Top 15 Companies in the Global Automotive Active Safety Market (2024–2035): Spherical Insights Analysis

RELEASE DATE: Mar 2026 Author: Spherical InsightsRequest Free Sample Speak to Analyst

Introduction

Automotive active safety represents a paradigm shift from surviving crashes to preventing them entirely through a digital shield of electronic intervention systems that monitor a vehicle’s surroundings in real-time. This safety architecture relies on a sophisticated fusion of LiDAR, high-resolution radar, and AI-driven cameras that act as the vehicle's eyes, machine learning algorithms processing gigabytes of data every second to detect hazards invisible to the human eye, enabling vehicles to navigate complex driving environments safely. In practical terms, these technologies manifest as Autonomous Emergency Braking (AEB) and Lane Keep Assist, which can autonomously steer a car back on track or slam the brakes milliseconds before a potential collision. This transition is being accelerated by landmark regulatory shifts, such as the NHTSA’s 2024 final ruling mandating AEB on all new passenger vehicles by 2029 and India's 2025 Cashless Treatment & phased ADAS mandates for commercial fleets.

Navigate Future Markets with Confidence: Insights from Spherical Insights LLP

The insights presented in this blog are derived from comprehensive market research conducted by Spherical Insights LLP, a trusted advisory partner to leading global enterprises. Backed by in-depth data analysis, expert forecasting, and industry-specific intelligence, our reports empower decision-makers to identify strategic growth opportunities in fast-evolving sectors. Clients seeking detailed market segmentation, competitive landscapes, regional outlooks, and future investment trends will find immense value in the full report. By leveraging our research, businesses can make informed decisions, gain a competitive edge, and stay ahead in the transition toward sustainable and profitable solutions.

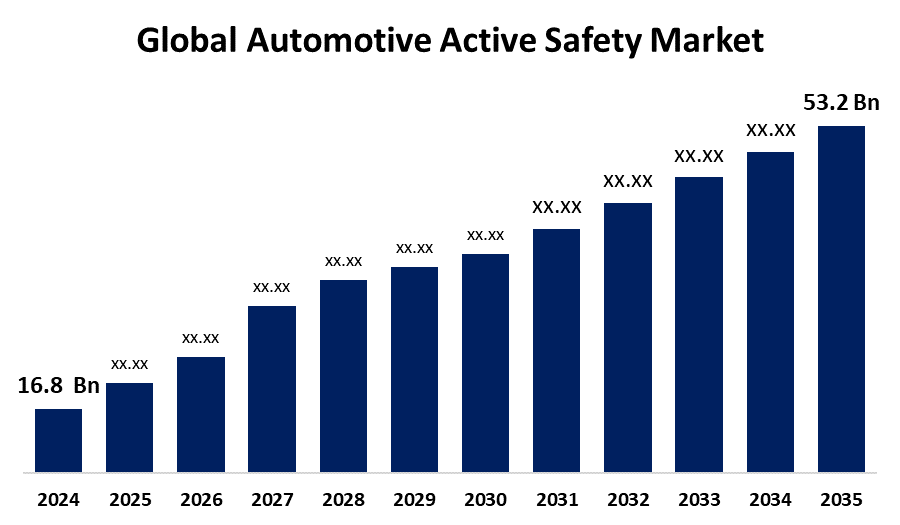

Global Automotive Active Safety Market Size & Statistics

- The Global Automotive Active Safety Market was estimated to be worth USD 16.8 billion in 2024.

- The market is projected to expand at a steady CAGR of 11.05% between 2024 and 2035.

- The Global Automotive Active Safety Market Size is anticipated to reach USD 53.2 billion by 2035.

- North America is identified as the region with the highest revenue demand during the forecast period. This is primarily fuelled by the NHTSA’s 2024 mandate requiring all light vehicles to have Automatic Emergency Braking (AEB) by 2029 and a rapid consumer shift toward Level 3 autonomous driving features.

- Asia-Pacific is identified as the fastest-growing region. Growth is spearheaded by China’s 2028 national standards for standard-fitment AEB and India’s 2025 phased ADAS mandates for commercial fleets, alongside a massive rise in domestic EVs.

Unlock exclusive market insights—Download the Brochure now and dive deeper into the future of the Automotive Active Safety Market.

Regional Growth & Demand Analysis

North America is the Highest Demand region through 2035. Growth is centred on the U.S. market following the NHTSA’s 2024 mandate requiring all passenger vehicles to have Automatic Emergency Braking (AEB) by 2029. Large investments in Level 3 autonomy from Detroit and Silicon Valley firms are moving active safety from premium models to standard fleet requirements. The region's lead is sustained by high adoption rates of V2X (Vehicle-to-Everything) tech and strict consumer safety ratings.

