green Giant)

- Goya Foods, Inc.

- Bonduelle Group

- B&G Foods, Inc.

- Hain Celestial Group

- Eden Foods

- Seneca Foods Corporation

- Others

Market Segment

This study forecasts revenue at global, regional, and country levels from 2020 to 2035. Spherical Insights has segmented the canned legumes market based on the below-mentioned segments:

Global Canned Legumes Market, By Product

Global Canned Legumes Market, By Distribution Channel

Global Canned Legumes Market, By Regional Analysis

- North America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East & Africa

- UAE

- Saudi Arabia

- Qatar

- South Africa

- Rest of the Middle East & Africa