Asia-Pacific is the fastest-growing region in this sector during the forecast period. The surge is driven by massive EV production in China and new safety laws in India. Key triggers include China’s 2026-2027 mandatory standards for Level 3 automated driving and India’s Bharat NCAP ratings, which have shifted buyer preference toward high-safety vehicles. With local brands like BYD and Tata integrating radar and camera systems into budget-friendly cars, the region is now the world's primary hub for mass-market active safety hardware.

Global Automotive Active Safety Market Segmentation

The Global Automotive Active Safety Market is segmented by System Type (Adaptive Cruise Control, Automatic Emergency Braking, Lane Departure Warning, Blind Spot Detection, and Others), Sensor Technology (Radar, Camera, LiDAR, and Ultrasonic Sensors), and Offering (Hardware Components and Software Solutions), with a focus across Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles & Buses). The analysis also provides a geographic breakdown across regions (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa), offering a detailed forecast for the 2024–2035 period.

Ready to lead the Automotive Active Safety Market?

Discover the regional trends and growth factors shaping the industry. We’re here to assist with expert, personalized data.

Call +1 303 800 4326 or Send us a message for a personalized consultation.

Top 10 Trends in the Global Automotive Active Safety Market

- Shift from Reactive to Proactive AI

- The Rise of 4D Imaging Radar

- Mandatory AEB Standardisation

- V2X (Vehicle-to-Everything) Integration

- Expansion of Driver Monitoring Systems (DMS)

- Edge Computing for Zero-Latency Sensing

- Software-Defined Safety (OTA Updates)

- Digital Twins for Crash Simulation

- Affordable ADAS for Emerging Markets

- Lidar-Camera Sensor Fusion

Unlock exclusive market insights—Download the Brochure now and dive deeper into the future of the Automotive Active Safety Market.

- Shift from Reactive to Proactive AI

The industry is moving away from last-second safety toward predictive prevention. While older systems only brake after a hazard is detected, new Proactive AI uses continuous data streams to forecast risks before they are visible. These systems reason through variables like road friction, pedestrian trajectories, and blind-spot data to subtly adjust speed or position, effectively stopping an accident before the driver even realises there was a threat.

- The Rise of 4D Imaging Radar

Standard radar is being replaced by 4D Imaging Radar, which adds height to the traditional data of distance, speed, and angle. This tech allows a vehicle to distinguish between a stationary car under a bridge and the bridge itself—a major flaw in earlier ADAS. By mapping surroundings in high-definition 4D, cars can navigate complex urban environments and see through heavy fog or rain where cameras usually fail.

- Mandatory AEB Standardisation

Automatic Emergency Braking (AEB) is no longer a luxury feature for premium cars. Following the NHTSA’s 2024 final rule, AEB must be standard on all light vehicles in the U.S. by September 2029. This legal shift forces manufacturers to integrate high-speed braking and night-time pedestrian detection into every base model, moving the market toward a safety-first baseline for all global consumers.

- V2X (Vehicle-to-Everything) Integration

Cars are losing their isolation and becoming part of a connected network. Through V2X communication, a vehicle can receive instant alerts from smart traffic lights or other cars about a crash three blocks ahead or an approaching ambulance. This digital sight allows vehicles to coordinate at intersections and avoid invisible collisions, drastically reducing the 94% of accidents currently caused by human perception errors.

- Expansion of Driver Monitoring Systems (DMS)

Safety is now looking inside the cabin as much as outside. Modern DMS uses near-infrared cameras and AI to track eye movement, head position, and even micro-sleep patterns. Instead of just a generic beep, these systems can detect if a driver is distracted by a phone or falling asleep and will escalate alerts—or even safely pull the car over—to prevent a fatigue-related disaster.

Empower your strategic planning:

Stay informed with the latest industry insights and market trends to identify new opportunities and drive growth in the automotive active safety market. To explore more in-depth trends, insights, and forecasts, please refer to our detailed report.

Top 15 Companies in the Global Automotive Active Safety Market

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Denso Corporation

- Autoliv Inc.

- Hyundai Mobis

- Magna International Inc.

- Valeo SA

- Aptiv PLC

- Infineon Technologies AG

- Mobileye (Intel)

- NXP Semiconductors

- BorgWarner Inc.

- Texas Instruments

- Renesas Electronics

- Robert Bosch GmbH

Headquarters: Gerlingen, Germany

The undisputed heavyweight in automotive electronics, Bosch sets the global benchmark for sensor fusion. Their iBooster and ESP (Electronic Stability Program) systems are the core components of modern collision avoidance. Bosch is currently focusing on a Software-Defined Vehicle strategy, integrating AI-driven predictive analytics that allow vehicles to anticipate hazardous road conditions and pedestrian movements long before a human driver can react.

- Continental AG

Headquarters: Hanover, Germany

Continental is a pioneer in radar technology, having recently surpassed the milestone of 200 million radar sensors produced globally. The firm’s strategic focus is on the See-Think-Act chain, particularly through its 2025 launch of Holistic Motion Control software. This technology decouples safety functions from hardware, allowing for over-the-air (OTA) updates that improve a vehicle’s emergency braking and lane-keeping capabilities throughout its entire lifespan.

- ZF Friedrichshafen AG

Headquarters: Friedrichshafen, Germany

ZF is a leader in high-performance computing and intelligent mechanical systems. Following the 2024-2025 spin-off of its passive safety division (ZF Lifetec), the company doubled down on Autonomous Driving and Electronics. Their ProAI supercomputer acts as the central brain for active safety, managing complex data from LiDAR and cameras to execute Level 3 autonomous manoeuvres, particularly in the premium passenger car and commercial trucking segments.

- Denso Corporation

Headquarters: Kariya, Aichi, Japan

A cornerstone of the Toyota Group's technical ecosystem, Denso focuses on Peace of Mind through mass-market ADAS democratisation. Denso's 2025–2030 strategy emphasises high-precision sensing that works in extreme weather conditions where standard sensors often fail. They are currently leading the integration of Global Safety Packages in emerging markets like India and Southeast Asia, bringing advanced collision-avoidance tech to affordable, high-volume vehicle segments.

- Autoliv Inc.

Headquarters: Stockholm, Sweden

While historically known for airbags, Autoliv became a major player in the active safety transition by focusing on the Human-Machine Interface (HMI). Their 2025 roadmap highlights Learning Intelligent Vehicles (LIV), which uses interior AI to monitor driver distraction and fatigue. Autoliv is uniquely positioning itself to bridge the gap between active and passive safety, developing external pedestrian airbags that deploy automatically when active sensors detect an unavoidable impact with a cyclist or walker.

Are you ready to discover more about the Automotive Active Safety Market?

The report provides an in-depth analysis of the leading companies operating in the global automotive active safety market. It includes a comparative assessment based on their product portfolios, business overviews, geographical footprint, strategic initiatives, market segment share, and SWOT analysis. Each company is profiled using a standardised format that includes:

Company Profiles

- Robert Bosch GmbH

- Business Overview

- Company Snapshot

- Products Overview

- Company Market Share Analysis

- Company Coverage Portfolio

- Financial Analysis

- Recent Developments

- Merger and Acquisitions

- SWOT Analysis

- Continental AG

- ZF Friedrichshafen AG

- Denso Corporation

- Autoliv Inc.

- Hyundai Mobis

- Magna International Inc.

- Valeo SA

- Aptiv PLC

- Infineon Technologies AG

- Mobileye (Intel)

- NXP Semiconductors

- BorgWarner Inc.

- Texas Instruments

- Renesas Electronics

Conclusion

The global automotive active safety market is making a definitive turning point where accident prevention is no longer a premium upgrade but a basic legal requirement. Driven by a massive USD 53.2 billion valuation by 2035, the industry is moving past simple alerts toward a proactive shield powered by 4D radar and Agentic AI due to technological advancements that can intervene before a human even perceives a threat. While North America maintains its lead through aggressive NHTSA mandates, the Asia-Pacific region is the new engine of volume, catalysed by Bharat NCAP and China’s standardised safety fitments. Ultimately, the next decade will be defined by V2X connectivity and software-defined architectures that aim to effectively engineer human error out of the driving experience, turning the zero-collision vision into a scalable global reality.

About the Spherical Insights & Consulting

Spherical Insights & Consulting is a market research and consulting firm which provides actionable market research study, quantitative forecasting and trends analysis provides forward-looking insight especially designed for decision makers and aids ROI.

Which is catering to different industry such as financial sectors, industrial sectors, government organizations, universities, non-profits and corporations. The company's mission is to work with businesses to achieve business objectives and maintain strategic improvements.

CONTACT US:

For More Information on Your Target Market, Please Contact Us Below:

Phone: +1 303 800 4326 (the U.S.)

Phone: +91 90289 24100 (APAC)

Email: inquiry@sphericalinsights.com, sales@sphericalinsights.com

Contact Us: https://www.sphericalinsights.com/contact-us

Need help to buy this report?